Africa Could Mine Its Way to Prosperity If It Addressed Instability

share

share

share

share

share

share

share

share

share

share

Last week I attended the Investing in African Mining Indaba in Cape Town, South Africa, as both a presenter and a student seeking opportunities. One of the highlights of the conference was former Prime Minister Tony Blair’s keynote address, during which he offered some crucial advice to African governments: To attract and foster a robust mining sector, a commitment to fiscal stability must be made.

Last week I attended the Investing in African Mining Indaba in Cape Town, South Africa, as both a presenter and a student seeking opportunities. One of the highlights of the conference was former Prime Minister Tony Blair’s keynote address, during which he offered some crucial advice to African governments: To attract and foster a robust mining sector, a commitment to fiscal stability must be made.

Since 2009, Blair has run the Africa Governance Initiative, which counsels leaders in countries such as Rwanda, Sierra Leone, Liberia, Guinea and others.

Simply put, without fiscal stability and predictability in taxation, capital will be unwilling to flow into any country—African or otherwise—for exploration and production. If a government changes its tax policy every three years or so, that instability discourages the inflow of financing. This is bad for Africa.

“The mining sector remains absolutely vital for Africa’s future,” Blair said, “and even with the sharp declines in [commodity] prices, there are tremendous opportunities and there will be, no doubt, an adjustment and reshaping of the face of mining within Africa over these next few years.”

I shared the following map last week, but it’s worth showing again, as it supports Blair’s point. Central and Southern Africa, especially, are extremely commodity-rich and maintain a large global share of important metals and minerals such as platinum, diamonds and gold.

Fiscal instability is also bad for investors in Africa. If foreign investment is not respected by a government, if it is punitively taxed or arbitrarily confiscated, further investment will not flow into that country. Politically, African nations need to recognize that seemingly faceless investment institutions represent real people’s hard earned dollars.

In Zambia, for example, a huge 12 percent of the country’s GDP comes from mining, an industry that employs 10 percent of all Zambians. Yet its government has increased, rather than cut or at least eased, restrictive royalty taxes on mines. In the case of open pit mines, royalties were raised from 6 percent to a crippling 20 percent.

Speaking to Reuters, a mining industry spokesperson speculated: “Mining companies are not going to put another dollar in [Zambia]” if the government continues to be unreliable.

Less Friction, Fewer Disruptions

This is proof positive of what I frequently say: Government policy is a precursor to change. In the example above, the tax policy is leading to change that could very well hurt Zambia’s economy. With mining being such a strong contributor to its GDP, it seems the government would want to make it easier, not more challenging and costly, for international producers to conduct business there.

The less friction and fewer disruptions there are, the easier it is for money to flow.

But Zambia’s isn’t the only African government that’s placing roadblocks in front of miners. The Democratic Republic of Congo is in the early stages of hiking royalties on mines and revising its mining code. And in his recent State of the Nation Address, South African President Jacob Zuma announced that foreigners could no longer own land in the country, which raises the question of what implications, if any, this might have on U.S. and Canadian companies that own and operate South African mines. Zuma’s announcement comes at a time when persistent electricity shortages have stymied mining activity and rumblings of a miners’ strike similar to the one last year that brought platinum and palladium production to a five-month halt are intensifying.

At the same time, many governments in Africa are waking up to see that they’re going to have to provide the sort of stability and consistency Prime Minister Blair outlined if they hope to attract the capital necessary to fund and develop their mining opportunities.

Miners Giving Back

A strong mining sector doesn’t just benefit the native country, either. It’s a global good that benefits all. In another presentation at the African Mining Indaba, Terry Heymann of the World Gold Council convincingly showed that the economic output of the global gold mining sector far exceeds the collective aid budget of world governments. Gold mining, he said, created and moved as much as $47.3 billion to suppliers, businesses and communities in 2013, compared to governments’ $37.4 billion.

Many gold mining companies take a more direct approach to helping the communities in the countries they operate in, including Randgold Resources, which works primarily in Mali. In an interview during the African Mining Indaba, CEO Mark Bristow detailed his company’s involvement in the fight against Ebola and other epidemics that have hit the West African country:

Our doctors, the Randgold doctors, run a technical committee meeting every day where we coordinate with the [Malian] health authorities, and we help manage the deployment of energy. Now that we’ve eradicated the second [Ebola] outbreak, our big focus is on prevention and education.

Bristow explained that the company had sponsored the development of an educational film about Ebola, before highlighting other company achievements:

Bristow explained that the company had sponsored the development of an educational film about Ebola, before highlighting other company achievements:

We were part of the Neglected Tropical Disease Initiative rollout… We’re very big on the AIDS programs around the country. We brought the malaria incident rate around our mines down by more than four times.

Because Randgold is the largest employer in Mali, Bristow suggested, he feels a moral obligation to partner with his host country and make it a healthier, safer place to live and work.

During the same interview, he insisted that Randgold, which we hold in our Gold and Precious Metals Fund (USERX) and World Precious Minerals Fund (UNWPX), has a “solid five years ahead of us,” citing the fact that the company holds no debt and managed to replace all the ounces it mined in 2014 at $1,000 long-term gold price. It also increased its dividend 20 percent.

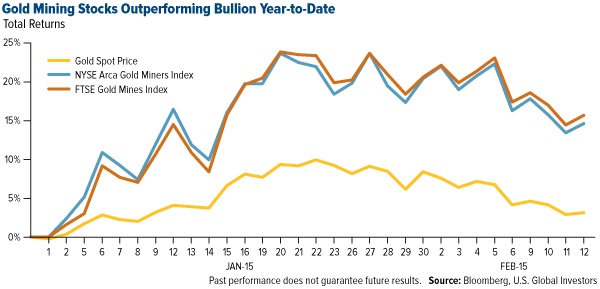

Despite bullion’s price hovering just above the relatively low $1,230 range, Randgold has delivered 16 percent year-to-date.

This is in line with gold mining stocks in both the NYSE Arca Gold Miners Index and FTSE Gold Mines Index, which are outperforming the return on bullion.

As I mentioned back in July, when mining stocks do well, bullion has tended to follow suit. This also shows that producers are successfully adjusting to a $1,200-per-ounce environment by scaling back on capital spending, selling off assets, putting exploration on hold and engaging in mergers and acquisitions—which in the past has signaled that a bottom in spot prices might be reached. B2Gold Corp. closed on its deal to buy Papillon Resources in October; we learned in November that Osisko Gold Royalties is taking over Virginia Mines; and last month it was announced that Goldcorp would be purchasing Probe Mines.

Weak Currencies, Low Fuel Prices

Speaking with Kitco News’s Daniela Cambone during last Monday’s Gold Game Film, I commented on some of the macro events aiding gold mining companies such as Randgold:

Mark Bristow has just hit the ball out of the park. He benefits from a weak Mali currency and he benefits from a weak euro because everything is priced in euros. He’s also benefited from weak oil prices.

Indeed, many miners not operating in the U.S. are the beneficiaries of a weak local currency. The West African CFA franc, Mali’s currency, is off 20 percent; the South African rand, 40 percent; the Canadian dollar, 15 percent.

Low energy prices are also helping gold producers, just as they’re helping companies in other industries, airlines especially. In most cases, fuel accounts for between 20 and 30 percent of gold miners’ total operating costs. Because Brent oil is currently priced around $60 per barrel, gold producers are seeing significant savings.

The Gold Demand

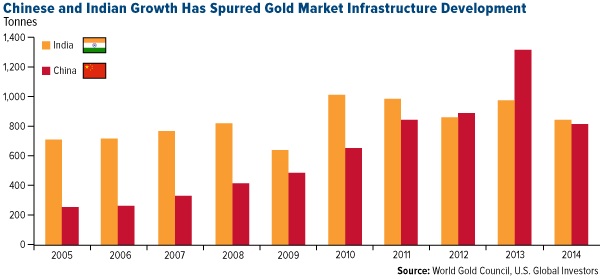

This Thursday marks the Chinese New Year, a traditional occasion for gold gift-giving. Chinese demand for the yellow metal was strong in 2014, as 800 tonnes flowed into the country. Over half of the global gold demand, in fact, was driven by the world’s two largest markets, China and India.

Historically low real interest rates are also driving investors into gold and gold stocks. As I told Daniela:

When you look at real interest rates out of the G7 and G10 countries, the only one with a modest increase is the U.S. dollar. Any time you get this negative real interest rate scenario, gold starts to rally in those countries’ currencies. Now what’s really dynamite is the gold mining companies like Goldcorp, which pays a dividend higher than a 5-year government bond.

Emerging Markets Webcast

Make sure to join us during our webcast today, February 18. USGI Director of Research John Derrick, portfolio manager of our China Region Fund (USCOX) Xian Liang and I will be discussing reflationary measures in China and emerging Europe. Don’t miss it!

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Gold, precious metals, and precious minerals funds may be susceptible to adverse economic, political or regulatory developments due to concentrating in a single theme. The prices of gold, precious metals, and precious minerals are subject to substantial price fluctuations over short periods of time and may be affected by unpredicted international monetary and political policies. We suggest investing no more than 5% to 10% of your portfolio in these sectors.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The index benchmark value was 500.0 at the close of trading on December 20, 2002.

The FTSE Gold Mines Index Series encompasses all gold mining companies that have a sustainable and attributable gold production of at least 300,000 ounces a year, and that derive 75% or more of their revenue from mined gold.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. Note that stocks and Treasury bonds differ in investment objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, and tax features. A fund’s yield may differ from the average yield of dividend-paying stocks held by the fund.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the Gold and Precious Metals Fund, World Precious Minerals Fund and China Region Fund as a percentage of net assets as of 12/31/2014: B2Gold Corp. 0.28% World Precious Minerals Fund; Goldcorp, Inc. 1.03% Gold and Precious Metals Fund; Osisko Gold Royalties 0.00%; Papillion Resources 0.00%; Probe Mines 0.00%; Randgold Resources Ltd. 2.30% Gold and Precious Metals Fund, 1.43% World Precious Minerals Fund; Virginia Mines, Inc. 1.14% Gold and Precious Metals Fund, 10.35% World Precious Minerals Fund.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

share

share

share

share

share

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

More from Silver Phoenix 500