How Rare Are Municipal Bankruptcies? A Lot Rarer Than You Think!

share

share

share

share

share

share

share

share

share

share

The odds of being struck by lightning are an insignificant 0.03 percent, yet many people still worry it might happen to them. There’s even a name for it: astraphobia. Similarly, some muni bond investors worry about municipal bankruptcies, based on recent high-profile cases, even though such cases occur very infrequently.

Think Orange County, California, in 1994; Jefferson County, Alabama, in 2011; or Detroit, Michigan, in 2013, the largest in U.S. history. Today, federal legislators are debating whether to allow debt-strapped Puerto Rico, which owes around $70 billion, to file for bankruptcy, something even U.S. states are not permitted to do.

These cases can sometimes lead to splashy headlines, which contributes to the misperception that they happen much more often than they actually do.

What municipal bond investors need to know is that, though there’s risk involved with any investment, municipal defaults are rare, and significantly rarer than their corporate counterparts.

Between 1937, when the U.S. Bankruptcy Code went into effect, and 2008, approximately 600 municipalities out of 90,000 filed for Chapter 9 protection. Governing magazine estimates that between 2008 and 2012, “only one of every 1,668 eligible general-purpose local governments filed for bankruptcy protection.” That amounts to a barely-there 0.06 percent—nearly in line with the odds of being struck by lightning—and includes everything from Aaa-rated municipalities to junk.

So far this year, only three local governments have filed, a 75 percent decline compared to 2012.

Often More Trouble than It’s Worth

One of the main reasons why municipal bankruptcies are so rare is because the hurdles are set exceedingly high. Unlike an individual or corporation, a city can’t independently arrive at the decision to file. Federal law allows local governments to file, but the municipality’s state government must also permit it. Strings ordinarily come attached.

Currently, only 12 states authorize municipalities to file for bankruptcy without conditions—Alabama, Arizona, Arkansas, Idaho, Minnesota, Missouri, Montana, Nebraska, Oklahoma, South Carolina, Texas and Washington State. Another 12 states permit filing only when certain conditions have been met.

There’s also a huge amount of pushback. Bankruptcy is never an easy decision, but for local governments, it’s often more trouble than it’s worth. Citizens oppose it since it often leads to painful budget cuts and austerity measures. Obviously bondholders and pensioners are against it. States don’t like it because they fear it might tarnish their reputation and lower their credit ratings. Following Detroit’s bankruptcy, borrowing costs in surrounding Michigan counties went up.

This could affect what a state contributes to the national economy. The diagram below, courtesy of HowMuch.net, shows the relative economic value of each state, with California (13.3 percent), Texas (9.5 percent) and New York (8.1 percent) generating the most.

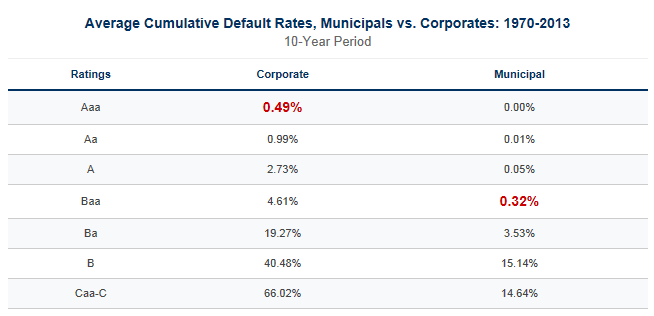

Highly-Rated Municipal Bonds Remained a Relatively Safe Asset Class

Closely related, default rates for high-quality municipal bonds—the kind our Near-Term Tax Free Fund (NEARX) heavily invests in—remain close to zero. Between 1970 and 2013, Baa-rated munis historically had similar default rates as Aaa-rated corporate bonds, according to ratings agency Moody’s.

Out of 25,000 equity and bond funds, only 30 have managed to deliver 20 straight years of positive returns, according to Lipper. NEARX is one of those 30 funds.

That’s a rare achievement indeed and represents the kind of track record most investment firms envy.

The recipient of glowing acknowledgements by popular financial and investment newsletter writers, NEARX is also highly-rated by Morningstar. It holds five stars overall among 187 Municipal National Short-Term funds as of 9/30/2015, based on risk-adjusted return.

Start taking advantage of our fixed-income expertise by requesting more information on NEARX today.

********

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

share

share

share

share

share

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

More from Silver Phoenix 500