Markets’ Ups And Downs

share

share

share

share

share

share

share

share

share

share

Stock markets in the US and those around the world, go up – and they go down. There are various names for the size and speed of the downdraft, which inevitably follow an up move. Pullback, correction, crash, and bear market are some of the terms used.

But, why do markets go up and down? “In the long term, markets are a weighing machine. In the short run, markets are a voting machine.” I’ve read that quote numerous times, attributed to several different people.

The gist of it is that, a company’s earnings and growth over the long haul are what will cause one company’s stock to double (or more!) while another’s goes down the toilet. But, since growth and earnings are measured in quarters, years, and longer, in the short run, it is how investors feel about those fundamentals – market participants’ sentiment – which causes the wiggles along the way. Sometimes those wiggles can be major temporary moves, but they still are just wiggles based on sentiment.

Those short run wiggles are no big deal, and are not so easy to make money from (although many traders have used MACD, RSI, chart patterns, and other methods successfully – and not).

Being sentiment driven, those wiggles also can have secondary sentiment effects, such as the “Wealth Effect.” If your stock just doubled during the last couple of months, you may be more inclined to buy a new car or go on a vacation, than if your stock went down.

So, there are short run, sentiment driven wiggles, and there are longer term, fundamentally driven up or down moves. However (now the other shoe drops), there are factors beyond the control either of investors or the businesses whose stocks they buy.

Just as politicians are trying to control our Global Climate today, those pols have been trying to control our Economic Environment for a hundred years or more. And, not just in the US.

The Federal Reserve, and Central Banks all around the world, manipulate the money supply and interest rates. Manipulate?! That’s a strong term. These brain trusts deign to determine the level of interest rates and the supply of paper money against what the rest of humanity – through the Free Market – would have those levels be. To me, that qualifies as manipulation.

Interest rates have many effects throughout our Economy, such as encouraging either personal saving or spending. One of those effects is much in the news today, and that is on the various stock markets around the world.

Through the perceived lessening of costs for businesses (lower interest expense) and a continuously falling value of each unit of the currency (more paper in circulation), businesses will have higher nominal profits, and investors will view those profits more favorably. Reduced yields on Bonds, etc also boost stocks’ relative allure.

Low interest rates make stock market margin money cheaper. Investors then can borrow more money more cheaply in order to invest. Low interest rates also encourage company managers to buy back their own stock, reinforcing the appearance of growing earnings.

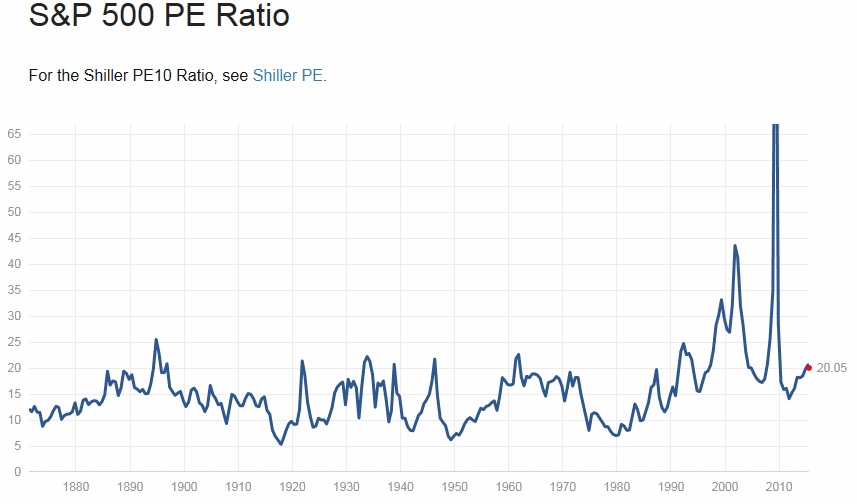

Over the last 100 years in the US, the average PE Ratio (the stock price compared to annual earnings) has run 14 or so. During secular bear markets, that PE can fall to 7 or less (that’s only 7 years to earn back your original investment, rather than 14!).

Generally, in the US, a PE of 21 is expensive – and we’re talking bubble territory when the general market PE gets to 28 or higher. These numbers are just guidelines, since numerous companies fudge their reported earnings (as with stock repurchases), but at least there is a rough guideline.

Today in the US, the PE on the S&P 500 is around 20 – on the expensive side. A good part of this is driven by the very high levels of margin debt.

One stock market which has tumbled recently is in Shanghai. There is much hand-wringing on the potential negative economic effects. But, this 5-year chart helps keep things in perspective. There was an obvious bubble, which has fallen almost 1/3 since the top. Prices today are down to what they were 4-5 months ago.

Excuse me if I don’t get overly excited about the world economy killing potential. Even if that index dropped a third from its current 3700, it still would be higher than it was a year ago. Yes, there will be winners and losers (what else is new).

As for the international effects, the average Chinese citizen still is quite poor by US standards. Though China today is the manufacturer for the world, their consumer market is tiny. A Chinese Recession – or Depression – would hurt the Chinese people mightily, but internationally, so far as trade goes, the effect would hardly be felt.

Some banks and financial institutions might have loans defaulted on, but that will just leave the remaining capital more in the hands of people who did a better job of allocating their funds. That’s the way the Free Market works, unless you let your government steal your money to do bailouts.

Stock markets go up, and they go down. We can minimize the effects of the swings by removing the external causes of the swings, which tend to cause the swings to be larger than a Free Market would dictate. And, with the swings which do appear, we should refrain from making matters worse through interest rate manipulation, bailouts, and tax policy.

share

share

share

share

share

Robert (Bob) Shapiro is self-taught in Austrian Economics and has consulted briefly for the governments of Mexico, Greece, Portugal and Spain. He has traded Gold & Silver and their stocks since 1970. Bob Shapiro’s blog is http://us-issues.com

Robert (Bob) Shapiro is self-taught in Austrian Economics and has consulted briefly for the governments of Mexico, Greece, Portugal and Spain. He has traded Gold & Silver and their stocks since 1970. Bob Shapiro’s blog is http://us-issues.com

More from Silver Phoenix 500