Silver Rocket And Gold Moribund

share

share

share

share

share

share

share

share

share

share

The prices of both metals were down again last week.

We would guess that it has something to do with the fact that everyone knows: higher rates are coming to the dollar. The yield on the 10-year Treasury closed the previous week at 1.762% and this week at 1.701%. ‘It may not look like much, but this is a change of +1.7%.’

Just repeat after me: “the Fed makes the economy more stable.”

In any case, there are a few holes in the “bonds are in a bubble” bubble. One is that the worldwide trend for 35 years is falling rates. If one wishes to argue that this trend is over, one would have to acknowledge its cause and argue that this cause is no longer in effect (one would need a real theory, not just the old “inflation expectations” saw).

More immediately, why are junk bonds and equities not dropping commensurately? If you look at a chart of junk bond yields, you see less volatility and the opposite trend. Since July 1, the Bloomberg High Yield Corporate Bond index is up 3.8%. In the same period, the Bloomberg US Treasury Bond Index is down 1.1%. When a bond price falls, that means the interest rate is higher.

For reference, 6-month LIBOR is up from 0.92% to 1.25%, or +36% (thirty six percent, not a typo).

We aren’t bond or equity traders, but we think it’s crystal clear that if rates are truly moving up, a lot, and durably, then all assets will be repriced lower. And if the US dollar is alone in bucking the falling rates trend, then look for a rising dollar index (i.e. all the other currencies will fall further, as traders will short them to get the even-greater interest rate differential).

Needless to say, the idea of a rising dollar does not fit the bond-bubble-burst rising-rates narrative.

So for the moment, the prices of the metals—silver more than gold—are driven by this narrative. How long until this narrative bursts?

There was an interesting news item this week, CME Group announced that it will presently launch a futures contract for the gold-silver ratio. This security will make it easier for the public to trade the gold-silver ratio. We think this is good, as it encourages arbitrage thinking. Of course, like every product in the market-casinos today, this one is designed to generate dollars (unlike our Fund, which deals in physical metal, and generates gains in gold). We will have more to say about this contract as it gets closer to launch (Oct 24).

Read on for the only true picture of the fundamentals of the monetary metals. But first, here’s the graph of the metals’ prices.

The Prices of Gold and Silver

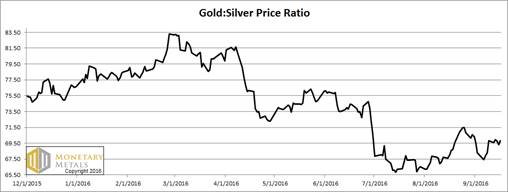

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. It did not change this week.

The Ratio of the Gold Price to the Silver Price

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

We switched from the October to December contract this week.

The price of gold fell this week, as did the basis.

The Monetary Metals fundamental price of gold is down just about as much as the market price.

Let’s look at silver.

The Silver Basis and Cobasis and the Dollar Price

The price of silver dropped just as much as gold, in proportion. The basis dropped more.

Our fundamental price is now two bucks under the market price. Does this mean the market price has to drop immediately, now that we know this? No, right now the market is in the grips of a mini silver mania (we would not dare say bubble, at least not without trigger warnings). Like the interest rate anomalies, it would be strange to see the price of silver take off like the famed mythological silver bug rocket while the price of gold languishes, moribund.

© 2016 Monetary Metals

share

share

share

share

share

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.

More from Silver Phoenix 500