Two Major Scenarios For The 60-Year Cycle Bottom

share

share

share

share

share

share

share

share

share

share

With less than a year to go before the bottom of the 60-year Super Cycle many investors are wondering how the coming months will play out. There are at least two major possibilities that need to be discussed: the soft landing and the hard landing.

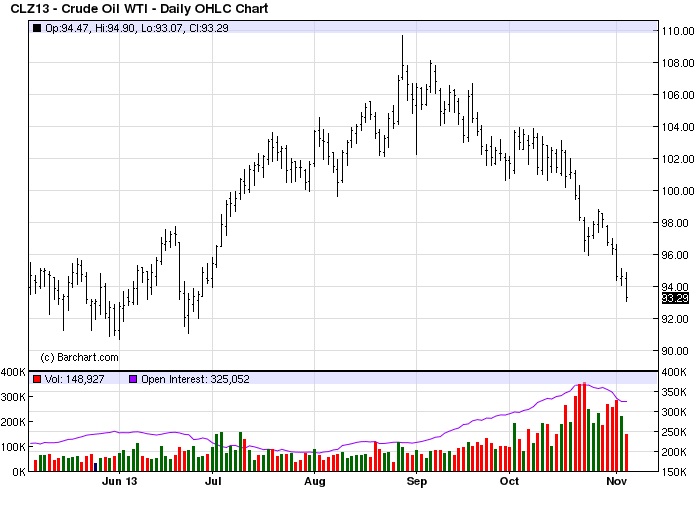

The effects long-term 60-year cycle, which answers to the economic long wave (K-Wave) can be seen in the fact that commodity prices and inflation are unusually low given the extraordinarily high levels of central bank and government stimulus in recent years. Despite $85 billion in monthly asset purchases by the Federal Reserve alone, the oil price – one of the most sensitive inflation indicators – has actually been declining in the last couple of months.

Its effects can also be seen in the fact that the job market remains an issue for central banks. The labor participation rate has dropped steadily in recent years as many unemployed have given up seeking work. And as we looked at in my previous commentary, money velocity has been steadily declining despite record amounts of liquidity being created by the Fed. All these indicators are symptomatic of a major deflationary undercurrent. The Fed is well aware of this structural problem and this is why it has steadfastly maintained a continuous flow of liquidity, for without this life-giving stimulus deflation would surely have its way altogether.

The long-term deflationary cycle has both a malevolent and a benevolent aspect. The negative attributes of this cycle are well chronicled and have been witnessed in recent years. The most obvious manifestation of this deflationary cycle was seen in the throes of the credit crisis of 2007-2009. The painfully slow nature of the job market recovery since then is a lingering reminder that deflation’s work is not yet done.

Yet deflation can also be quite beneficial for consumers if allowed to take its course. In Japan deflation was a huge benefit to the country’s aging population for some 20 years as low consumer prices helped the elderly and underemployed get by during times when the economy was sluggish. With the advent of Abenomics, Japan is finally starting to see signs of inflation after more than 20 years of falling prices. Just as Japan was the first major nation to feel the effects of the long-term deflationary cycle, it’s also first to emerge from the long-wave deflationary winter. What is now happening to Japan is instructive, for it will also happen to the U.S. once the cycle has bottomed next year.

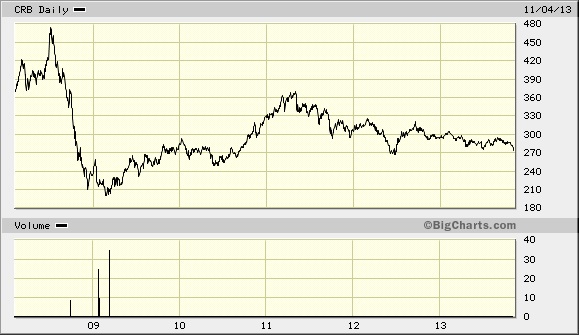

Stock prices have greatly benefited from the Fed’s asset purchases and low interest rate policy. They’ve also benefited from the low commodity prices of the last couple of years, as can be seen in the CRB commodity index shown below, since profit margins are higher when input costs are lower. There’s a possibility the stock market can dodge the proverbial bullet next year as the long-term cycle makes its final descent, thereby resulting in a mild bottom. If this happens, however, the danger to the economy will be acute in the years immediately following 2014.

By refusing to let prices fall continuously since 2008, the Fed’s intervention has artificially boosted retail prices to an extent that the next inflationary long-term cycle that begins in late 2014/early 2015 could easily create runaway inflation. That is, prices and interest rates could go through the roof once the new cycle kicks into high gear. This is where Japan’s experience will be most instructive.

Another thing to watch for as we enter the final months of the cycle is China. Note that China’s stock market, as reflected in the Shanghai Composite Index (below), has been in a downward trend since 2009. China’s economy has also been showing signs of weakness at various times in the past two years. A truism of the 60-year cycle is that the bottom must manifest somewhere. If it doesn’t produce severe effects in the U.S. next year, it will surely do significant damage to another area of the globe. The most likely candidate is China.

With China’s government significantly curtailing real estate growth over the past year, the risk of an economic crisis will increase with the added pressures of the deflationary cycle bottom in 2014. China is another problem area to watch as we enter the final months of the cycle.

********

High Probability Relative Strength Trading

Traders often ask what is the single best strategy to use for selecting stocks in bull and bear markets? Hands down, the best all-around strategy is a relative strength approach. With relative strength you can be assured that you’re buying (or selling, depending on the market climate) the stocks that insiders are trading in. The powerful tool of relative strength allows you to see which stocks and ETFs the “smart money” pros are buying and selling before they make their next major move.

Find out how to incorporate a relative strength strategy in your trading system in my latest book, High Probability Relative Strength Analysis. In it you’ll discover the best way to identify relative strength and profit from it while avoiding the volatility that comes with other systems of stock picking. Relative strength is probably the single most important, yet widely overlooked, strategies on Wall Street. This book explains to you in easy-to-understand terms all you need to know about it. The book is now available for sale at:

http://www.clifdroke.com/books/hprstrading.html

Order today to receive your autographed copy along with a free booklet on the best strategies for momentum trading. Also receive a FREE 1-month trial subscription to the Momentum Strategies Report newsletter.

Clif Droke is the editor of the three times weekly Momentum Strategies Report newsletter, published since 1997, which covers U.S. equity markets and various stock sectors, natural resources, money supply and bank credit trends, the dollar and the U.S. economy. The forecasts are made using a unique proprietary blend of analytical methods involving cycles, internal momentum and moving average systems, as well as investor sentiment. He is also the author of numerous books, including most recently “High Probability Relative Strength Trading.” For more information visit www.clifdroke.com

share

share

share

share

share

More from Silver Phoenix 500