5 Things To Ponder…To QE Or Not To QE

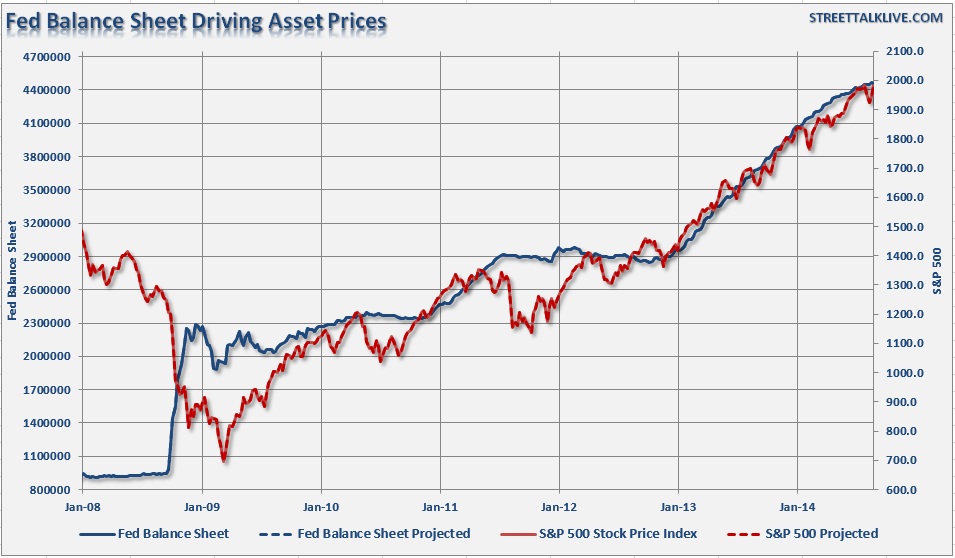

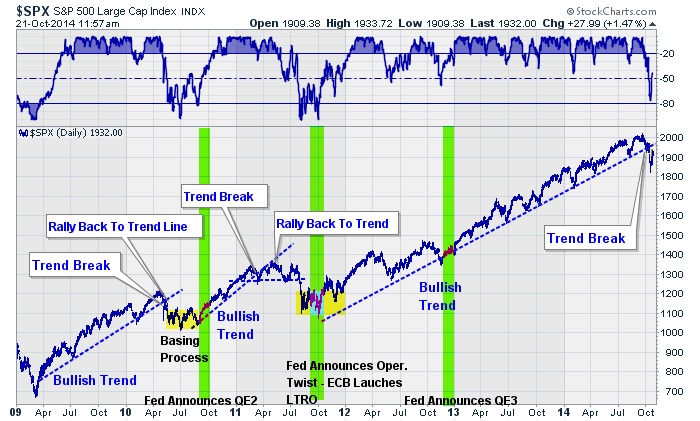

Over the last few weeks, the markets have seen wild vacillations as stocks plunged and then surged on a massive short-squeeze in the most beaten up sectors of energy and small-mid capitalization companies. While "Ebola" fears filled mainstream headlines the other driver behind the sell-off, and then marked recovery, was a variety of rhetoric surrounding the last vestiges of the current quantitative easing program by the Fed. As I have shown many times in the past, there is a high degree of correlation between the Fed's liquidity programs and the advance in the markets.

This weekend's reading list is a compilation of views on whether the Fed will end the current QE program at this week’s FOMC meeting or not. In the past, the extraction of their monetary interventions has led to market declines that were halted only once a new program was started. Are the markets, and the economy, finally strong enough to stand on their own? Or, will the end of the current QE program be the start of a bigger correction?

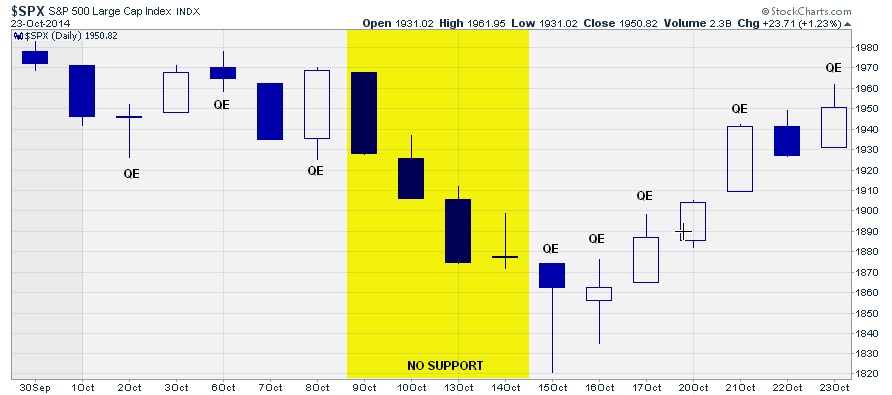

Here is something to consider if you believe that the Fed will end their monetary purchases next week. The chart below shows the recent sell-off and rebound matched to the Fed's current monetary interventions.

What will happen when the Fed is absent altogether with just one round of purchases to go? ($1 billion on Monday)

1) Fed Official: End QE On Schedule by Robin Harding via Financial Times

"The comments by Mr Rosengren, an advocate for strong monetary stimulus in recent years, suggest there is limited support for a plan put forward by James Bullard, president of the St Louis Fed, to keep buying assets at a pace of $15bn a month until December.

Mr Rosengren said Fed asset purchases have achieved their stated goal, the jobs report for September is already in and his economic forecasts have not changed. 'There has been substantial improvement in labour markets,' he said. 'As a result I would be pretty comfortable [ending purchases] at the end of the month.'”

[Note: I wonder if the 94 million considered "not in labor force," the 34% out of work longer than 6-months, or the 49 million dealing with food insecurity would agree with Mr. Rosengren?]

Also Read: Fed Official Bullard Says Keep QE Alive by Robin Harding via Financial Times

Also Read: Fed Official Fisher: Correction Possible But QE End Needed by Matthew Belvedere via CNBC

2) The Fed Shouldn't End Its Stimulus Program Yet by Danny Vinik via New Republic

"Should QE end next Wednesday? That depends. The economy really has improved over the past year, so it makes sense for the Fed to adopt a more normal policy posture. At the same time, the economy is still far from full employment and wage growth is barely keeping up with inflation. Meanwhile, the outlook for the global economy worsened over the past month, with growth slowing in China, Japan and the Eurozone. Investors are worried that policymakers, particularly the European Central Bank, will not act aggressively if the economy slows down. Economists are also unsure how the Ebola outbreak could affect the economy."

Also Read: The Statistical Recovery Continues via Streettalklive

Also Read: Bond Market Braced For End To QE by Colleen Godo via Business Day

3) All The Markets Need Is $200 Billion A Quarter From Central Banks by Simon Kennedy via Bloomberg

"By estimating that zero stimulus would be consistent with a 10 percent quarterly drop in equities, they calculate it takes around $200 billion from central banks each quarter to keep markets from selling off.

Bank of America Merrill Lynch strategists said in a report today that another 10 percent decline in U.S. stocks might spark speculation of a fourth round of quantitative easing from the Fed. That would mimic how the Fed acted following equity declines of 11 percent in 2010 and 16 percent in 2011.

'With central banks much more concerned about a return to recession than about asset-price bubbles, they have little choice but to step back in,' said Citigroup."

4) How QE Contributed To The Nations Inequality Problem by William Cohan via NYT

"[Yellen] did a wonderful job highlighting the growing disparity between rich and poor and how it is beginning to impinge upon what it means to be an American, but she ignored the fact that, in many ways, the Fed’s policies have compounded the problem.

Quantitative easing adds to the problem of income inequality by making the rich richer and the poor poorer. By intentionally driving down interest rates to low levels, it allows people who can get access to cheap money on a regular basis to benefit in extraordinary ways."

Also Read: Let Them Eat Cake via ECRI

5) World Economy So Damaged It May Need Permanent QE by Ambrose Evans-Pritchard via The Telegraph

"We will find out soon whether or not this a replay of 1937 when the authorities drained stimulus too early, and set off the second leg of the Great Depression.

Crashes are another story. They signal global stress, doubly dangerous today because the whole industrial world is one shock away from a deflation trap, a psychological threshold where we batten down the hatches and wait for cheaper prices. That is the Ninth Circle of Hell in economics. Lasciate Ogni Speranza."

Also Read: "Plunge Protection Team" Behind Market's Sudden Recovery by John Crudele via NY Post

Bonus Read: The Fed's Bubble: "Overtrading" and "Discredit" Always End In Revulsion by Van Hoisington/Lacy Hunt via ZeroHedge

"In their 2014 book House of Debt. Chapter 8, entitled 'Debt and Bubbles,' Mian and Sufi demonstrate that increasing the flow of credit is extremely counterproductive when the fundamental problem is too much debt, and excessive debt can fuel asset bubbles.

Based on our reading of these two books we would define an asset bubble as a rise in prices that is caused by excess central bank liquidity rather than economic fundamentals. As Kindleberger clearly stated, the process of excess liquidity fueling higher prices in the face of faltering fundamentals can run for a long time, a phase Kindleberger called 'overtrading.' But eventually, this gives way to 'discredit', when the discerning few see the discrepancy between prices and fundamentals. Eventually, discredit yields to 'revulsion', when the crowd understands the imbalance, and markets correct."

********

Courtesy of http://streettalklive.com/

More from Silver Phoenix 500