April CPI: Worst Good News Ever

share

share

share

share

share

share

share

share

share

share

The monthly rise in prices based on the Consumer Price Index (CPI) came in slightly lower than projected, sending a wave of euphoria across the financial landscape.

The consensus is cooling inflation puts Federal Reserve interest rate cuts back on the table.

The Dow Jones, S&P 500, and the NASDAQ all hit record highs after the data came out on Wednesday. A CNN headline called the CPI report “encouraging” and an analyst from CIBC Private Wealth US told CNN the data “supports a Fed rate cut in the fall.” Yahoo Finance called it a “soft reading on consumer prices.”

It was great news, except it wasn’t.

When you look at the data objectively and in a broader context, it becomes clear the price inflation dragon the Federal Reserve and the U.S. government unleashed during the pandemic is alive and well. He might be resting, but he certainly isn’t dead.

The CPI Numbers

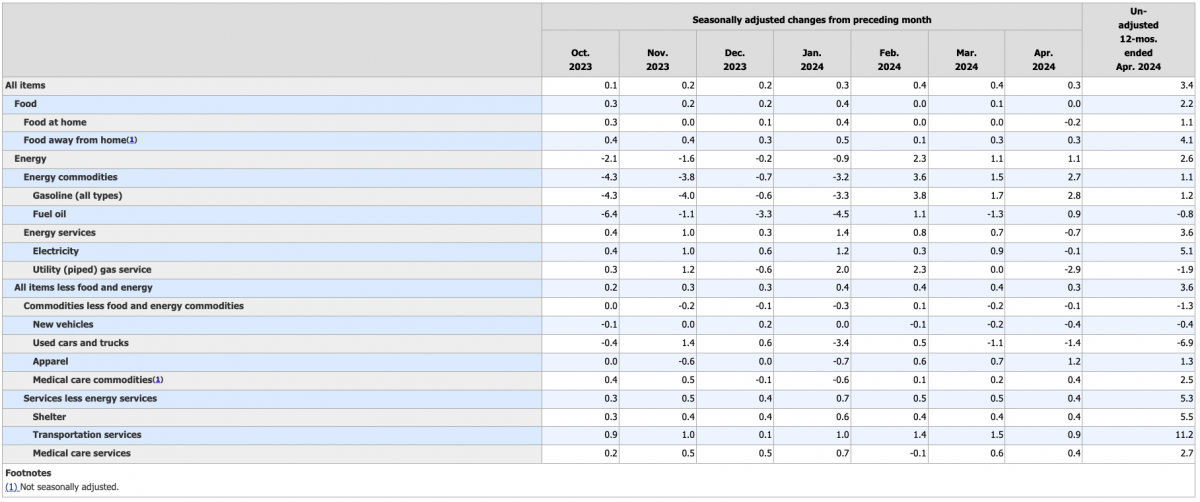

On an annual basis, prices rose 3.4 percent in April according to the Bureau of Labor Statistics (BLS) data. That was down just a tick from the 3.5 percent reading last month and met expectations. To put it in a little broader context, the annual CPI print was 3.2 percent in February and 3.1 percent in November.

On a monthly basis, prices rose 0.3 percent. That was below the expectation of a 0.4 percent monthly increase and the primary source of the euphoria. But annualizing that monthly number gives you an annual price inflation rate of 3.6 percent, nowhere near the Fed’s mythical 2 percent target.

Prices have gone up 1.6 percent in the last five months alone, hardly a cause for celebration for those of us who have to pay those prices.

Excluding more volatile food and energy prices (as if anybody can exclude such things from their budgets) core CPI was up 0.3 percent in April, down a tick from the 0.4 percent read in February and March.

On an annual basis, core CPI was 3.6 percent.

Looking at the core CPI data over the last six months provides more context. It came in a 0.2 percent in October, 0.3 percent in November and December, 0.4 percent in January and February, and 0.3 percent in March. In fact, core CPI has been mired in this range since last July.

It’s important to note that none of these numbers are close to the Federal Reserve’s mythical 2 percent price inflation target. You can argue that the April numbers show a hint of cooling, but we’ve seen that before. Everybody was convinced prices were falling and inflation was beat late last summer.

Meanwhile, producer prices rose 0.5 percent in April, with prices for final demand services increasing by 0.6 percent and the index for final demand goods up 0.4 percent.

Producer prices are generally a leading indicator of price inflation because producers pass at least some of their rising costs on to consumers.

When you put all of the data in context and look at it with an objective eye, it's pretty clear that price inflation remains sticky.

And keep in mind, inflation is worse than the government data suggest. The government revised the CPI formula in the 1990s so that it understates the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers. So, if the BLS was using the old formula, we’re looking at CPI closer to 6 percent. And using an honest formula, it would probably be worse than that.

Digging deeper into the numbers, we find that rapidly new and used vehicle prices helped pull overall CPI lower. Used car and truck costs fell by 1.4 percent month on month. New car prices dropped by 0.4 percent.

Meanwhile, clothing costs spiked by 1.2 percent, service prices were up 0.4 percent, energy prices rose with gasoline up 2.7 percent, and shelter costs continued to climb at a 0.4 percent rate.

While prices continue to rise, workers are falling further behind. Average earnings fell 0.2 percent on the month as wages failed to keep up with rising prices.

It’s fair to speculate car prices are falling because people can’t afford to buy a vehicle with other prices still climbing quickly.

Put in context, the CPI report provided very little good news for people struggling with rising prices. The only real positive is that the monthly rise wasn’t quite as bad as expected, and we finally got an overall CPI report that wasn’t worse than projected.

Everybody is Desperate for Interest Rate Cuts

The mainstream seems to be reading the April CPI data through the lens of wishful thinking. That’s because everybody is desperate for rate cuts. That includes the central bankers at the Federal Reserve.

Everybody knows that this economy can’t function long-term in a higher interest rate environment. The economy is loaded up with debt and higher interest rates are a giant anchor.

Just look at the rising interest expense on the national debt.

Uncle Sam has shelled out $624.5 billion on interest payments so far in fiscal 2024. That's a 35.7 percent increase over the same period in fiscal 2023. The federal government spent more on interest payments than it did on national defense or Medicare. The only category with higher spending was Social Security.

Debt service costs in the corporate and consumer sectors look equally problematic.

Despite talks of rate cuts, the Federal Reserve hasn't done enough to slay the inflation monster it unleashed over the last decade-plus. It is alive and well because the Fed was never fully committed to killing it.

If the central bank was truly all-in on driving price inflation back to 2 percent, we’d be hearing about additional rate hikes - not pending rate cuts.

Make no mistake; 5.5 percent interest rates are high for an economy loaded up with debt. But they aren’t high in the face of a 6 percent-plus CPI (using the more honest 1970s formula).

Keep in mind that the Federal Reserve injected nearly $5 trillion of money created out of thin air during the pandemic. The U.S. government took a lot of that money in the form of “stimulus” and showered it on Americans who weren’t producing anything. That is the source of these rising prices. A few rate hikes and a modest reduction in the balance sheet weren’t nearly enough to unwind that massive monetary malfeasance – on top of the trillions in inflation they created during the Great Recession.

Nevertheless, mainstream optimism about rate cuts this fall isn’t entirely misplaced. The central bankers at the Fed will likely take any opening they can to move forward with cuts. This CPI report, along with retail sales data showing spending slowing could crack the door open enough to let them wiggle through even though price inflation clearly isn’t dead and buried.

Consider this: if the Fed is willing to consider rate cuts now, with inflation still sticky, what will the central bankers do when something breaks in the economy?

And it’s important to remember what rate cuts mean. It is a pivot back to inflationary policies that got us here in the first place.

In other words, the eulogy for inflation is premature.

*********

share

share

share

share

share

More from Silver Phoenix 500