Behold The Power Of Buybacks And Dividends

Buybacks and dividends. The mere mention of either one is often enough to make some investors’ hearts race with excitement and embolden them with confidence that company management is being better stewards of capital.

Buybacks and dividends. The mere mention of either one is often enough to make some investors’ hearts race with excitement and embolden them with confidence that company management is being better stewards of capital.

Last week I discussed the importance of core investments, focusing on debt securities such as U.S. Treasuries and quality municipal bonds. Because most economists expect the Federal Reserve to raise interest rates later this year, it might be prudent for investors to stick with short-term, quality munis right now, as they’re less sensitive to rate increases than longer-term bonds.

But just as important to building a strong portfolio are investments in companies that return capital to shareholders in the form of dividends and repurchases of shares. This is one of the ways, in fact, that we screen companies for inclusion in our All American Equity Fund (GBTFX).

$1.2 Trillion in Buybacks

Why should you care about buybacks? There are a few answers to this question, but typically a company will initiate a buyback program when its management team believes that the stock is undervalued. This suggests that the company has a lot of confidence in its own future and could signal that strong growth is ahead.

Some effects and possible ramifications of buybacks are higher earnings per share, higher stock price and lower volatility.

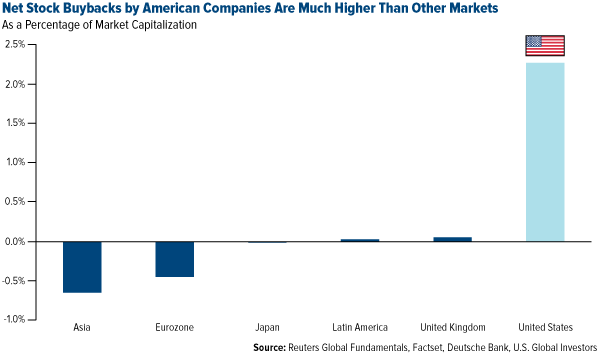

When it comes to stock buybacks, no other world market right now beats the U.S. If we look at net buybacks, which is the difference between issuances and buybacks, American companies are clearly in the lead, repurchasing over 2 percent of market cap.

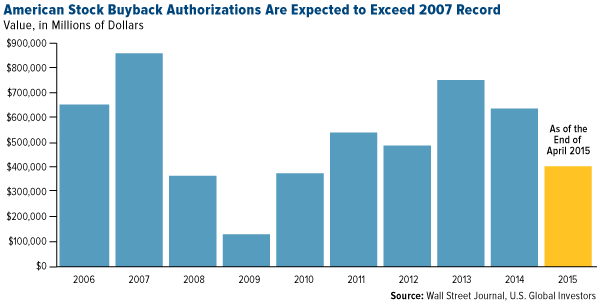

In April, a staggering $141 billion in buybacks were authorized—the most ever in a single month and an increase of 121 percent from April 2014. If this pace keeps up, a record $1.2 trillion in buybacks could be reached by year’s end, crushing the all-time high of $863 billion set in 2007.

Leading the way is Apple, held in our All American Equity Fund and Holmes Macro Trends Fund (MEGAX). Between August 2012 and March 2015, the tech giant repurchased $80 billion of its own shares.

As for dividends, Apple has paid out $2.8 billion in each of the last four quarters, for a total of over $11 billion.

As for dividends, Apple has paid out $2.8 billion in each of the last four quarters, for a total of over $11 billion.

Dividends per Share at Stunning Double-Digit Growth Rates—Government Bonds at Unattractive Yields

Goldman Sachs recently estimated that dividend yield will be the single largest contributor to total returns by the end of this year.

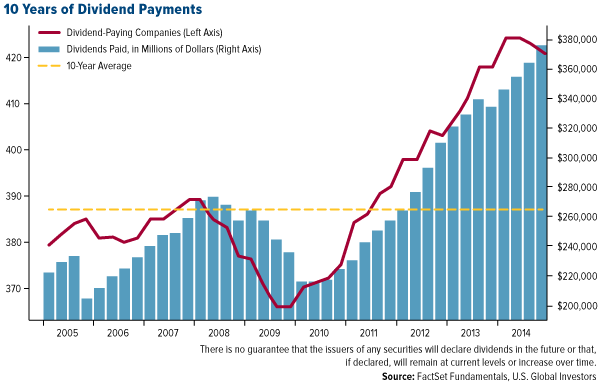

It’s easy to see why, judging from the sheer number of companies that offer a dividend now. Apple is joined by 420 others in the S&P 500 Index that similarly reward shareholders. That calculates to an impressive 84-percent participation rate.

For the last 16 quarters, dividends per share rose at double-digit rates, and each of the last four quarters gave us a new record high in payment amounts.

Earlier in the month I shared the fact that dividends had a 15 percent year-over-year growth rate in the first quarter. Looking ahead, dividends per share are expected to increase an additional 8.2 percent over the 12 months starting March 2015.

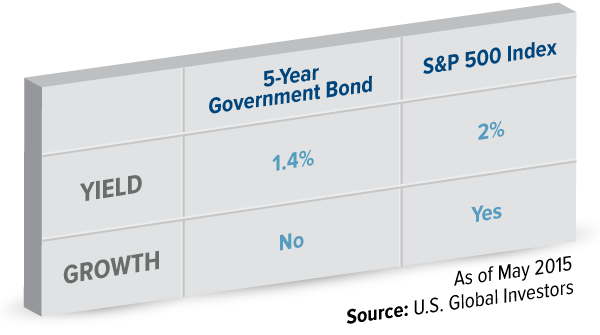

Compare these attractive figures to the five-year government bond. Not only is the yield lower than that of S&P 500 companies as a whole, but the five-year doesn’t provide any growth. Stocks and Treasury bonds do have some obvious differences, though, including investment objectives, costs and expenses, liquidity and safety.

All of the companies in our All American Equity Fund either pay a dividend or buy back their stock. Those that currently have the highest yield are integrated energy company Entergy (5.12 percent), AT&T (5.44 percent) and communications provider CenturyLink (6.5 percent). The three also have stock buyback programs.

Airlines Top the List of Bargain Stocks

Investors might point out that the domestic equities market is expensive right now. Historically, it is. The S&P 500 is trading at 18.6 times earnings.

But there are still many can’t-miss deals out there. Barron’s recently published its annual list of the 500 cheapest domestic stocks, which in the past have demonstrated better-than-average growth. In 2014, for instance, the 20 cheapest stocks on the list rose a combined 20.7 percent, beating the 12.6 percent the S&P companies as a whole delivered.

This year, American Airlines and United Continental top the list of cheap stocks, the former trading at 5.1 times estimated earnings, the latter at 5.7. Also appearing in the top 20 are Prudential Financial, MetLife, Hewlett-Packard and Valero—all vastly cheaper than the S&P 500, and all held in our All American Equity Fund.

Buying the Dip

Too often we see that investors buy into a stock or industry too late in a bull market, after much of the gains have already been made.

We saw this very thing happen when the Shanghai Composite Index tumbled 6.5 percent last Thursday, the most significant correction since January. The index has been on a tear for the 12-month period, returning over 125 percent. But between Wednesday the week before last and Wednesday last week—just one day before the correction—approximately $4.6 billion in emerging market funds around the globe were moved into China A-Shares. It was the largest weekly inflow since 2005.

We noted the Shanghai Composite bull market last September and were early participants in the rally through our exposure to China A-Shares. We also accumulated on the dip as we expect the index to move higher.

“It’s very important to know the rhythm of a bull market—slow rise, sharp correction, slow rise, sharp correction,” says Xian Liang, portfolio manager of our China Region Fund (USCOX). “In fact, one should be concerned if the market doesn’t correct because too much froth builds up in the near-term.”

Losing your confidence is one of the worst things that can happen when investing. We maintain our confidence by seeking companies that reward shareholders through stock buybacks and dividend payments and that trade at discounted rates.

********

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Past performance does not guarantee future results.

Stock markets can be volatile and share prices can fluctuate in response to sector-related and other risks as described in the fund prospectus.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Shanghai Stock Exchange Composite Index is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. Note that stocks and Treasury bonds differ in investment objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, and tax features.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the All American Equity Fund, Holmes Macro Trends Fund and China Region Fund as a percentage of net assets as of 3/31/2015: Apple Inc. 4.03% in All American Equity Fund, 5.34% in Holmes Macro Trends Fund; AT&T Inc. 1.09% in All American Equity Fund; Entergy Corp. 1.04% in All American Equity Fund; CenturyLink Inc. 1.01% in All American Equity Fund; American Airlines Inc. 0.00%; United Continental Holdings Inc. 0.00%; Prudential Financial Inc. 1.11% in All American Equity Fund; MetLife Inc. 1.17% in All American Equity Fund; Hewlett-Packard Co. 0.81% in All American Equity Fund; Valero Energy Corp. 1.50% in All American Equity Fund.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

More from Silver Phoenix 500