Billions And Billions Pour Into India And China

It’s been a little over a year since Narendra Modi took office in India, and so far the results have been mostly positive for the South Asian country and the surrounding region. Among other achievements, Modi’s government has managed to enact important policy reforms, increase public investments in infrastructure, lower food inflation and generally open India up to business on a global scale.

It’s been a little over a year since Narendra Modi took office in India, and so far the results have been mostly positive for the South Asian country and the surrounding region. Among other achievements, Modi’s government has managed to enact important policy reforms, increase public investments in infrastructure, lower food inflation and generally open India up to business on a global scale.

CLSA’s chief equity strategist, Christopher Wood, gives the country accolades in his most recent newsletter. Wood writes that while “the halo effect has come off the Modi phenomenon” somewhat, India nonetheless remains “the most promising major emerging market story on a five- to 10-year view globally.”

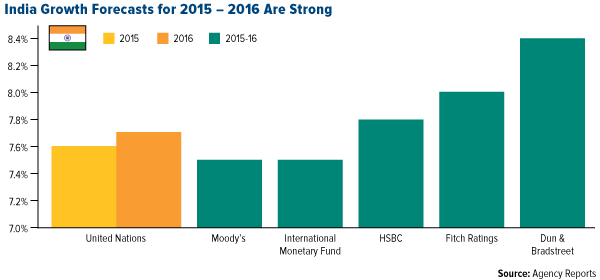

Looking ahead, analysts forecast that India’s economy will expand between 7.5 percent and 8.5 percent for the 2015 and 2016 fiscal years, faster than any other G20 nation, including China.

This is growth that can be sustained for the long-term, a topic I wrote about last October. According to the International Monetary Fund, within the next decade and a half, “India will have the largest, and among the youngest, workforces in the world, and will need to create jobs for the roughly one hundred million young Indians who will enter the job market in the coming decade.” By 2050, India is expected to be the world’s second-largest economy based on purchasing power parity, following China.

Global investors recognize these positive data points and are piling into Indian equities, especially now that aggressive monetary easing in the country seems likely. CLSA’s Wood points out that $737 million a month on average have flowed into India-focused mutual funds since Modi took office last May, a dramatic reversal from the amounts seen prior to that.

Historically Low Interest Rates Help Push Chinese Equities Higher

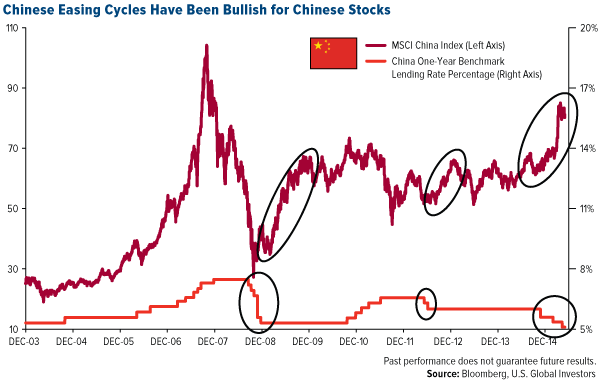

Indeed, rate cuts have been constructive for not only Indian equities but also the Chinese market. As you can see below, easing cycles have historically coincided with strong market rallies in the MSCI China Index, a proxy for China H-shares, or stocks of Chinese companies listed on foreign exchanges. H-shares are one of the principal ways our China Region Fund (USCOX) has participated in the current bull market.

After three cuts in the most recent easing cycle, Chinese rates now stand at their lowest point ever, helping the index move higher in its quest to regain its November 2007 highs.

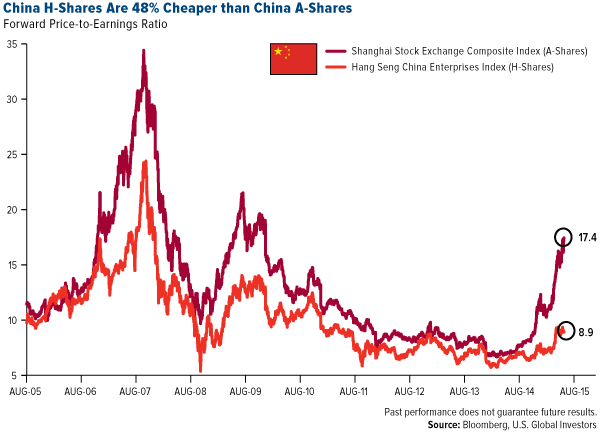

H-Shares Half as Cheap as Chinese Domestic Equities

Judging from the rally in H-shares, some investors might be concerned that the market is too expensive right now. On the contrary, H-shares, expressed below by the Hang Seng Index, are trading at a much cheaper multiple of 8.9 times estimated earnings to A-shares’ 17.4, a discount of 48 percent.

You can also see that both H-shares and A-shares have traded at much higher multiples in the past, evidence that the rally is not yet overdone.

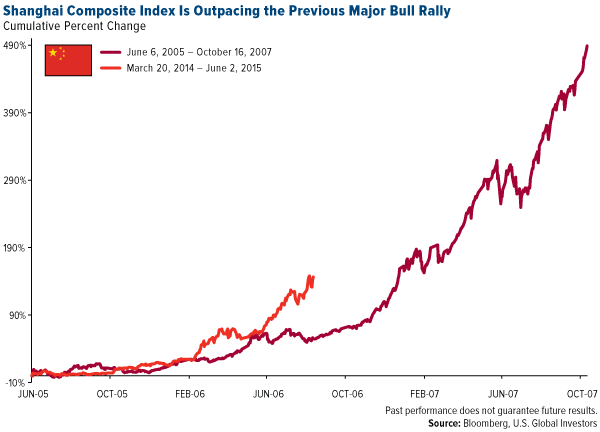

When we compare this trading cycle with the previous major rally that occurred from June 2005 to October 2007, we see that the run-up has plenty of room to climb higher.

“We might be in the middle of a bull market, not the end,” says Xian Liang, portfolio manager of USCOX.

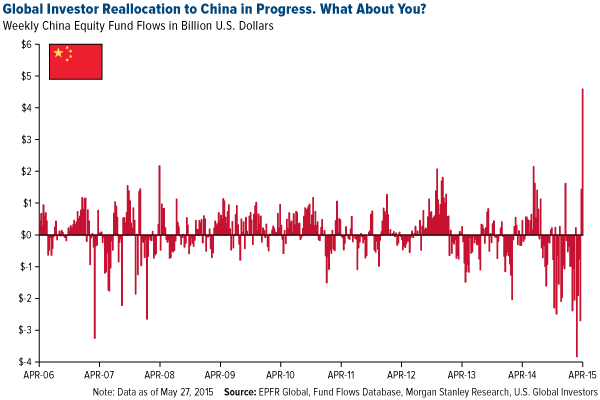

Like Indian equities, Chinese equities are attracting massive amounts of fund inflows. For the week ending May 27, global investors reallocated $4.6 billion to A-shares ahead of FTSE indexing.

Last Thursday, the Shanghai Composite Index fell 6.5 percent, probably due to profit-taking. This represented the most significant correction since January, when the Chinese government curbed margin lending. It’s important for investors to look beyond the short-term noise and recognize that any correction this cycle could be seen as an opportunity to accumulate.

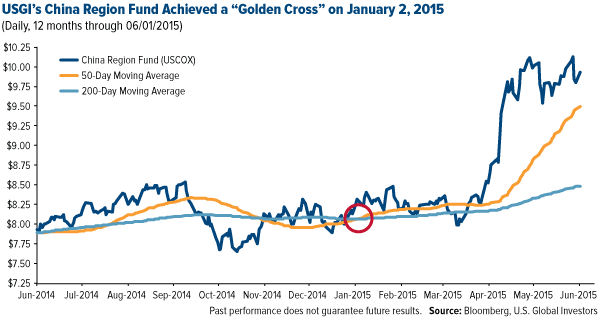

Again, USCOX continues to participate in this bull market through China H-shares and A-share exchange-traded funds. This helped the fund achieve a “golden cross” in January, which occurs when the 50-day moving average crosses above the 200-day moving average.

Such technical indicators are seen as harbingers of strong growth. This particular move shows that the Chinese market has the support it needs to maintain upward momentum.

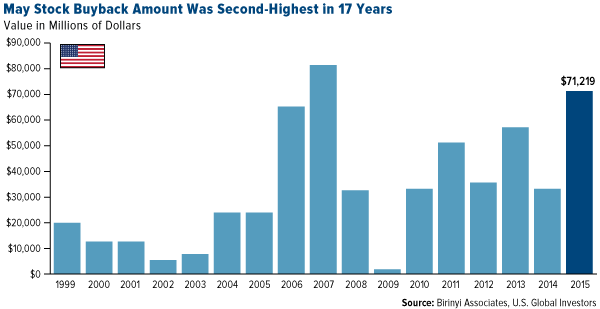

American Companies Buy Back $71 Billion of Stock in May Alone

As for American equities, they continue their trend of rewarding shareholders in the form of dividends and stock buybacks. Last week I mentioned that the amount in buybacks is expected to reach a staggering $1.2 trillion by year’s end, surpassing the all-time high of $863 billion set in 2007.

Stock market research firm Birinyi Associates reports that U.S. companies repurchased over $71 billion of shares in May alone.

This is one more compelling reason we find the domestic market so attractive, and offer investors the opportunity to participate with our All American Equity Fund (GBTFX). All of the holdings in GBTFX either pay a dividend or are currently buying back their stock.

Countless Jets Will Need to Be Replaced in the Coming Years

A final note I’d like to end on is the sheer number of jumbo jets that will need replacing in the coming years as domestic airlines seek to incorporate smaller, more efficient aircraft. Manufacturers Boeing and Airbus certainly have their work cut out for them and, in fact, face years’ worth of backlogs.

Business Insider recently shared a slideshow that reveals what happens when airlines retire older models in their fleet. Many of them end up at the Southern California Logistics Airport, where they wait to be resold, dismantled or put back into commission. You can view the slideshow here.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Past performance does not guarantee future results.

Total Annualized Returns as of 3/31/2015

|

|

One-Year |

Five-Year |

Ten-Year |

Gross Expense Ratio |

Expense Cap |

|

China Region Fund |

6.63% |

0.52% |

5.14% |

2.97% |

2.55% |

Expense ratios as stated in the most recent prospectus. The expense cap is a voluntary limit on total fund operating expenses (exclusive of any acquired fund fees and expenses, performance fees, extraordinary expenses, taxes, brokerage commissions and interest) that U.S. Global Investors, Inc. can modify or terminate at any time, which may lower a fund’s yield or return. Performance data quoted above is historical. Past performance is no guarantee of future results. Results reflect the reinvestment of dividends and other earnings. For a portion of periods, the fund had expense limitations, without which returns would have been lower. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance does not include the effect of any direct fees described in the fund’s prospectus (e.g., short-term trading fees of 0.05%) which, if applicable, would lower your total returns. Performance quoted for periods of one year or less is cumulative and not annualized. Obtain performance data current to the most recent month-end at www.usfunds.com or 1-800-US-FUNDS.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio.

Stock markets can be volatile and share prices can fluctuate in response to sector-related and other risks as described in the fund prospectus.

The MSCI China Free Index is a capitalization weighted index that monitors the performance of stocks from the country of China. The Hang Seng Index is a capitalization-weighted index of 33 companies that represent approximately 70 percent of the total market capitalization of The Stock Exchange of Hong Kong. The Shanghai Stock Exchange Composite Index is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the China Region Fund and All American Equity Fund as a percentage of net assets as of 3/31/2015: The Boeing Co. 0.00%, Airbus Group SE 0.00%.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.