The Causes Of Greece’s Crisis

How did the misconstruction of the Eurozone cause the Greece’s debt crisis? The main reason was excessive public spending starting in the 1980s when the socialist government came to power. Since then, external borrowing was used to boost consumption. Greece has been living beyond its means, long before it joined the Eurozone.

How did the misconstruction of the Eurozone cause the Greece’s debt crisis? The main reason was excessive public spending starting in the 1980s when the socialist government came to power. Since then, external borrowing was used to boost consumption. Greece has been living beyond its means, long before it joined the Eurozone.

However, after it adopted the single currency, the public spending soared. Thanks to the flawed institutional structure of the Eurozone, Greece could externalize its reckless fiscal behavior to its neighbors as the European Central Bank accepted Greek government bonds as collateral for their lending operations, monetizing them in effect. That way, the Greek government has been bailed out by the Eurozone in a constant transfer of purchasing power.

If the Greek bonds were not accepted by the ECB as collateral for its loans (or at least if they were not treated if they were German bonds), Greece would have paid much higher interest rates for its debts, which could have forced it to conduct some structural reforms. Instead of abandoning the expansionary, pro-cyclical fiscal policy and increasing its international competitiveness, the Greek government ran fiscal deficits of 6 percent of GDP on average, increasing the share of the government spending in the economy. The government increased its spending in order to buy public support, practically nationalizing the economy as most of business contracts were in fact given by the government. According to the Kouretas’ paper, the dramatic increase in public sector employees “led to a reallocation of capital and labor away from the private sector (…) leading to the loss in competitiveness”.

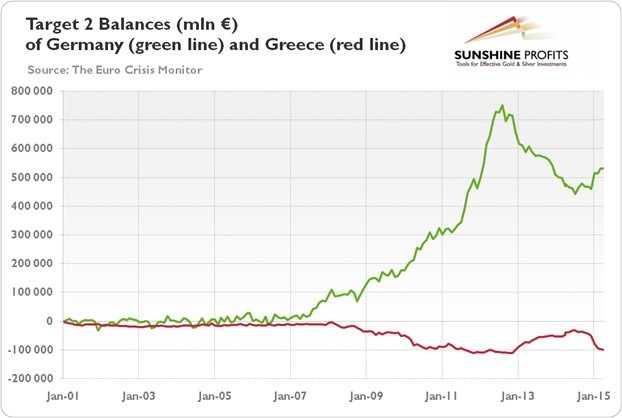

The ongoing bailout was reflected in the Target2, a joint gross clearing system of the Eurozone and the operational tool through which national central banks of Eurozone’s members provide payment and settlement services for intra-Eurozone transactions. We do not have enough space to describe its mechanism thoroughly (if you are interesting in the topic, we recommend this paper or this article), but the most important thing is that a positive Target2 balance reflects a net claim vis-à-vis the ECB and a negative balance corresponds to a net liability. As the chart no. 1 shows, the current account deficits of Greece were financed for years by refinancing credits of its national central bank and the concomitant Target credit.

Chart 1: Target2 balances (mln €) of Germany (green line) and Greece (red line) between January 2001 and April 2015.

Imports of goods (e.g., German cars) to Greece were financed by the Greek commercial banks granting loans to Greek entrepreneurs and households by increasing their refinancing with the Bank of Greece. That money creation resulted in Taget2 debits for the Bank of Greece and Target2 credits for the Bundesbank. For years, the Eurosystem encouraged Greece to finance its current account deficits and live beyond its means via money creation and without structural reforms. Thanks to this constant bailout mechanism, the country neither deregulated labor markets nor reduced government spending to adjust prices relatively, but continued its spending spree and maintained its uncompetitive internal structure.

Second important factor behind the public adventure park was the drop in the interest rates on Greek government bonds due to entering the Eurozone. The implicit bailout guarantee from the ECB and other members of the Eurozone resulted in a change of the market’s perception of the Greek sovereign debt. Seen as a safe investment, it pushed Greek yields down almost to German levels, despite the fact that the latter was more productive and much sounder fiscally. In other words, the introduction of the euro led to the reduction of the exchange-rate uncertainty and reduction of inflation expectations, which were usually high in Greece with historical high levels of inflation and lack of economic policy credibility. Consequently, the borrowing costs were reduced. Indeed, according to Kouretas’ paper, “during the period prior to the entry of Greece in the EMU the interest-rate spreads between 10-year Greek and German government bonds were reduced drastically from 1,100 basis points in early 1998 to about 100 basis points one year before the entry. Following the entry in the Eurozone the spreads fell to 50 basis points whereas during the period 2002 until the end of 2007 the spreads fell even further ranging from 10 to 30 base points.”

Additionally, Greece converted its currency into euro at a very high exchange rate. To mitigate this problem, the government increased its spending for unemployment benefits and early retirement and employed people as public workers, instead of reducing wages to increase productivity. Thanks to strong labor unions, the public sector wages rose by 50 percent between 1999 and 2007 (far faster than average in the Eurozone), while the government revenue was hit by widespread tax evasion.

Though the global financial crisis initially had little impact on Greek financial markets, the rapid worsening of the fiscal situation in Greece (in October 2009 the fiscal deficit in 2009 was revised to be 12.7 percent[later even to more than 15 percent] instead of the 6 percent forecasted by the previous government), and the sharp increase in risk aversion after Dubai World asked for a six-month debt moratorium, causing a prolonged rise in the yields on Greek bonds which continued into early 2012. According to Dellas and Tavlas, the Greek-German spread on “the 10-year sovereign widened from about 130 basis points in October 2009, to around 900 basis points one year later”, and Greece came to be frozen out of international bond markets.

The causes of the Greek sovereign debt crisis were structural and resulted from the expansionary fiscal policy conducted by the socialist governments since 1980s and misconstruction of the Eurozone and the following tragedy of the commons, which not only did not prevent, but actually encouraged imprudent fiscal policy. It should be clear that nothing will change radically under leftist Syriza. Thus, gold should see some safe-haven demand in the future. Indeed, it seems that renewed concerns on the Greek crisis support gold prices, as gold is higher in the euro and even in U.S. dollar terms this year, despite significant headwinds, like the appreciation of the greenback, surging and record-breaking stock prices, the end of the Fed’s QE and the expected interest rate hike in the U.S.

********

Would you like to understand the debt crises on global economy and gold prices expressed in different currencies? Did you like the above analysis? If so, we would like to invite you to try our services. We focus on the fundamental economic analysis in our monthly gold Market Overview reports and we provide also Gold & Silver Trading Alerts for traders interested more in the short-term prospects. We also invite you to join our gold newsletter. It’s free and you can unsubscribe in just a few clicks.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017. He is a board member of the Polish Mises Institute of Economic Education, author of several dozen scientific publications (including in such periodicals as the Journal of Risk Research, Prague Economic Papers, Quarterly Journal of Austrian Economics, and Research in Economics), and a regular contributor to GoldPriceForecast.com and SilverPriceForecast.com. His two books, Money, Inflation and Business Cycles and Monetary Policy after the Great Recession, are both published by Routledge. Arkadiusz is also a certified Investment Adviser, a long-time precious metals market enthusiast, and a free market advocate who believes in the power of peaceful and voluntary cooperation of people.

More from Silver Phoenix 500