CFTC Silver Probe: See-no-Evil, Hear-no-Evil, Speak-no-Evil

When the world’s largest commodity futures “regulator” releases the results of a five-year probe; one expects to see a detailed, thorough, and well-reasoned analysis. What we see instead is a pathetic exercise in pseudo-logic – which could have been written in its entirety in a single afternoon. “Shallow” cannot begin to describe the lack of depth in this probe.

Indeed, one would not even attempt such a vacuous non-response to the question/issue of silver manipulation unless they were absolutely certain that their findings would not be questioned in the slightest – as poking holes in this drivel is proverbial “child’s play.” Thus in releasing such a farcical probe, this directly implies a totally corrupt (Corporate) media – one which only parrots, never questions.

Fortunately the CFTC has been kind of enough to place all of its pseudo-reasoning in bullet-point form, saving readers precious minutes of their lives which they would have otherwise wasted in going through its drivel line-by-line in order to expose this Big Lie. This makes the task of analysis simple: list these bogus arguments, expose the gigantic, unstated assumption (and omitted facts) upon which these “reasons” are based – and then translate them back into the Real World.

- Silver cash and futures prices have risen dramatically between 2005 and 2007, with silver outperforming the gold, platinum and palladium markets, suggesting that silver futures prices are not depressed relative to other metals prices.

- NYMEX silver futures prices tend to track closely the price of physical silver.

- Concentration levels for the top four short futures traders in the silver market are comparable to those observed in the gold and copper futures markets, and generally are lower than the levels seen in the platinum and palladium futures markets.

- The composition of the traders comprising the top four short futures traders, in terms of net positions, change over time. These traders represent a diverse group, and their futures positions are driven by an even more diverse group of customers.

- There is no observable relationship between short-futures-trader concentration levels and silver prices.

- There is a slightly positive relationship between the total net position of the large short futures traders and silver prices; this suggests that larger short futures positions are associated with higher, not lower prices.

All of this report is totally and completely predicated upon one, single assumption, with the exception of arguments (2), (3) and (4), which (because of their specific nature) are also based upon separate, false assumptions and missing facts.

The huge assumption upon which the entire CFTC report rests is that the silver market was “normal” at the time it commenced its sham-analysis, a market with supply and demand in balance, and prices in equilibrium. We know that this is an assumption in all of the CFTC’s reasoning, because never once does it attempt to address how its analysis would differ if one did not assume a market in perfect balance.

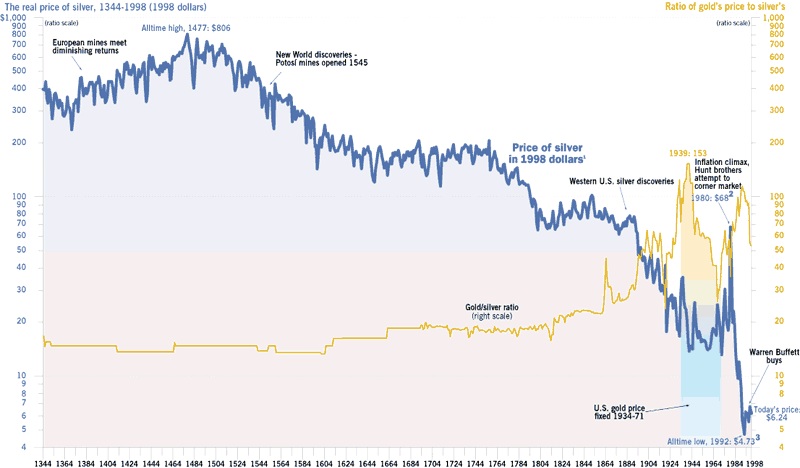

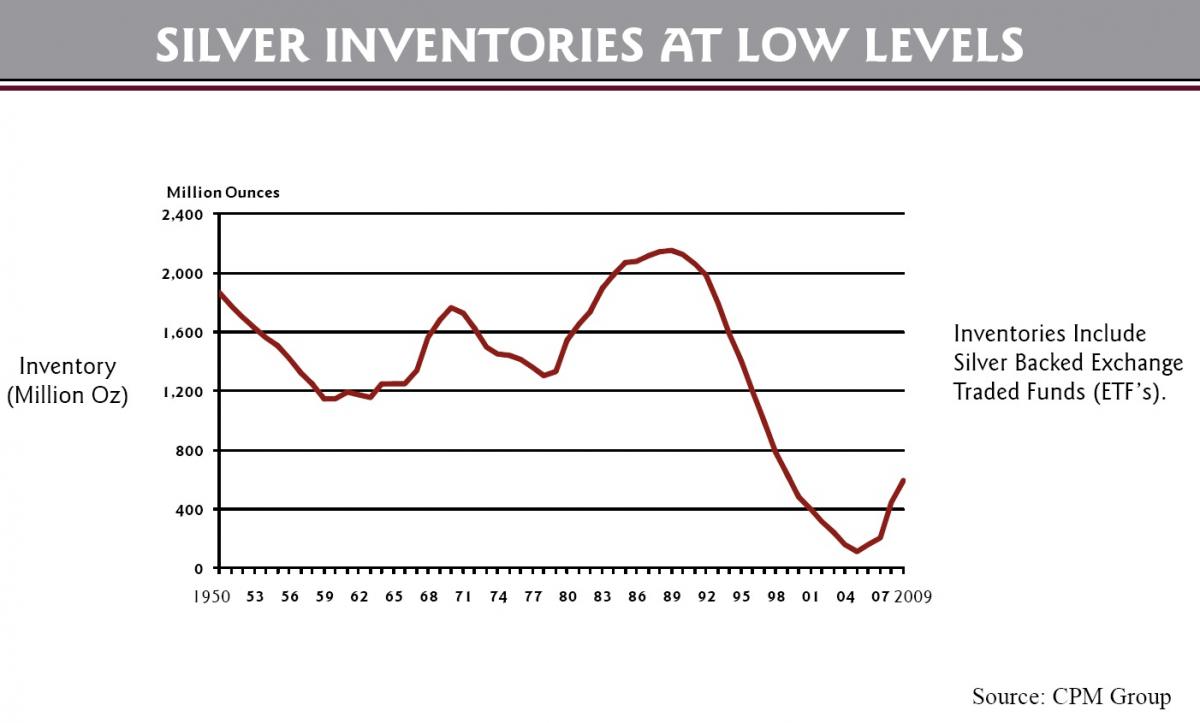

In fact, at the time the CFTC commenced its examination of the silver market; the silver market represented the most-tortured, perverted commodity market in the history of human commerce: prices near multi-century lows, inventories totally collapsed, near-complete genocide in the silver mining industry.

These fundamentals are so extreme that no “regulator” could possibly fail to be aware of them. Indeed, the CFTC deliberately, cynically chose the absolute lowest point of this multi-century silver trough as the “norm” upon which it bases its entire pseudo-analysis.

The charts below express these points in unequivocal terms:

By 2005, prices had barely crept off of the bottom of their 600-year low (in real dollars). Inventories were at an absolute low (up to that point in time), having collapsed by 90% between 1990 and 2005. Damage to the silver mining sector was at its absolute zenith: miners were still crippled by the 600-year low in price, and had not (yet) begun to benefit in any substantial way from prices creeping slightly off of that bottom.

Obviously the devastation wrought in the silver sector prior to this period of analysis could not possibly be a naturally-occurring event in any hard commodity market, as the simultaneous (and sustained) collapse in silver prices and silver inventories is an economically perverse event. Those with even the most-elementary exposure to economics understand that collapsing inventories always imply rising prices (as that good becomes “scarce”). Conversely, falling prices directly imply large and/or rising inventories – a good in “over-abundance”.

One cannot rebut the elementary principles of economics, nor overwhelming (and extreme) empirical evidence. The period prior to 2005 marked a period of sustained, obvious, ultra-extreme manipulation of the silver market, where more than 90% of all its producers were driven into bankruptcy.

Viewed from the correct perspective, it then becomes simple to boil-down this CFTC report to what it really represents: viewing the current period of extreme manipulation in the silver market through the ‘lens’ of even more-extreme past manipulation – while pretending that this more-extreme manipulation represented “normalcy”.

If someone standing under the sun in the Sahara Desert steps into the shade, they may tell you that “it’s cool in the shade.” But anyone looking at the nearest thermostat will see the objective, obvious truth. In releasing this sham-analysis, the CFTC has “proven” nothing – except that it refuses to look at the thermostat.

See no Evil, hear no Evil, speak no Evil. Viewed through the prism of reality, we can now dispense with these silly arguments, one-by-one.

- “Silver cash and futures prices have risen dramatically…” Yes, push the price of anything down to a 600-year low and it will rise dramatically. Had the price been pushed to a thousand-year low it would have risen even more dramatically – despite the extreme post-2005 manipulation of the silver market. All the CFTC has “proven” here is that no manipulation can permanently suppress the price of any physical asset.

- “NYMEX silver futures prices tend to track closely the price of physical silver.” Pure cynicism. Former Goldman Sachs banker Jeffrey Christian disclosed in testimony at a CFTC hearing that the bankers’ paper-bullion markets are (at least) one hundred times larger than the real, “physical” markets. The physical market is absolutely and totally a Hostage Market; where a fraudulently-inflated (paper) Tail flagrantly and continuously “wags” the (relatively miniscule) Dog.

o For the CFTC to pretend differently, despite its own recorded (and uncontradicted) testimony which proves that the paper market rules the physical market is “proof” of nothing except the CFTC’s own, endemic corruption. See no Evil, hear no Evil, speak no Evil.

- “Concentration levels…are lower than…in the platinum and palladium futures markets.” Laughable. This merely duplicates the false-reasoning upon which the whole report is based. The CFTC plucks out the only two commodities in the world with even more-extreme (criminal?) short-positions – and depicts them as the “norm” upon which to base comparison.

o Notably the myopic CFTC avoided comparing the “concentration” in the silver market with concentration in oil market, where (in relative terms) that concentration is less than 1/50th as large. Also notably absent from this myopic analysis is the fact that the “concentration” of these Four, Largest Traders (on the short side) averages-out to being as large as the Hunt Brothers’ long position – when they were successfully prosecuted for illegal over-concentration in the silver market (i.e. “cornering the market”).

o The implied “moral of the story” from this CFTC decision? If you have one “Hunt Brothers” on the long side it’s a crime; but if you have four “Hunt Brothers” on the short side, it’s “business as usual” – and the Criminals can continue their crimes indefinitely, unimpeded by (CFTC) “regulation”. See no evil, hear no evil, speak no evil.

- “The composition” of the Four Criminals changes over time, and they “are a diverse group”. Even more laughable.

As was explained in a recent commentary; compelling and comprehensive research by a trio of Swiss Researchers has concluded that there is, in fact, only One Bank in the world – a “super-entity” which by itself controls 40% of the global economy. The Four Criminals in the silver market are merely four tendrils of the One Bank. Claiming that the subsidiaries of this one, banking monopoly are “diverse” is more-absurd still.

These Subsidiaries are regularly caught colluding to manipulate markets; with their past-and-continuing manipulation of the $500-trillion “LIBOR”-based debt market being their largest (revealed) Crime to date. Proving the corruption of our entire (One Bank-ruled) financial system; these fraud-tainted “LIBOR” contracts continue to be enforced – in direct violation of every principle of contract law, and the Rule of Law itself.

There isn’t enough space available here to also discuss how these same banks serially collude to “launder” money from the global drug cartels (on an ongoing basis), and were recently caught colluding in gangster-like warehouse fraud (also in metals markets). See no Evil, hear no Evil, speak no Evil.

- “There is no observable relationship” between silver-shorting and silver prices. More cynicism. This merely repeats the false-logic the CFTC used in (1). All that is being “proven” here is that after driving the price of silver to a 600-year low and totally decimating global inventories that no amount of silver-shorting can prevent some level of price-correction from that ultimate extreme.

- “There is a slightly positive relationship” between silver-shorting and silver prices. Repeating this same (absurd) argument for a third time – but in a slightly different form – makes it no more rational than the first time the CFTC attempted to pass-off this nonsense.

Indeed, by repeating the same argument three times while totally ignoring all of the evidence contained in this commentary, ignoring all of the direct “smoking gun” evidence submitted to the CFTC from noted whistle-blower Andrew Maguire (and JPMorgan’s own traders), and ignoring the mountains of evidence and the decades of research from the legendary Ted Butler (also submitted); the CFTC has “proven” only one thing with this report: its own (corrupt) tunnel-vision.

See no evil, hear no evil, speak no evil.

Jeff Nielson

Jeff Nielson is co-founder and managing partner of Bullion Bulls Canada; a website which provides precious metals commentary, economic analysis, and mining information to readers/investors. Jeff originally came to the precious metals sector as an investor around the middle of last decade, but soon decided this was where he wanted to make the focus of his career. His website is www.bullionbullscanada.com.

Jeff Nielson is co-founder and managing partner of Bullion Bulls Canada; a website which provides precious metals commentary, economic analysis, and mining information to readers/investors. Jeff originally came to the precious metals sector as an investor around the middle of last decade, but soon decided this was where he wanted to make the focus of his career. His website is www.bullionbullscanada.com.

More from Silver Phoenix 500