The Credit Gradient

The United States, and every country, is subject to a monetary authority and legal tender laws. Here in the U.S. we have the Federal Reserve, a central bank that plans money and credit. The Fed thought they had perfected their planning (but of course it cannot be perfected). They thought they had ended the boom and bust cycle, and brought us into a brave new era, their so-called great moderation that ended in 2008. All they really did was manage the banking system to the brink of insolvency.

Let’s try a thought experiment. Suppose the monetary central planner attempts to fix the problem of insolvency by massive injections of liquidity. The central bank buys bonds. It dictates rates near zero on the short end of the yield curve, and promises not to raise rates for years to come. What perverse outcome would we expect?

Arbitrageurs see a green light, telling them that they can safely borrow short to buy long bonds. As the price of a bond goes up, the rate of interest goes down—it’s a rigid mathematical inverse. This is how suppression of short-term rates causes suppression of long-term rates.

This poses a problem for investors. Every investor has a minimum yield he must earn in order to meet his goals, such as retirement. When the yield available in government bonds falls, this gives the investor a strong push to other bonds with higher yields. Some Treasury bond owners sell, and go into AAA corporate bonds. This, of course, pushes up bond prices and pushes down the yield. This pushes some AAA corporate investors into AA bonds. And so on.

The net yield earned by every investor is pushed lower. However, at each step in the process, the effect is diminished. The wave of credit does not quite make it all the way to the other side of the pool, where the small businesses are trying to get wet.

In a free or semi-free market, credit is generally plentiful and inexpensive for mature, large enterprises. When well managed, these companies offer a low credit risk. Conversely, it has always been difficult for startups to obtain credit. When they can get it, they have to pay dearly. In other words, there is a credit gradient.

A gradient describes a change in concentration of something as you move through a range of coordinates. For example, this is a color gradient.

Of course, there is always a credit gradient. Only now, the Federal Reserve has exaggerated it to an extreme. They have made the gradient steeper.

The biggest players are drunk, chugging as much as they want. At the same time, the scrappy disruptors with the greatest opportunities to improve our world are more dehydrated than ever. Worse yet, the innovators have to try to compete for resources with the large corporations.

The credit gradient is artificially enhanced. The end result is not surprising.

I came across this paper, by the Brookings Institute. Authors Ian Hathaway and Robert Litan found that “Like the population, the business sector of the U.S. economy is aging. … The share of firms aged 16 years or more was 23 percent in 1992, but leaped to 34 percent by 2011—an increase of 50 percent in two decades.”

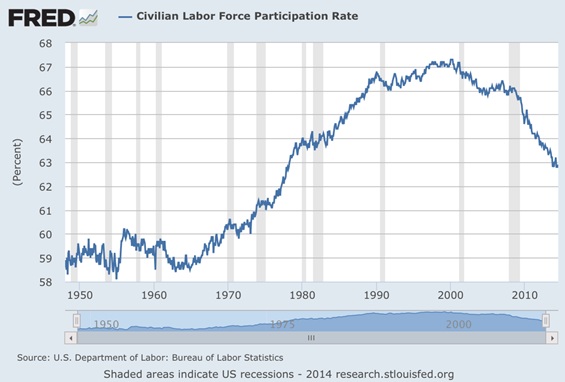

Entrepreneurial young companies are not hiring, or in many cases, surviving. The older, larger ones are all that remain. Their hiring is anemic compared to that of younger companies. The proof is in the labor force participation rate, which shows the percentage of working age people who are employed or seeking employment. It is now down to a level last seen during the Carter Administration in the late 1970’s.

Although there are other factors that contribute to this dismal reality including minimum wage and labor law, taxes, environmentalism, subsidies for crony companies, and regulations, the artificially enhanced credit gradient deserves the lion’s share of the blame.

********

© 2013 Monetary Metals

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.