The Destruction Of The Euro

The Eurozone is bust. The deterioration of TARGET2 imbalances have been hardly noticed, but in recent months it has been alarming. Despite official denials over the years that it is a matter of concern, it is increasingly obvious that the national banks of Italy, Spain and other nations with increasing bad debts are hiding them within the TARGET2 system. The first wave of Covid-19, which is leading to bankruptcies throughout the Eurozone, is now being followed by a second wave, which will almost certainly take out a number of important banks, in which case the cross-border euro system will implode.

Introduction

If ever there was a political construct the unstated objective of which is to enslave its population, it is the European Union. Its opportunity stems from national governments which, with the exception of Germany and a few other northern states, had driven or were on the way to driving their failed states into the ground. The EU’s objectives were to support the policies of failure by corralling the accumulated wealth of the more successful nations to fund the failures in a socialistic doubling-down, and to accelerate the policies of failure to ensure that all power resides in the hands of statist looters in Brussels.

It is Ayn Rand’s vision of the socialising state as looter in action. All of surviving big business is aligned with it: those who refused to play the game have disappeared. Senior executives with extensive lobbying budgets are no longer at the beck and call of contentious consumers and have hollowed out their smaller competitors. They have opted for the easier non-contentious life of seeking favours of the looters in Brussels, enjoying the champagne and foie gras, the partying with the movers and shakers, and the protection they bribe for their businesses.

It is a corrupt super-state that evolved out of American post-war policy — the child of the American Committee of United Europe. Funded and staffed by the CIA in 1948, the committee’s objectives were to ensure the European countries bought into a US-controlled NATO, in the name of stopping Stalin’s westwards expansion from the post-war boundaries. This was the official story, but it is notable how it formed a template for subsequent American control of other foreign states. It is the action of the jewel wasp that turns a cockroach into a zombie, so that its lava can subsequently feed off it.

This European cockroach is now in the final stages of its zombified existence. In Brussels they don’t realise it, but they are partying into the dawn of the next world, and they will have nowhere left to go. Outside of the Brussels hothouse and EU capitals it is hard to discern any support for a failing political system, beyond simply keeping the show on the road. The German population grumbles about lending their money to economic failures, but like any creditor deep in the hole they will remain blind to the deeper systemic problem for fear of its collapse. At the other extreme are the Greek socialists who claim Germany still owes them for their brutality and destruction seventy-five years ago. It is a Faustian pact between creditors and debtors to ignore the reality of their respective positions. It is the method of imperialism; but instead of being applied to other nations, Brussels applies imperial suppression to its own member states. And now that they been hollowed out, there is nothing left to sustain Brussels.

This is the destination they have arrived at today. Brussels and its European Parliament are nearing the end of their ridiculously expensive and pointless pig-on-pork socialising destruction. Not only have the panjandrums no one left to rob, nowhere left to go, but they have bankrupted a whole continent. Surely, the robbing of the rich and giving to the poor is close to its end. The creditors and debtors have nothing material left — money in everyone’s balance sheet will be written off through a monetary and economic collapse. It is the process of it and the destination we must analyse.

The Eurozone’s banking system is a heartbeat from collapse, as will become evident in this article. There are two basic elements involved. At the bottom there are the commercial banks with rapidly escalating non-performing loans, a phrase which hides the truth, that they are irretrievable bad debts. At the top is the Eurozone-wide settlement system, TARGET2, which is increasingly used to hide the bad debts accumulating at national levels.

Before we look at the position of the commercial banks, in order to understand how toxic the Eurozone has become we will start by exposing the dangers hidden in the settlement system.

TARGET2 — chickens are coming home to roost

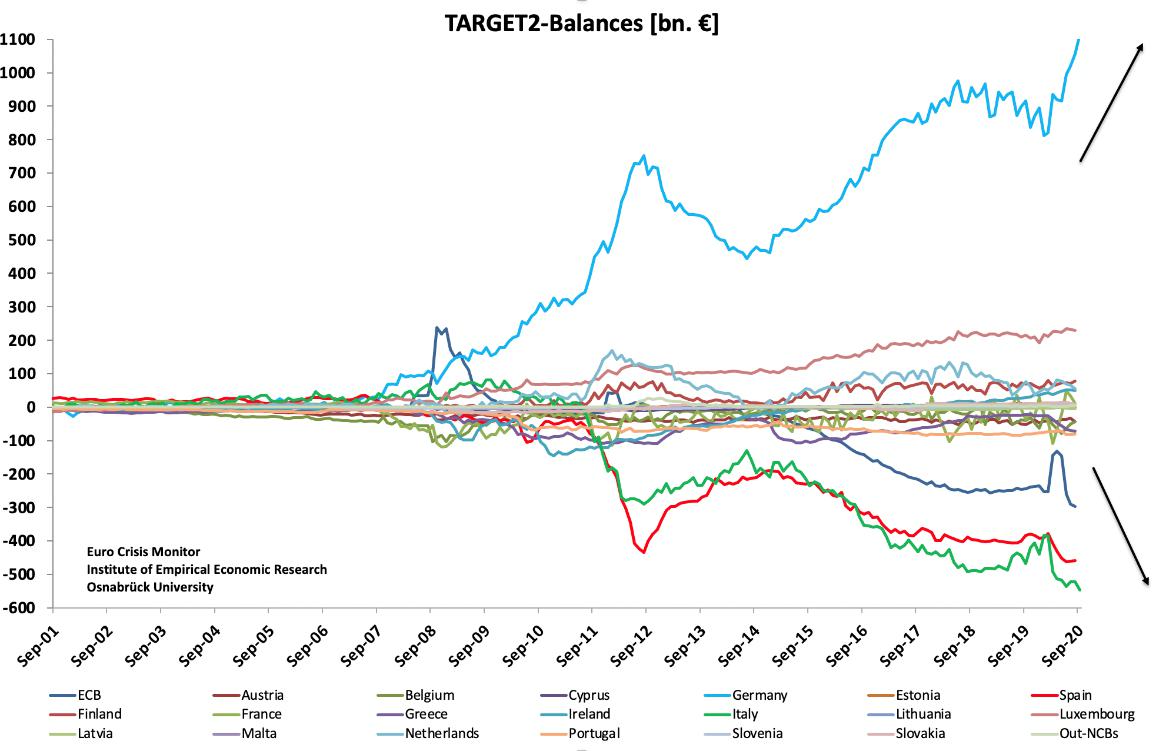

The imbalances between the ECB and the national central banks in the TARGET2 Eurozone settlement system are indicative of the current situation.

Germany (light blue) is now “owed” €1.15 trillion, an amount that has escalated by 27% between January and September. At the same time, the greatest debtors, Italy, Spain and the ECB itself have increased their combined debts by €275bn to €1.3 trillion (before September’s additional deterioration for Spain and the ECB are reported — only figures up to August for them are currently available). But the most rapid deterioration for its size is in Greece’s negative balance, increasing by €45.6bn between January and August.

Is the Bundesbank worried by the increasing quantities of euros owed to it in a system that was always intended to roughly balance? Certainly. Will it publicly complain, or privately demand they be corrected? Almost certainly not. For statist systems such as the EU depend entirely on total obedience towards a common objective. All dissenters are punished, in this case by the waves of destruction that would be unleashed by any state refusing to continue to support the PIGS. TARGET2 is a devil’s pact which is in no one’s interest to break.

The imbalances are all guaranteed by the ECB. In theory, they shouldn’t exist. They partially reflect accumulating trade imbalances between member states without the balancing payment flows the other way. Additionally, imbalances arise when the ECB instructs a regional central bank to purchase bonds issued by its government and other local corporate entities. As the imbalances between national banks grew, the ECB has stopped paying for some of its bond purchases, leading to a TARGET2 deficit of €297bn at the ECB. The corresponding credits conceal the true scale of the deficits on the books of the PIGS national central banks. For example, to the extent of the ECB’s unpaid purchases of Italian debt, the Bank of Italy owes more to the other regional banks than the €546bn headline amount suggests.

Inside the workings of TARGET2

The way TARGET2 works, in theory anyway, is as follows. A German manufacturer sells goods to an Italian business. The Italian business pays by bank transfer drawn on its Italian bank via the Italian central bank through the Target2 system, crediting the German manufacturer’s German bank through Germany’s central bank.

The balance was restored by trade deficits, in Italy, for example, being offset by capital inflows as residents elsewhere in the eurozone bought Italian bonds, other investments in Italy and the tourist trade collected net cash revenues. As can be seen from the chart, before 2008 this was generally true. Part of the problem is down to the failure of private sector investment flows to recycle trade-related payments.

Then there is the question of “capital flight”, which is not capital flight as such. The problem is not that residents in Italy and Spain are opening bank accounts in Germany and transferring their deposits from domestic banks. It is that the national central banks which are heavily exposed to potentially bad loans in their domestic economy know that their losses, if materialised in a general banking crisis, will end up being shared throughout the central bank system, according to their capital keys if they are transferred into the TARGET2 settlement system.

If one national central bank runs a Target2 deficit with the other central banks, it is almost certainly because it has loaned money on a net basis to its commercial banks to cover payment transfers, instead of progressing them through the settlement system. Those loans appear as an asset on the national central bank’s balance sheet, which is offset by a liability to the ECB’s Eurosystem through Target2. But under the rules, if something goes wrong with the TARGET2 system, the costs are shared out by the ECB on the pre-set capital key formula.

It is therefore in the interest of a national central bank to run a greater deficit in relation to its capital key by supporting the insolvent banks in its jurisdiction. The capital key relates to the national central banks’ equity ownership in the ECB, which for Germany, for example, is 26.38% of the euro-area national banks’ capital keys. If TARGET2 collapsed, the Bundesbank, to the extent the bad debts in the Eurosystem are shared, would lose the trillion plus euros owed to it by the other national central banks, and instead have to pay up to €400bn of the net losses, based on current imbalances.

To understand how and why the problem arises, we must go back to the earlier European banking crisis following Lehman, which has informed national regulatory practices. If the national banking regulator deems loans to be non-performing, the losses would become a national problem. Alternatively, if the regulator deems them to be performing, they are eligible for the national central bank’s refinancing operations. A commercial bank can then use the questionable loans as collateral, borrowing from the national central bank, which spreads the loan risk with all the other national central banks in accordance with their capital keys. Insolvent loans are thereby removed from the PIGS’ national banking systems and dumped on the Eurosystem.

In Italy’s case, the very high level of non-performing loans peaked at 17.1% in September 2015 but by mid-2019 had been reduced to 6.9%. Given the incentives for the regulator to deflect the non-performing loan problem from the domestic economy into the Eurosystem, it would be a miracle if any of the reduction in NPLs is genuine. And with all the covid-19 lockdowns, Italian NPLs will be soaring again.

In the member states with negative TARGET2 balances such as Italy there have been trends to liquidity problems for legacy industries, rendering them insolvent. With the banking regulator incentivised to remove the problem from the domestic economy, loans to these insolvent companies have been continually rolled over and increased. The consequence is that new businesses have been starved of bank credit, because bank credit in the member nation’s banks is increasingly tied up supporting the government and businesses that should have gone to the wall long ago. The added pressure on failing Italian businesses from covid-19 is now being reflected in the Bank of Italy’s soaring TARGET2 deficit. The system could not be more calculated to cripple the Italian economy over the longer term.

Officially, there is no problem, because the ECB and all the national central bank TARGET2 positions net out to zero, and the mutual accounting between the national central banks keeps it that way. To its architects, a systemic failure of TARGET2 is inconceivable. But, because some national central banks end up using TARGET2 as a source of funding for their own balance sheets, which in turn fund their dodgy commercial banks using their non-performing loans as collateral, some national central banks have mounting potential liabilities, the making of national bank regulators.

The Eurosystem member with the greatest problem is Germany’s Bundesbank, now owed well over a trillion euros through TARGET2. The risk of losses is now accelerating rapidly as a consequence of the first round of Covid lockdowns, as can be seen in the chart of TARGET2 imbalances above. The second round of surging infections is leading to yet more economic destruction, yet to be reflected in TARGET2 balances, which will increase again. The Bundesbank should be very concerned.

Current imbalances in the system total over €1.5 trillion. According to the capital keys, in a systemic failure the Bundesbank’s assets of €1.115 trillion would be replaced by liabilities up to €400bn, the rest of the losses being spread around the other national banks. No one knows how it would work out because failure of the settlement system was never contemplated; but many if not all of the national central banks will have to be bailed out on a TARGET2 failure, presumably by the ECB as guarantor of the system. But with only €7.66bn of subscribed capital the ECB’s balance sheet is miniscule compared with the losses involved, and its shareholders will themselves be seeking a bailout to bailout the ECB. A TARGET2 failure would appear to require the ECB to effectively expand its QE programmes to recapitalise itself and the whole eurozone central banking system.

Now that really would be a crisis, the likes of which has never been seen before, where a central bank prints money purely to save itself and its regional agents.

The commercial banks are also in deep trouble

The deterioration in TARGET2 imbalances cannot be ignored by those with links to or outside of the Eurozone. While the UK is not in the euro or the TARGET2 settlement system, the Bank of England is a 14% shareholder in the ECB and could be on the hook for significant sums in the case of a Eurozone systemic crisis. Furthermore, with the City of London being the international financial centre for Europe, the UK banking system has considerable counterparty risks with Eurozone banks and other European banks.

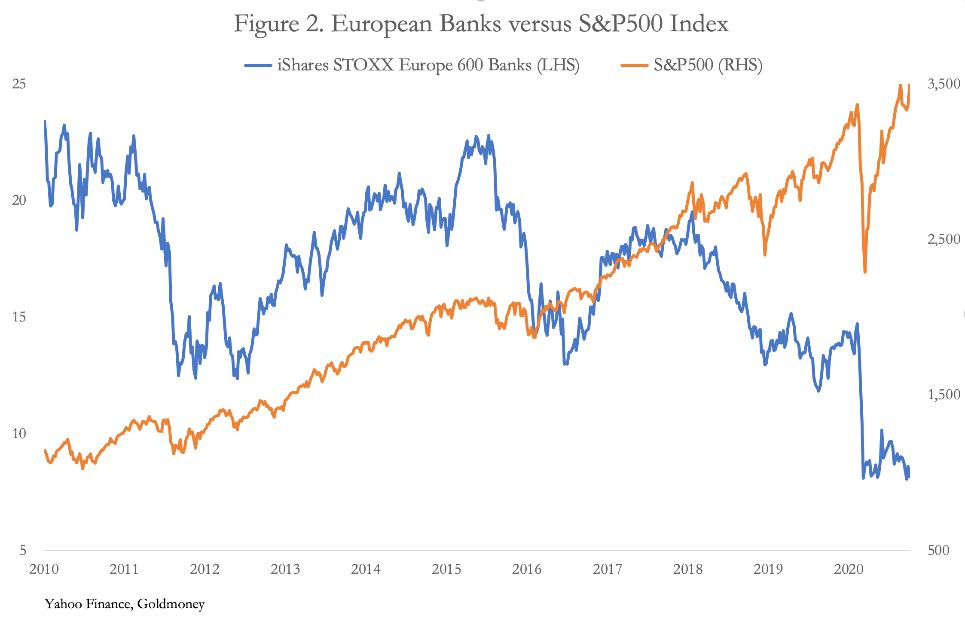

Over 50% of the iShares STOXX Europe 600 Banks ETF is invested in Eurozone banks: 28% is invested in UK banks, 13% in Swedish banks, and the balance in Danish and Swiss banks. Its weighting in favour of the Eurozone and UK makes it a reasonable proxy for the market rating of the major banks based in the European time zone. Figure 2 shows the performance of this ETF compared with the S&P500 Index, taken as a proxy for the world’s stockmarkets.

Since the aftermath of the Lehman crisis in 2008, the S&P500 index was in a continual bull market until February this year. At the same time, the share prices of European banks as represented in the ETF were in a bear market. Ahead of the Fed’s reflationary move on 23 March, from mid-February both the S&P500 and the European banks ETF crashed, but the S&P then soared to new hights. After the briefest of recoveries, the ETF sank to new lows.

Given the strong performance of equity markets following the March lows, the abysmal performance of the banks’ shares is ominous. In fact, the contradiction is so great the message from the stock markets appears to be that the Fed and other central banks will ensure, so far as they can, that stimulus will reach businesses sufficiently for them to recover from the covid-19 hiatus irrespective of the banks survival. It is a contradictory message suggesting businesses may survive and prosper but banks might not.

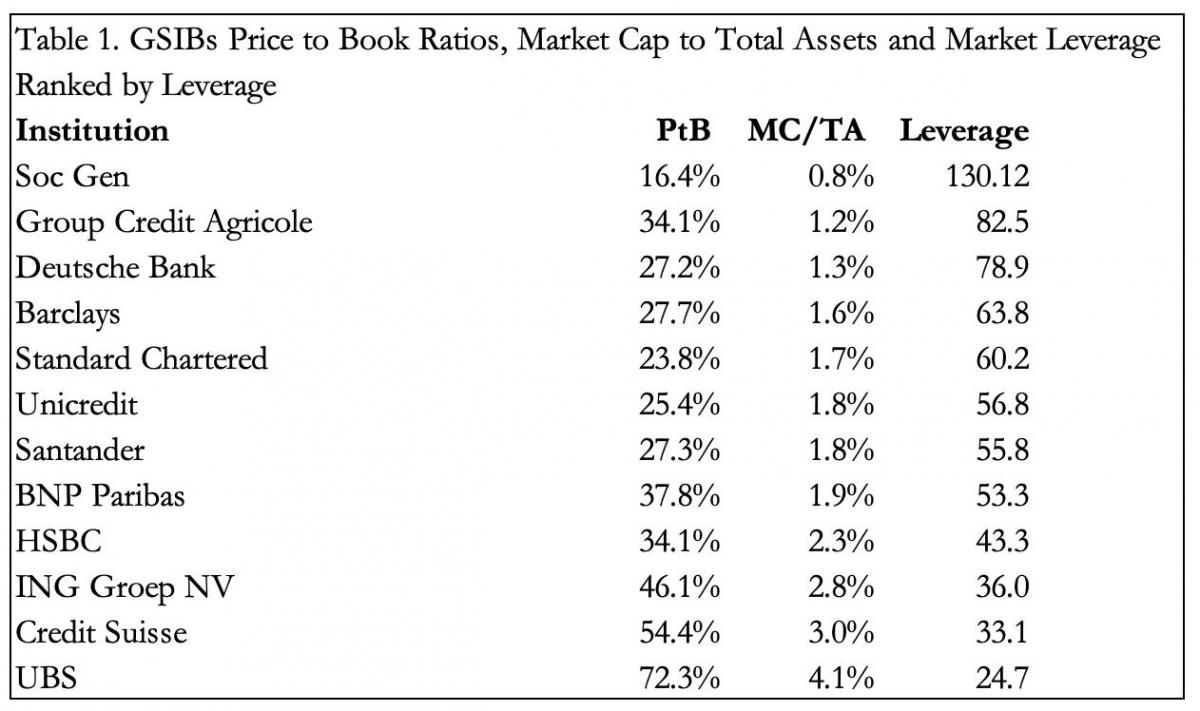

Besides the enormous implied faith among investors being placed in the ability of central banks to keep the wealth creating stock market bubble on the boil, either banks are being overlooked or are in serious trouble. The latter appears to be the case. Being more undercapitalised than the major commercial banks in any other region, many Eurozone banks present serious systemic risks and should not be trading. Figure 1 shows the market leverages of European globally-important banks — the G-SIBs, including those of EU, UK and Switzerland.

Only two of them, the Swiss banks, have price to book ratios in excess of 50%. As well as these G-SIBs there are many other commercial banks in Europe with similarly horrifying price to book ratios and balance sheet to market capital leverage ratios. Blind to the implications of market capitalisations, regulators look no further than the relationship between total assets and balance sheet equity. But when markets place a price to book valuation of considerably less than 100% on any enterprise, they tell us the enterprise is not just insolvent, but in a winding-up, shareholders are unlikely to recover their funds. So, when we observe that Société Generale, the major French bank, has a price to book ratio of only 16.4%, without a major capital injection it is almost certainly bankrupt because its share price is little more than option money on its future survival.

The price to book values of all these G-SIBs have improved marginally in recent weeks, carried along by a dead-cat bounce. Even then, bank stocks remain close to their long-term lows when stock indices such as the S&P500 index have been forging new highs. This contradiction also suggests that investors have not been making rational decisions, and that with the exception of banks, stock markets are being driven by a combination of monetary expansion and the madness of crowds.

European businesses are now being bankrupted by a second covid-19 wave. The bankruptcies from the first have not yet fully worked into the financial system and will now be compounded by a second wave. Nothing can stop non-performing loans increasing and undermining overstretched commercial banks. The game of passing the parcel up into TARGET2 imbalances will continue until it crashes. Since few understand TARGET2 and those that do are frightened into silence, presumably it will be market assessments of individual banks and their collapse into bankruptcy that will be the trigger for a widespread systemic crisis in the Eurozone. The whole Eurozone monetary system is deep into borrowed time.

The euro’s valuation

For the moment, the euro is riding high against the dollar, encouraging the ECB to explore deeper negative interest rates. But it is worth reminding ourselves of the currency dynamics behind the euro-dollar cross rate.

Until September 2019, large hedge funds were playing the fx swaps market. In effect, through their banks they were borrowing euros, selling them for dollars, and gaining the interest differential. This was one of the reasons for last September’s repo crisis in New York, when the leading banks ran out of balance sheet to finance both fx swaps and other derivative and credit activities. The repo crisis ended with the Fed cutting its funds rate from 2%, first to 1.5% then 1%, which took much of the steam out of the euro-dollar fx cross. With those positions now closed down the euro is more influenced by trade flows. And here, the EU runs a trade surplus of about €150bn with the US, which given that the US budget deficit has increased substantially, seems set to increase further unless Americans suddenly adopt a savings habit.

The capital position is favourable to the euro as well, when in June 2019, the last recorded total of US financial securities held by EU residents, totalled $9.631 trillion. And US residents’ ownership of Euro area securities totalled $2.952 trillion at end-2019 — a gap of $6.679 trillion. Therefore, in a banking crisis when foreign investments get sold down, there is likely to be substantial net buying of the euro against the dollar.

The euro has the potential to rise further against the dollar before and possibly during a systemic banking crisis. After such a crisis, all bets will be off. All we know is that the rottenness of the euro area monetary system will almost certainly lead to its destruction and most likely the end of the euro itself. The immediacy of the problem allows us to dismiss talk of resets and central bank digital currencies, which are being pushed by the monetary looters at the ECB who might sense there is a crisis to avoid. The talk of monetary stimulation with yet deeper negative interest rates is part of it, the hope being a new central bank digital currency will bypass a broken banking system.

But now the commercial banks are bust, we are about to see a monetary implosion that can only result in the euro’s destruction.

A Phoenix will arise from the ashes — eventually

It was not the people, but the governments they were fooled into electing, and which in turn were fooled into the European project, which will bear responsibility for the collapse of the European Union. The large corporations which were corrupted into supporting socialistic ideals instead of serving their customers for profit, played their part in the looting. All this will be destroyed. There will be acute hardship as the rotten system collapses, but so be it.

Hopefully, the civil conflicts and the evolution to a sounder form of money and monetary system will be time-limited — but that depends on how long events take to evict the looters in government. The best that the residents of Euroland can hope for at this juncture is that the collapse of the money will hasten their demise.

The fate of the euro will be shared with the majority — if not all — of other fiat currencies for reasons specific to them. The recovery from the ashes of government incompetence can be swift — a matter of a year or two, so long as successor governments quickly learn that free markets, sound money and minimal interference from government are all required for the restoration of economic progress. Additionally, all socialist policies must be discarded, and the profit motive and individual wealth creation embraced.

It will require the wholesale destruction of state bureaucracies — that will happen when the euro collapses. And they must not be replaced by new bureaucracies beyond a bare minimum required for administering law and order. Politicians must learn that bureaucratic power is a false and dishonest objective, and that a nation can only become great by the efforts of its people pursuing profits by providing what consumers want. As a creed, Caveat emptor for consumers must be reinstated.

Consumers are the kings to be worshipped by producers seeking profits. And consumers have a responsibility to themselves, judging what is best for them and not relying on regulating government agencies to decide on their behalf. In business, there is no room for the luxuries of dissent. Employing people on the basis of their sex, race, disabilities and other mores must cease. The basis of any employment must be purely on ability, skills and suitability. All regulations over production must be abandoned. The businesses that supped with the devil in Brussels must never regain the advantages through their political influence. If they don’t collapse with the euro, these corporations will have to learn to survive competition from new challengers on their own.

The concept of a European superstate must be discarded, and any attempt to reinvent it firmly stopped. European nations must stand by the successes and failures of their national abilities to create wealth, allowing their peoples to do it and retain it for themselves. Tax competition between jurisdictions will help guarantee that the growth of government is contained.

Underwriting a new Europe must be small government, free markets and sound money. As Germany discovered following both world wars, sound money is the precondition for economic progress. Fortunately, there are still a few sound money men in the central banks of Germany, The Netherlands, and believe it or not France and Italy — evidenced by their gold holdings and in the case of the former two their repatriation from foreign vaults. They must establish their own gold substitutes and be directly exposed to the consequences of monetary manipulation, should future governments be tempted to corrupt the money again.

The concept of farming out monetary affairs to a superstate organisation will have been disproved by the collapse of the euro and must not be attempted again. In a successful future, the people of Europe will decide personal their needs and wants, individually.

Alasdair Macleod

HEAD OF RESEARCH• GOLDMONEY

Twitter: @MacleodFinance

MOBILE: +44 7790 419403

Goldmoney

The Most Trusted Name in Precious Metals tm

NEW YORK | ST. HELIER | TORONTO

Publicly Traded Symbols: CA: XAU | US: XAUMF

© 2020 GOLDMONEY INC. ALL RIGHTS RESERVED. THIS MESSAGE MAY CONTAIN CONFIDENTIAL OR PRIVILEGED INFORMATION. IF YOU ARE NOT THE INTENDED RECIPIENT, PLEASE ADVISE US IMMEDIATELY. THIS MESSAGE IS FOR GENERAL INFORMATION ONLY AND SHOULD NOT BE CONSTRUED AS AN OFFER OR SOLICITATION OF AN OFFER TO BUY SECURITIES OR ANY OTHER FINANCIAL INSTRUMENTS. WE DO NOT PROVIDE TAX, ACCOUNTING, OR LEGAL ADVICE, AND RECOMMEND THAT YOU SEEK INDEPENDENT PROFESSIONAL ADVICE IF NECESSARY. WE CONSIDER INFORMATION IN THIS MESSAGE RELIABLE BUT WE DO NOT REPRESENT THAT IT IS ACCURATE, COMPLETE, AND/OR UP TO DATE AND IT SHOULD NOT BE RELIED ON AS SUCH. OPINIONS EXPRESSED ARE OUR CURRENT OPINIONS AS OF THE DATE APPEARING ON THIS MESSAGE ONLY AND ONLY REPRESENT THE VIEWS OF THE AUTHOR AND NOT THOSE OF GOLDMONEY INC OR ITS SUBSIDIARIES UNLESS OTHERWISE EXPRESSLY NOTED.

Notice: This email may contain confidential or privileged information. If you received this email in error or believe you are not the intended recipient, please notify the sender immediately and delete this email without forwarding or opening any attachments. Thank you for your cooperation and attention.

********of US Portfolio Holdings of Foreign Securities by Country and Type of Security, as of December 31, 2020

More from Silver Phoenix 500