Does Your Muni Bond Fund Own Puerto Rico’s Bad Debt?

While the media and investors are focused on Greece, Puerto Rico is having a debt meltdown of its own. The U.S. territory owes lenders over $70 billion, $5.4 billion of which is due in the next 12 months. But without some form of debt restructuring, says Governor Alejandro García Padilla, it will be unable to meet its obligations. Countless municipal bond fund investors—many of them unaware they have exposure to the Caribbean island—could be affected.

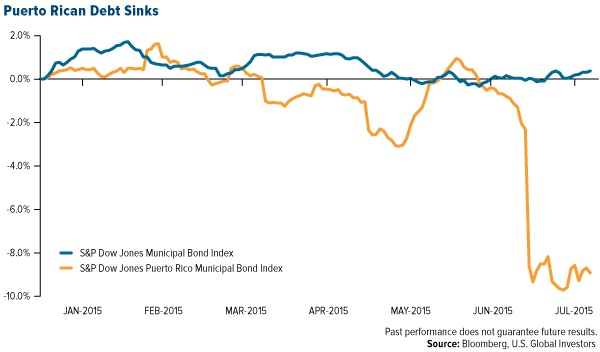

Year-to-date, Puerto Rican munis have lost 9 percent while U.S. munis have gained 0.4 percent.

Our Near-Term Tax Free Fund (NEARX) has no exposure to Puerto Rico. NEARX invests predominantly in high-quality munis, and our investment team prudently adjusted fund allocations when it became clear the commonwealth would face serious problems paying back bondholders.

The same can’t be said for many other funds in the U.S., however. Over 20 percent of American bond funds owns Puerto Rico’s bad debt, according to Morningstar. Sixteen of the 20 mutual funds with the highest ownership by percentage are run by a single investment management firm. The same firm owns nearly half of all Puerto Rican debt that’s owed by U.S. funds. Another firm offers a fund that has half of its investments in Puerto Rican bonds.

You might be wondering why these funds have invested so heavily in the island. Because they carry a “junk” rating, Puerto Rican bonds offer a higher yield than more conservative bonds. They also provide what’s called “triple tax exemption,” meaning they’re tax-free at the federal, state and local levels.

The tradeoff, of course, is that investors assume a greater deal of credit risk. That’s why it’s crucial for investors to be familiar with their funds’ holdings.

To Bail Out or Not to Bail Out?

On Monday, Governor Padilla asked Congress to grant Puerto Rico the ability to declare bankruptcy. The problem, though, is that like all U.S. states, the territory can’t file for Chapter 9 bankruptcy protection. That’s an option available only to municipalities and cities such as Detroit, whose own bankruptcy exactly two years ago was the largest in U.S. history by debt, estimated at between $18 and $20 billion.

Whether to bail out the commonwealth is currently being debated. Some officials believe Puerto Rico is “too big to fail.” Others argue that its leaders haven’t done enough to reverse years of economic slowdown. Forty-six percent of all native-born Puerto Ricans who moved to the U.S. mainland between 2006 and 2013 did so for job-related reasons, according to the Pew Research Center.

“Puerto Rico is a beautiful island with a rich culture, but currently its government isn’t doing enough to encourage young professionals to stay,” says Kat, USGI’s web designer, who moved from Puerto Rico to San Antonio in 2007. “The cost of living keeps going higher while wages haven’t improved. I don’t know what needs to be done, but raising the sales tax and doing nothing to prevent talent from leaving the island aren’t the answer.”

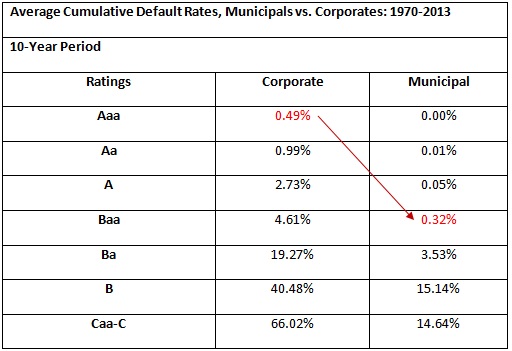

Highly-Rated Municipal Bonds Remained a Relatively Safe Asset Class

Just as investors should know what assets they own, it’s important for them to realize that Chapter 9 filings—at least among highly-rated municipalities—have been the exception, not the norm. According to ratings agency Moody’s, Baa-rated munis historically had similar default rates as Aaa-rated corporate bonds.

Source: Moody’s, U.S. Global Investors

Again, NEARX invests in quality, short-term munis. Having provided investors with over 20 straight years of positive returns, the fund holds five stars overall from Morningstar, among 184 Municipal National Short-Term funds as of 6/30/2015, based on risk-adjusted return.

Let’s hope our friends to the south can reach a solution to the debt crisis.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Total Annualized Returns as of 6/30/2015:

|

Fund |

One-Year |

Five-Year |

Ten-Year |

Gross Expense Ratio |

Expense Cap |

|

Near-Term Tax Free Fund |

0.90% |

2.27% |

2.98% |

1.08% |

0.45% |

********

Expense ratio as stated in the most recent prospectus. The expense cap is a contractual limit through April 30, 2016, for the Near-Term Tax Free Fund, on total fund operating expenses (exclusive of acquired fund fees and expenses, extraordinary expenses, taxes, brokerage commissions and interest).Performance data quoted above is historical. Past performance is no guarantee of future results. Results reflect the reinvestment of dividends and other earnings. For a portion of periods, the fund had expense limitations, without which returns would have been lower. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance does not include the effect of any direct fees described in the fund’s prospectus which, if applicable, would lower your total returns. Performance quoted for periods of one year or less is cumulative and not annualized. Obtain performance data current to the most recent month-end at www.usfunds.com or 1-800-US-FUNDS.

Bond funds are subject to interest-rate risk; their value declines as interest rates rise. Though the Near-Term Tax Free Fund seeks minimal fluctuations in share price, it is subject to the risk that the credit quality of a portfolio holding could decline, as well as risk related to changes in the economic conditions of a state, region or issuer. These risks could cause the fund’s share price to decline. Tax-exempt income is federal income tax free. A portion of this income may be subject to state and local taxes and at times the alternative minimum tax. The Near-Term Tax Free Fund may invest up to 20% of its assets in securities that pay taxable interest. Income or fund distributions attributable to capital gains are usually subject to both state and federal income taxes.

The S&P Municipal Bond Index is a broad, market value-weighted index that seeks to measure the performance of the U.S. municipal bond market. The S&P Municipal Bond Puerto Rico Index is a broad, market value-weighted index that seeks to measure the performance of bonds issued within Puerto Rico.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

More from Silver Phoenix 500