Don’t Let Market Motion Sickness Keep You From Missing The Boat

By most accounts, major U.S. markets have performed positively this year, generating significant wealth for many investors. The S&P 500 Index has made fresh highs pretty regularly and is currently up 12 percent, and so far the Nasdaq Composite Index has returned 14 percent.

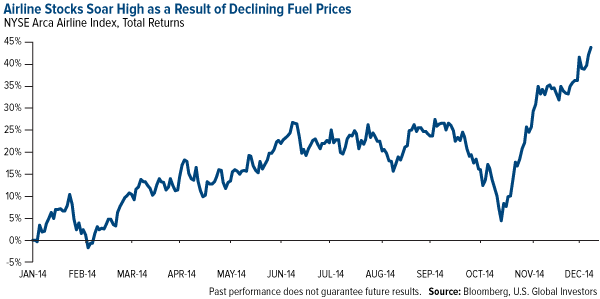

The upside to falling oil prices is consumers are heading in to the holiday shopping season with extra money in their pockets. At a handful of stations in Oklahoma and Texas, gas prices fell below $2 last week. Consumer airlines are also benefitting from the “tax break” of low fuel prices. Year-to-date, the NYSE Arca Airline Index has delivered a stellar 43 percent. The benefit is not limited to the U.S., as China Airlines is up 31.5 percent.

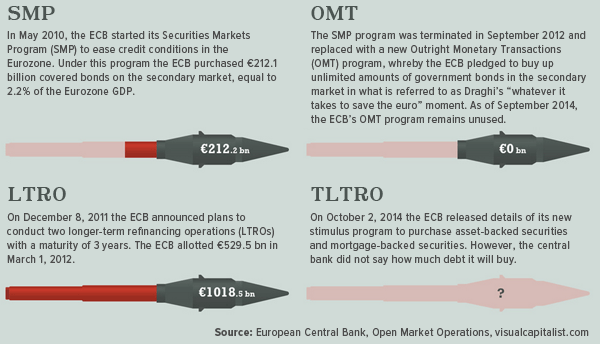

The most welcome news coming out of Europe is that although its central bank did not take concrete action this week, European Central Bank (ECB) president Mario Draghi offered assurances that more aggressive stimulus to help jumpstart the eurozone’s flagging economy is just around the corner. The plan is called—deep breath—Targeted Long-Term Repo Operation (TLTRO) and will allow the ECB to purchase covered bonds and asset-backed securities over the next two years. Such a plan will hopefully stimulate bank lending to non-financial corporations.

Below are some of the other programs in the ECB’s arsenal, courtesy of Visual Capitalist:

While Europe is seeking stimulus, Russia is staring down a recession next quarter because of international sanctions, declining oil prices and a weakening ruble. The combined costs of these setbacks are expected to reach a stunning $140 billion a year. Our Emerging Europe Fund (EUROX) has benefited from our decision to pull out of Russia last year.

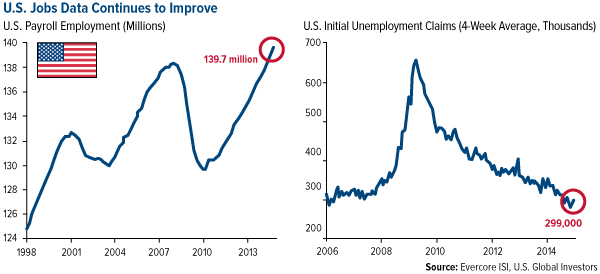

And we must not forget the positive U.S. jobs data, released on Friday. Last month payrolls grew an astounding 321,000, exceeding market-watchers’ expectations, while the jobless rate holds at 5.8 percent. As many commentators have pointed out, this year has shaped up to be the strongest for job creation since President Clinton resided in the White House.

But Many Investors Stymied by Uncertainty

Despite all of the good news, the recent threat of market volatility, which we’ve seen plenty of in commodities and emerging markets, seems to have pushed close-to-retirement folks away from equity securities. The August and October downturns, not to mention the decline in gold and oil prices, have understandably heightened consumer fears.

Fair enough. I’ve spoken with a lot of people who have shown the symptoms of seasickness from the dips and swings in the market.

A new study, in fact, highlights the growing number of green-faced investors who may be missing out on the long-term wealth creating opportunities of the market.

Allianz Life recently polled close to 800 Americans, none of them retired yet, and found that a vast majority—78 percent—said they “preferred financial products with guarantees over products with higher growth potential but the possibility of losing value.”

Also interesting, when Allianz asked them what they would do if they had extra money to invest, too many people chose inaction.

Surprisingly, over 30 percent said they would either put the cash in a savings account earning next-to-zero interest or keep waiting for the market to correct before investing. Caution is one thing, paralysis is another altogether. As President George H. W. Bush once said: “If Columbus had waited until all the problems of his time were solved, the timbers of the Santa Maria would be rotting on the Spanish coast to this day.”

Another block of respondents, nearly 40 percent, said they preferred some balance. That is to say, they would invest in a product that provided a little growth and a little protection.

In other words, they’re perfectly willing to embark on what could be a rewarding voyage, so long as they have some Dramamine on hand—you know, the stuff that treats motion sickness.

As you shall see, a portfolio that strategically balanced both stocks and municipal bonds for the long term historically gave back healthy returns while protecting against some loss.

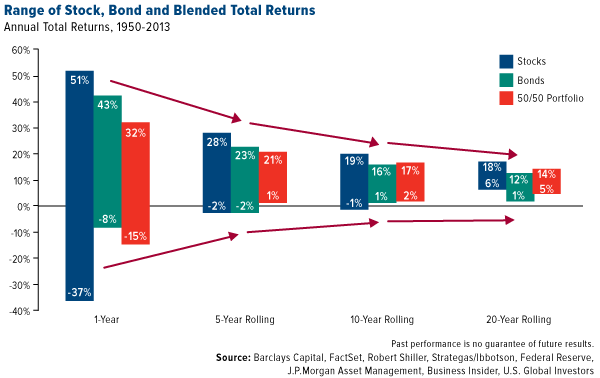

Balancing Act

Take a look at the chart below. What it shows are the risks and rewards of holding various instruments for one, five, 10 and 20 years.

Based on annual returns from 1950 to 2013, the rewards were huge when securities were held for one year—but so were the risks. While stocks could have netted up to 51 percent, they could also have taken back as much as 37 percent. Bonds returned a little less, up to 43 percent, but the average loss was only 8 percent—a 29-point spread from stocks. A 50/50 portfolio, held for only a year, trailed both, returning up to 32 percent.

But a funny thing happened if you extended the holdings out. The blended portfolio began to play catchup not only on the upside but also the downside. Held for 10 years, such a portfolio outperformed bonds and was only two percentage points shy of matching stocks. It was also less risky.

Twenty years out, a 50/50 portfolio handily beat bonds and had an approximate amount of risk as stocks.

Investors who blended their portfolios might have made out with a little less than those who held only equity securities, but they also underwent a lot less stress and fewer sleepless nights—especially if they invested during the first decade of the century, when there were not one but three major financial crises.

14 Years of Positive Returns

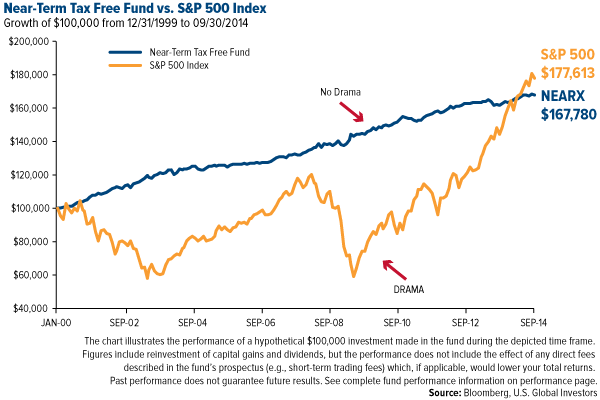

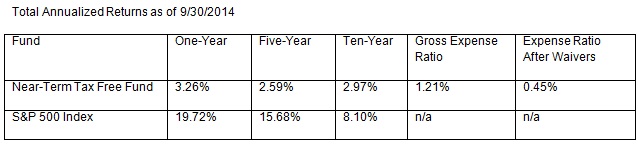

For those investors who know that life offers few guarantees and appreciate balance in their life and investments, we have a product that has worked similarly to offset, but not entirely eliminate, the volatility you might experience in the major markets: the Near-Term Tax Free Fund (NEARX).

Many of you have no doubt seen the following chart, but it’s worth sharing again. Whereas the S&P 500 showed extreme volatility last decade because of the dotcom bubble, 9/11 and the financial crisis, NEARX climbed modestly upward, oblivious to the ups and downs that created so much heartache and anxiety for stockholders.

I shared a story about a couple of weeks back that dramatizes this very point, and already I’ve received quite a lot of positive feedback. You can read it here if you haven’t already done so. It’s not to be missed!

What’s most striking about this chart is that, following a hypothetical investment of $100,000 in 2000, it took the S&P 500 nearly 14 years to catch up with NEARX.

Naturally, past performance doesn’t guarantee future results, and you shouldn’t reasonably expect the fund to keep pace with an index of equity securities like the S&P 500 over the next 10, 15 and 20 years. However, NEARX has historically shown a greater likelihood of dodging the dramatic swings the equity market has often experienced in times of uncommonly high volatility, such as we saw in the first decade of the century.

I’ve just returned from London where I spoke at the Mines and Money Conference and I’ll share insights from that event soon. In the meantime, you can catch my interview with Bloomberg TV while I was there.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Expense ratio as stated in the most recent prospectus. The expense ratio after waivers is a contractual limit through December 31, 2014, for the Near-Term Tax Free Fund, on total fund operating expenses (exclusive of acquired fund fees and expenses, extraordinary expenses, taxes, brokerage commissions and interest). After December 31, 2014, this arrangement will become a voluntary limitation that may be changed or terminated by U.S. Global Investors at any time, which may lower the fund’s yield or return. Performance data quoted above is historical. Past performance is no guarantee of future results. Results reflect the reinvestment of dividends and other earnings. For a portion of periods, the fund had expense limitations, without which returns would have been lower. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance does not include the effect of any direct fees described in the fund’s prospectus which, if applicable, would lower your total returns. Performance quoted for periods of one year or less is cumulative and not annualized. Obtain performance data current to the most recent month-end at www.usfunds.com or 1-800-US-FUNDS.

Past performance does not guarantee future results.

Bond funds are subject to interest-rate risk; their value declines as interest rates rise. Though the Near-Term Tax Free Fund seeks minimal fluctuations in share price, it is subject to the risk that the credit quality of a portfolio holding could decline, as well as risk related to changes in the economic conditions of a state, region or issuer. These risks could cause the fund’s share price to decline. Tax-exempt income is federal income tax free. A portion of this income may be subject to state and local taxes and at times the alternative minimum tax. The Near-Term Tax Free Fund may invest up to 20% of its assets in securities that pay taxable interest. Income or fund distributions attributable to capital gains are usually subject to both state and federal income taxes.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio. The Emerging Europe Fund invests more than 25% of its investments in companies principally engaged in the oil & gas or banking industries. The risk of concentrating investments in this group of industries will make the fund more susceptible to risk in these industries than funds which do not concentrate their investments in an industry and may make the fund’s performance more volatile.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The NYSE Arca Airline Index is designed to measure the performance of highly capitalized and liquid U.S. and international passenger airline companies identified as being in the airline industry and listed on developed and emerging global market exchanges. The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000. The Russell 3000 Index consists of the 3,000 largest U.S. companies as determined by total market capitalization.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the funds mentioned as a percentage of net assets as of 9/30/2014: Allianz Life Insurance Company of North America 0.00%, China Airlines 0.00%.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.