The Fed Meets The S&P500 Bull

Yesterday's Fed statement drove stock lower, but did the overnight slide tick all the boxes so far – that's the question to ask. And why exactly did the market get so disappointed with the FOMC moves? I'll answer these questions in today's analysis, and lay out the prospects for the stocks ahead.

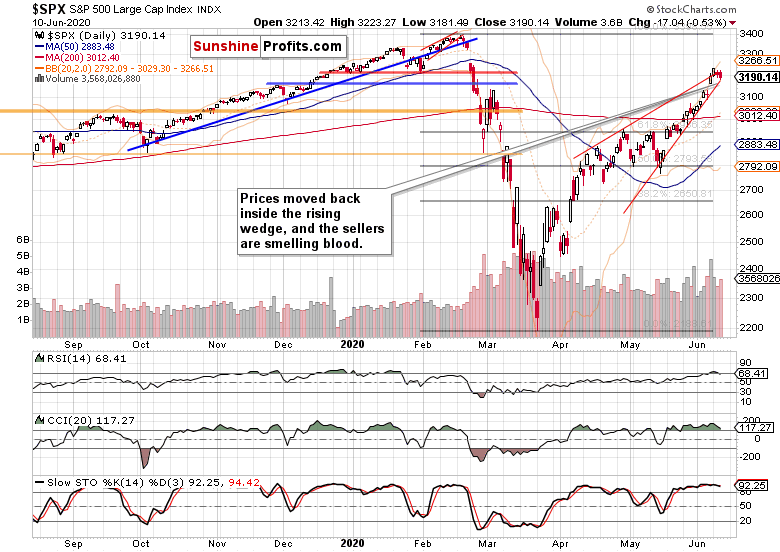

S&P 500 in the Short-Run

Let’s start with the daily chart perspective (charts courtesy of http://stockcharts.com ):

Well before going into the Fed policy statement, signs were there that the bulls aren't at their strongest, and I took profits from the open long position off the table. Since then, the S&P500 went largely sideways until the Fed moment came. The following spike higher attracted the bears' interest, and stocks gave up all of their momentary gains. What exactly did the Fed say that it drove stocks that much lower in the overnight trading?

I expected them to not rock the boat – so, did they do it actually? Offering a sober assessment of the economy, they aren't looking to raise rates any time soon, and will keep the wheels greased. No surprise here.

But there are two things hanging in the air, one of which depends on the Fed, while the other doesn't.

I've written quite a few times lately about the rising Treasury yields. Rising yields translate into falling Treasury prices, and it raises the prospects of yield curve control arriving. Yield caps could indeed be coming. Quite logical if you consider that the Treasury needs to finance ever larger deficits.

When the economy expands or is expected to regain footing as is the case currently, and money flows from bonds into stocks, the S&P 500 is rising while the bond market (Treasuries) sees rising yields that translate into declining bond prices. That's what we have seen in the runup to yesterday's Fed.

Rising yields are a sign of belief in the recovery story, but when Powell reiterates fears of stubborn corona consequences and that he stands ready to expand the balance sheet to infinity should they rise too much, that certainly dampens the bullish spirits in stocks. And yesterday's action in both shorter- and longer-dated Treasuries (IEI ETF, TLT ETF respectively) have shown that the market isn't willing to bet against the Fed right now.

Against this background, paring some of the recent gains in stocks is understandable, especially when we consider the second factor that is outside of the Fed's control.

As the riots proceed, coronavirus made a comeback into the headlines. The fears of the second wave in the U.S. are here. This is likewise working to keep the risk appetite at bay.

Are the stock bulls panicking, with prices getting ahead of themselves in their downside move?

Before answering, one more thought about low yields and stocks. Once a recessionary shock is over (not getting worse) and inflationary pressures of the moment are still low (forget about the forward-looking inflationary expectation – they're not manifest in the real economy just yet), stock prices and bond prices tend to move hand in hand. The real economy is far from its potential output, and isn't overheating just yet.

Tick, that's what we're facing right now. That's why low yields are a good companion of a stock bull market. Remember, bonds top first, stocks next, and finally commodities. As we haven't seen a top in Treasuries just yet, the stock bull market peak is even farther off.

As promised, let's check now whether the stock bulls are panicking or not.

The Credit Markets’ Point of View

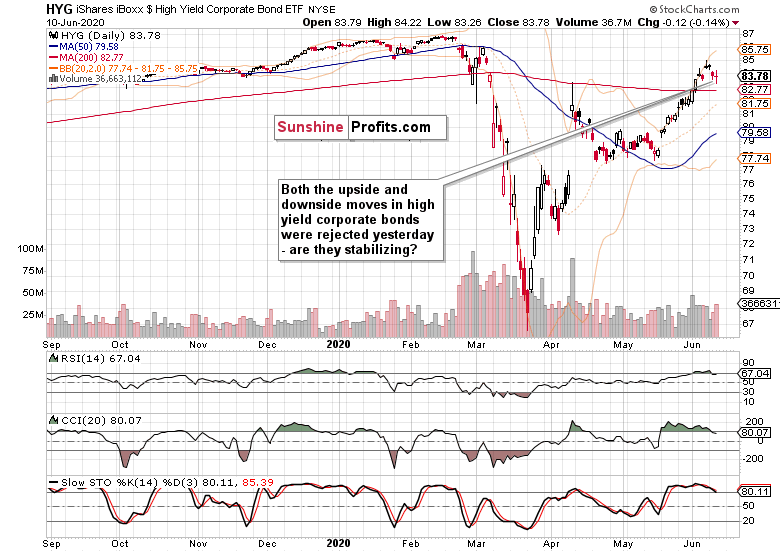

High yield corporate bonds (HYG ETF) refused to move any lower yesterday, but by the same token, they didn't rise either. The daily indicators are almost in unison on sell signals, so caution is warranted before calling the bonds stabilized. Needless to say, I continue to think we have still a bit more to go before seeing corporate bond prices above Friday's highs.

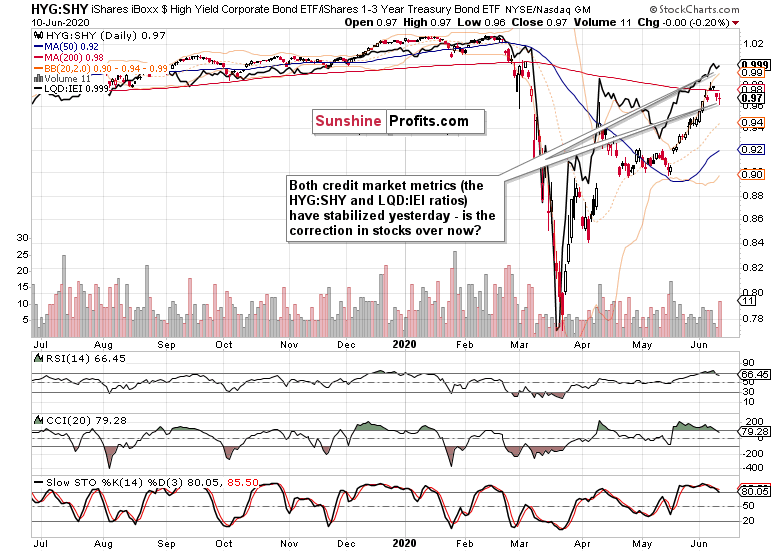

This is the shape of both the above-mentioned leading credit market ratios.

The more risk-on one (HYG:SHY) is still leading the downswing, and unless it edges higher, it's a red flag. As I wrote yesterday:

(…) The animal spirits are thus likely to get tested relatively soon, with perhaps today's Fed monetary policy] statement and conference being the catalyst. Or Friday's inflation expectation figures could play that role.

Either way, unless credit markets recover, stocks are in the short-term danger zone.

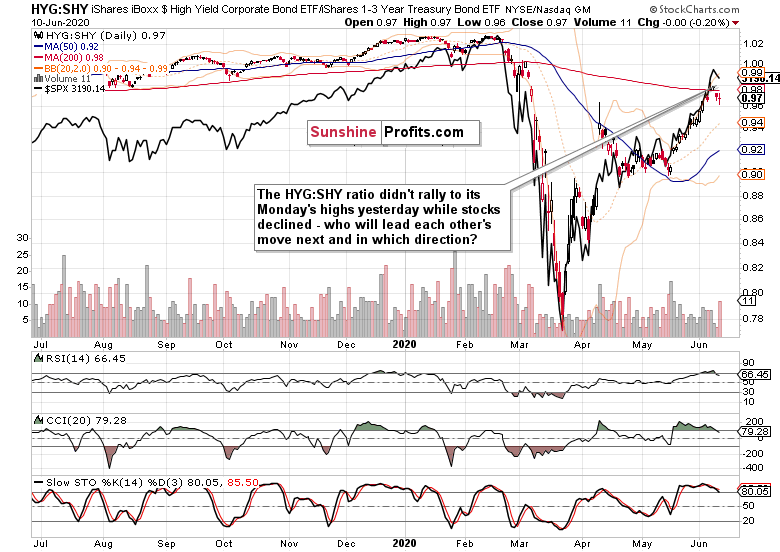

Next, I showed you the following chart with overlaid S&P 500 prices.

And other yesterday’s thoughts are valid also today, showing that stocks are still vulnerable in the short run.

(…) Stocks are kind of hanging out there in the short run, and the degree of relative extension makes me think that the stock upswing isn't likely to proceed with its previous momentum before taking a pause first.

What about the S& 500 sectoral moves?

Key S&P500 Sectors in Focus

Technology (XLK ETF) closed at new 2020 highs but gave up half of its intraday gains, while healthcare (XLV ETF) finished not too far from its Tuesday's closing values. Financials (XLF ETF) certainly led the downswing in the S&P 500 heavyweights.

Energy (XLE ETF), materials (XLB ETF) and industrials (XLI ETF) moved sharply lower yesterday, which is not a good short-term omen for the bull-run.

As pointed out in yesterday’s analysis:

(…) unless the credit markets get their act together, the short-term risks for stocks are getting skewed to the downside. That could be amplified by the USDX taking a breather after the recent sea of red.

The USD Index breather is underway as the greenback is finally making a move from its short-term lows. How vigorous that turns out to be, would put to test the stock market bull-run. Remember, since the WWII ended, we've seen only one market rally above the 61.8% Fibonacci retracement that was followed by a plunge below the prior bear market low.

And I fully expect that the March 23 lows won't be challenged, let alone broken.

Summary

Summing up, the Fed provided the catalyst for stocks to move down, and neither the credit markets nor the sectoral analysis show signs that this correction is already over. Smallcaps at Russell 2000 (IWM ETF) are leading the downside move, which coupled with the earlier USDX move, raises short-term risks for stocks. Even accounting for today's premarket action, I still say short-term – the narrative of reopening optimism is only now being challenged by yet another down-to-earth Fed real economy assessment and returning coronavirus fears. The credit markets will show us how far the bulls are really willing to retreat.

I encourage you to sign up for our daily newsletter - it's free and if you don't like it, you can unsubscribe with just 2 clicks. If you sign up today, you'll also get 7 days of free access to the premium daily Stock Trading Alerts as well as our other Alerts. Sign up for the free newsletter today!

Monica Kingsley

Stock Trading Strategist

Sunshine Profits: Analysis. Care. Profits.

* * * * *

All essays, research and information found above represent analyses and opinions of Monica Kingsley and Sunshine Profits' associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Monica Kingsley and her associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Ms. Kingsley is not a Registered Securities Advisor. By reading Monica Kingsley’s reports you fully agree that she will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Monica Kingsley, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

********

Monica Kingsley is a trader and financial markets analyst. Checking dozens of charts daily, she integrates their messages with economics and in-depth experience. Trade calls and writing are her cup of tea as much as studies in market histories. Having been at the financial markets when the Great Recession arrived, she experienced many bull and bear markets - be it in stocks, bonds, gold and silver. https://www.monicakingsley.co