Federal Reserve Folly

-

Unneeded Fire Trucks

-

Slamming the Brakes

-

Force-Feeding Liquidity

-

The Right Course

-

Washington, DC, Maine, Colorado, and Personal Losses

Great news: The US economy is officially out of recession. We know this because the National Bureau of Economic Research’s official recession-calling committee said so this week. The economy has been in an expansion phase since last April, making this the shortest recession on record at only two months.

The NBER committee always makes these calls in hindsight—both the beginning and end of recessions. Literally everyone could see the economy coming to a halt in March and April. The signs weren’t subtle. Yet it wasn’t until June 8, 2020, that they said the economy had peaked in February, marking the recession’s onset. I don’t blame them for waiting to see the data, though. Caution is appropriate on these things.

But really, 15 months to affirm the economy has been expanding? Their statement was quite specific. They call April 2020 the bottom because that month showed clear troughs in unemployment, GDP, PCE, and personal income ex-transfers. All this was known long ago.

Unlike NBER, a private group with no formal power, the Federal Reserve can actually do something with this kind of information. Nor does the Federal Open Market Committee have to wait for confirmation. It can act whenever it sees a need, which it certainly did when the pandemic struck.

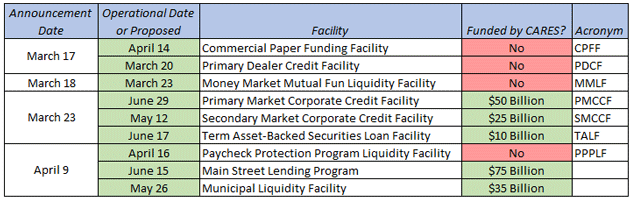

Here’s a handy timeline summarizing the Fed’s near-daily actions in March and April 2020. They did far more than just open the Quantitative Easing spigots ($120 billion a month and counting) and lower the Fed Funds rates to zero.

Source: AAF

As I said back then, the Fed’s dramatic response (accompanied by the federal government’s equally dramatic fiscal response) was appropriate given what was known at the time. It was an unprecedented situation, potentially threatening the economy and financial system’s core stability. They had to act quickly and aggressively.

Where we can/should blame Fed leadership, though, is in the failure to recognize the time to slowly end the extraordinary measures, which are now having extraordinary and harmful side effects. Today I want to describe what is happening and tell you what I think the Fed should do. Though, to be frank, I have little hope they will.

Let me be very clear. I believe the Federal Reserve has already made a significant policy error that can lead directly to recession. An accompanying fiscal policy error by the US Congress could compound the Fed’s error, although that remains to be seen, as it is not clear what will pass Congress.

Unneeded Fire Trucks

I greatly admire the skill and bravery of firefighters. I once had the personal benefit of their help (recounted here) and was glad they came.

In watching how firefighters work, I have noticed some patterns. When notified of an emergency like a high-rise fire, which could be either very serious or a mild annoyance, they assume the worst. They arrive quickly and in force. Once on-scene, they decide exactly what is needed and the chief then either calls for reinforcements or releases the extra capacity to go elsewhere. But they initially bring it all “just in case.” This is prudent when lives may be at stake.

What they don’t do is stay on the scene in full force once the emergency is over. Of course, large fires can smolder for days. They might leave a small crew to extinguish any flare-ups but they won’t tie up the entire department when it may be needed elsewhere.

Now imagine the Federal Reserve is our financial fire department. It got a 12-alarm call in March 2020 and rolled out every truck it had. That was the right response. But within a few months, or at most a few quarters later, it was clear the Fed’s part of the emergency was over.

COVID-19 wasn’t over, of course (and still isn’t), nor was the economy in a great position. But the systemic meltdown risk had passed. The fire was still smoldering but at that point, it was mainly a fiscal fire. Fire Chief Jerome Powell himself said so, repeatedly begging Congress to deal with unemployment and business failures more effectively. He admitted there was little else his fire trucks could do but he kept them there anyway in the form of massive quantitative easing and keeping rates at the zero bound. They are still on-scene now.

It is my opinion that this has the potential to go down as the greatest policy error in central bank history. I know that’s saying a lot. Arthur Burns and G. William Miller letting inflation rise in the 1960s and 1970s ranks up there. Alan Greenspan kept rates too low for too long. Failing to better regulate the mortgage industry was a major problem. Powell’s predecessors Ben Bernanke and Janet Yellen also kept fire trucks on scene even though the crisis was over. In fact, they even deployed additional trucks (QE2 etc.) long after the recession ended. But Powell is doing it on a vastly larger scale.

This might be tolerable if these financial fire trucks were just parked and waiting. That’s not the case. They are blocking traffic, preventing deliveries, and slowing progress. Their revved-up engines are spewing fumes, choking innocent bystanders. And the highly-skilled firefighters are actually losing their skills as the needless deployment consumes their training time.

Leaving rates at the zero bound is financial repression. It harms savers and retirees. Buying $40 billion worth of mortgage bonds every month to hold down mortgage rates in the midst of an extraordinarily significant rise in housing costs seems counterproductive, especially for first-time buyers.

Even more egregious is the Fed seems to have assumed a third mandate: keeping the stock market rising. Not only does this exacerbate wealth disparity, it borders on malpractice because, at some point, the Fed will have to take its foot off the accelerator. When that happens the potential for another “taper tantrum” is significant. The Fed absolutely should not think the stock market is its responsibility. To do so (as I believe they are) sets up all of us for extreme future volatility.

Supply chain problems are going to get fixed, albeit slower than we would like. Eventually, the fiscal stimulus will go away and everyone will have to adjust. Monetary policy isn’t the solution for that particular problem.

This has to stop. The economy is growing now. Unemployment, while still elevated, is improving. Creditworthy borrowers can easily get financing. Even if another major COVID-19 wave strikes, we have thankfully progressed beyond the need for economy-stifling restrictions.

The emergency is over, at least from the perspective of the need for quantitative easing and low rates. The Fed should bring its fire trucks home.

Unfortunately, that’s not happening… and it’s having an effect.

Slamming the Brakes

Everyone agrees inflation would be a problem if we had enough of it for an extended period. Then the agreement breaks down. Are rising inflation benchmarks “transitory” or will they persist? If they do persist, do they even mean anything for most people?

We wrestled with these questions at the SIC in May (see Expecting Inflation and Deflation Talk). I’ve been more on the “transitory” side, but small differences matter. The Fed has a 2% inflation target. Sounds minor, but 2% annual inflation compounds to 22% higher prices over 10 years. Fed leaders think it’s fine. It is not fine. Even “low” inflation harms savers and consumers.

Worse, the Consumer Price Index is a terrible proxy for consumer prices. It is massaged and adjusted, sometimes for good reasons, but the adjustments disguise inflation’s impact on segments like housing. The “cost of living” grows faster than official inflation for many people, and in some cases far faster. The inflation we see today is especially pernicious for the lower 60% of the income and wealth brackets.

One argument, to which I am somewhat sympathetic, is that this doesn’t matter because the Fed can’t generate inflation even if it wants to. It’s been trying and failing for over a decade. What we see now is less about Fed policy and more about pandemic-driven supply chain disruptions. As that passes, the Fed will be trapped again.

Moreover, some of this is outside the Fed’s control. The rising prices that add up to inflation are the result of producer and consumer expectations for the future. It’s a decentralized, complex process that can easily get out of hand—and force the Fed’s hand.

In general, a loose monetary policy is by definition inflationary. And while Powell can make a real argument about inflation being “transitory,” his monetary policy, coupled with an expansionary fiscal policy, is extending the period of time that we call transitory.

Businesses are raising prices. You can see businesses, small and large, specifically saying so in their quarterly calls, in the Beige Book, and other sources. You can also see it when you go to the store or shop online. Prices are rising. Clearly wages are rising. Those price increases and especially wage increases are going to be “sticky.” Consumer inflation expectations are growing. Inflation fear embedding itself into the average economic mindset. That is dangerous. Those of us who lived through the 1970s know inflation expectations have a way of becoming ingrained.

The always-excellent Jesse Felder described it well in one of his letters last week (Over My Shoulder members can read it here), A brief excerpt:

… (T)he Fed might be able to afford to pursue the most aggressive monetary policy experiment in US history so long as inflation expectations remain in check. However, if inflation expectations take off then the jig is up.

Because once inflation expectations become unanchored, consumer and business behavior shifts in a way to ensure that inflation is more than “transitory.” People begin stockpiling things they fear they won’t be able to get in the future due to rising prices or shortages. This pushes up prices further, exacerbating these very fears, inspiring even more stockpiling and so on.

At this point, the Fed would be forced to break the inflationary psychology by rapidly reversing monetary policy to something far more hawkish than almost any market participant can imagine today. For some perspective, the last time core CPI hit 4.5%, as it did last month, the Fed Funds rate was over 5% versus 0% today.

As Mohamed El-Erian put it, “The facts on the ground call for the world’s most powerful central bank to start easing its foot off the stimulus accelerator. By refusing to do so, the Fed runs a higher risk of having to slam the policy brakes down the road.” The longer the central bank waits to curb inflationary psychology, the harder they will have to hit the brakes when the time comes.

See, at some point inflation gets worse simply because enough people expect inflation to get worse. Then what?

In the 1970s, Burns and then Miller accommodated that inflation, not wanting to risk recession in order to control inflation. Then things got out of hand. Rather than small, controlled tightening efforts, we needed a massive shock to the system, producing the worst back-to-back recessions since World War II.

That’s how we got Paul Volcker, incidentally. Jimmy Carter installed him in 1979 because inflation was so high. Volcker then did what should have been done earlier. Neither Powell nor any likely successors appear eager to normalize Federal Reserve policy. That creates severe economic danger, possibly forcing the Fed toward things it doesn’t want to do.

Force-Feeding Liquidity

There’s another way to look at the inflation question: Maybe we actually have major inflation already. Instead of CPI or PCE, it’s showing up mostly in asset prices—mainly stocks and residential real estate. Both have risen significantly lately, arguably due to Fed policies and programs.

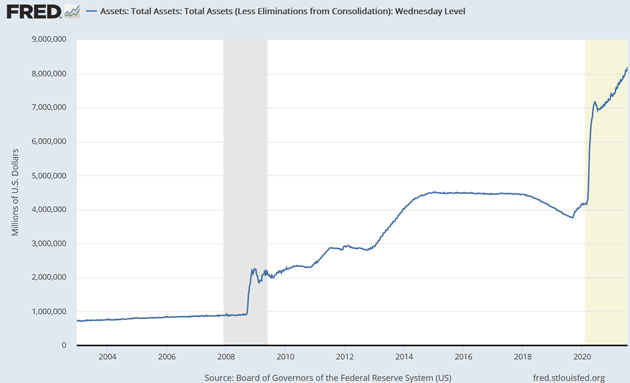

The connection is real. Stock prices and home prices both respond to liquidity, and the Fed is stuffing the economy with as much liquidity as it can. It injects another $120 billion into Treasury securities and mortgage-backed securities every month. Recent activity far outstrips what they did in the Great Financial Crisis and following, which was itself unprecedented at the time.

Source: FRED

Look at the upper right of this chart. That sharp vertical line is the Fed responding aggressively and quickly to the unfolding crisis last year. They injected staggering amounts of liquidity which, at the time, made sense. Maybe they overdid it but, like those fire trucks I described above, they erred on the side of having too much help ready. Okay, fine.

But what happened after the initial alarm is less forgivable. Instead of pulling back, they brought in yet more horsepower, as shown in the jagged line. This is why stocks and home prices are rising. It’s not so much the near-zero short-term interest rates, though that helps too. The Fed is simply force-feeding liquidity into the economy and it has to go somewhere. These assets are the path of least resistance.

Now, you might say Fed officials surely know this. Why are they still pumping? An excellent question. We may get an answer someday, years from now, when the people making those calls are able to talk more freely. For now we can only guess, and my best guess is that the Fed is effectively monetizing the giant and fast-growing government debt. They aren’t technically monetizing because they don’t have that authority, but it amounts to the same thing.

But why do that? Why encourage fiscal profligacy? Maybe because they think it will happen anyway, and they want to minimize the economic hit. The alternative is to let the Treasury issue trillions in new debt that would push interest rates far higher. That might end the inflation threat, but would have other serious consequences.

The Right Course

As I’ve said in the past, decades of policy errors leave the Fed with no good options. All the choices are bad and they can only choose the least bad. Not a good position to be in, but it’s where they are. And the rest of us are with them, like it or not.

I was critical during the last period of tightening, with the Fed both raising rates and reducing their balance sheet at the same time. It was a risky two-variable experiment. Today is somewhat different. Here’s what the Fed should do, in my opinion:

-

Slowly begin reducing balance sheet growth, say by $10 or $20 billion a month, and sometime early next year begin slowly raising the Fed funds rate, meeting by meeting, Greenspan style.

-

Stop being an arm of the US Treasury, which they certainly appear to be today, and let the government be responsible for its own mistakes.

The Fed’s primary job is to control price inflation. I think its obsession with 2% inflation is a serious mistake. It’s not “price stability” to reduce everyone’s buying power by 22% in 10 years and 50% in 36 years.

It is certainly not beneficial to retirees who no longer have the ability to earn income and under the current financial repression can’t even keep up with inflation. And while I know that Congress gave the Fed a mandate to maximize employment, nobody has been able to explain to me how monetary policy can do that. Yes, low rates make it easier for businesses to expand, but they also harm savers and retirees. Robbing Peter to pay Paul distorts markets.

I would like to go back to a time when we didn’t wake up in the morning wondering what the Federal Reserve would do. Its actions have distorted the economy, repressed savers, and made the wealth and income divide far greater than it should be.

Quick plug: There are things you can do as an investor to hedge/protect/grow your portfolio. I don’t mean the normal approach to markets. There is an entire world of outstanding alternative investments out there. My partners at CMG (where I serve as the chief economist) and AlphaCore have an entire menu of options. We call it the Mauldin Kitchen. Click on the link to see our special white paper What’s In Your (Investment) Kitchen? A representative from Team Mauldin will call you and show you what’s in my kitchen.

By the way, over the last month, we had a “small” opportunity to participate in a very unique income fund, mostly funded by large, well-known endowments and pensions. Our connectivity gave us a small slice that we showed to current clients. You really do want to be at the table when those opportunities present themselves. It didn’t take a lot of time to develop that relationship, but it will pay big dividends.

Washington, DC, Maine, Colorado, and Personal Losses

I plan to go to Washington, DC, for a few days before heading out to Grand Lake Stream for Camp Kotok, the annual fishing and economic fest. This year my youngest son Trey (who is now 26) will once again accompany me, which he has done for most years since he was 12. Then I will go to Steamboat, Colorado, for a speaking engagement at Gobundance. Sounds like a fun group.

Those of us of a certain age begin to notice more and more of our friends “shuffle off this mortal coil” way too frequently. This week I was deeply grieved that my longtime friend Toby Goodman died of a heart attack at the relatively young age of 72. He was my personal/family lawyer but so much more. He personally rewrote the family law code while he was in the Texas House of Representatives. He was deeply involved in the community, but to me he was a confidant and friend. It is without exaggeration that I can say we shared at least 100 Italian meals, talking politics, philosophy, and personal lives. Requiescat in Pace, Toby.

On a lighter note, Shane and I and friends went to a small park in downtown San Juan and took salsa lessons. It was fun, and we will do it again, but you won’t see me on Dancing with the Stars. Maybe Shane. And Trey and Tiffani, granddaughter Lively and friends show up this next week.

And with that I will hit the send button. Don’t forget to follow me on Twitter. I seem to binge once or twice a week, and for the most part enjoy the intellectual back and forth.

You have a great week. I think I will spend more time on the phone with friends.

*********

********

More from Silver Phoenix 500