New Economic Report Card Shows That The US Still Has The Competitive Edge

America’s still got it.

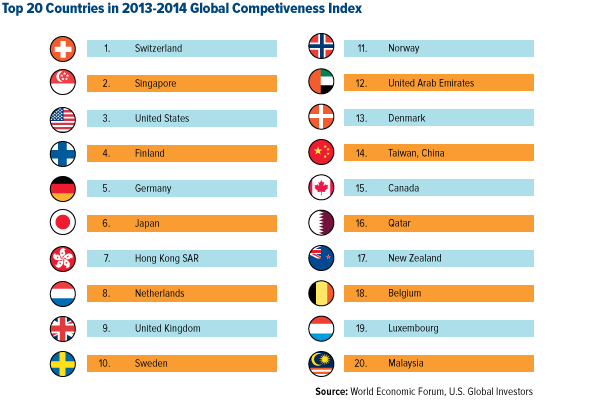

That’s according to the latest Global Competitiveness Report, which names the U.S. the third-most competitive nation in the world, our highest ranking since 2008.

For 10 years now the World Economic Forum (WEF) has published its annual competitiveness report, which assesses the strength of 144 countries’ 12 “pillars,” including institutions, infrastructure, health and primary education and higher education. It then ranks these countries based on their overall ability to promote prosperity for their citizens.

Singapore retains its number two spot for the fourth straight year, while Switzerland leads for the sixth year in a row.

From 2006 until 2008, the U.S. held the top position, but following the financial crisis, our ranking slipped to number seven in 2012.

This year, the WEF notes:

“U.S. companies are highly sophisticated and innovative, and they are supported by an excellent university system... Combined with flexible labor markets and the scale opportunities afforded by the sheer size of its domestic economy—the world’s largest by far—these qualities make the United States very competitive.”

You might be thinking: But wait, didn’t China’s economy just exceed our own?

Yes and no.

It’s true that, when U.S. and China’s economies are not adjusted for costs of living, the U.S. is still “the world’s largest by far.” Our GDP stands at around $16.8 trillion whereas China’s is $9.3 trillion.

But based on purchasing power parity (PPP), a calculation that factors in relative costs of living to make comparisons between and among countries “fairer,” China has indeed caught up with and surpassed the U.S.

This news might bruise some readers’ egos, but it’s actually a tailwind for both commodities and our China Region Fund (USCOX). China is such an important player in the global economy that it’s nearly impossible for any serious investor to see China’s ascent as anything but positive.

Below are some of the key takeaways from the Global Competitiveness Report.

Strengths

The economic report card gives the U.S. many accolades, including its capacity to attract and retain talented people from abroad. I always say that when people want to innovate and start businesses, they typically come here to the United States. The report reveals it’s relatively easy in the U.S. for “entrepreneurs with innovative but risky projects to find venture capital.” Our financial services are strong, and we have ready access to bank loans for sound business plans. When it comes to the ease of raising money by issuing shares on the stock market, we come in at sixth place, following Hong Kong, Taiwan, South Africa, New Zealand and Qatar.

Only Switzerland beats us in our capacity for innovation.

Only Switzerland beats us in our capacity for innovation.

We score very well in our availability and corporate adoption of the latest technologies, as well as availability of scientists and engineers, quality of scientific research institutions and company spending on R&D. We rank eleventh in the number of patent applications filed under the Patent Cooperation Treaty (PCT), amounting to 149.8 per one million U.S. citizens.

In the business sophistication pillar, we excel above all other countries in our use of sophisticated marketing tools and techniques.

Areas for Improvement

It comes as no surprise that the top three most problematic factors for doing business in the U.S., according to the report, are tax rates, tax regulations and inefficient government bureaucracy. It’s for these reasons that some businesses, including Burger King, Medtronic and Chiquita, are in the process of moving their corporate headquarters to countries with friendlier tax rates—Ireland, Canada and Singapore, among others.

To prevent such tax inversions from occurring, our tax code sorely needs amending. Our 35-percent corporate income tax rate is the highest among the 34 member nations of the Organisation for Economic Co-operation and Development (OECD), and we actually rank 32 out of 34 in the 2014 International Tax Competitiveness Index. Only Portugal and France fare worse.

To prevent such tax inversions from occurring, our tax code sorely needs amending. Our 35-percent corporate income tax rate is the highest among the 34 member nations of the Organisation for Economic Co-operation and Development (OECD), and we actually rank 32 out of 34 in the 2014 International Tax Competitiveness Index. Only Portugal and France fare worse.

Indeed, the Global Competitiveness Report shows that, to a large extent, taxes reduce the incentive to work: in this department we come in at number 37, just between China and Ghana. As for wastefulness of government spending, we rank number 73, trailing France by one point and China by 49 points. The report also shows that it can often be difficult for some businesses to comply with U.S. government regulations.

If our government were to simplify the tax code and ease regulations, there’s no doubt that the U.S. could once again claim top honor.

Other crucial areas for improvement include quality of electrical supply (we come in at number 24, following Barbados), soundness of banks (number 49), gross domestic secondary enrollment rate (59) and quality of math and science education (51).

Emerging Countries

Some of the emerging markets that we track at U.S. Global Investors either made gains this year or maintained their positions.

Poland, for instance, held on to its rank of 43. The WEF noted the country’s “improvements… in institutions, infrastructure and education,” its “increased flexibility in labor market efficiency” and its “[c]ontinued structural reforms geared toward strengthening its innovation and knowledge-driven economy.” A well-educated population and secure financial market make Poland globally competitive, but to truly boost its innovative capacity, it needs to improve its infrastructure, soften regulations and make settling business disputes more efficient.

Greece jumped 10 spots to reach the rank of 81. Despite its high levels of government debt, the Mediterranean country has managed to improve the functioning of its goods and labor markets and reduce its budget deficit. However, its government is still inefficient and its financial market has yet to recover from the recent crisis that hit parts of Europe. A lack of access to financing is the most problematic factor for doing business in Greece.

Other key emerging markets that rose up the list were China, Malaysia, Thailand, Indonesia and the Philippines.

Keep Investing in America

Despite a few areas for improvement, the United States is still the preeminent place on earth to invest, with plenty of openings for growth. As we continue to recover from the recession, now is the most opportune time in years to place your trust in America’s future.

Our two U.S. equity funds, All American Equity Fund (GBTFX) and Holmes Macro Trends Fund (MEGAX), have been impacted by the global economic slowdown and growth scare. Cyclical stocks—the kind we focus on in these two funds—have lagged defensive stocks, by about 6 percent in the last month and a half.

Cyclicals are those types of goods and services consumers can afford to purchase when the economy is performing well. Examples include discretionary-type companies such as Apple, Priceline and Tesla Motors. Defensives, on the other hand, typically remain stable, even in times of market downturns. Examples include electricity, gas and food.

This might sound like troubling news, but we view it as an opportunity. As you can see, a similar discrepancy between cyclical and defensive stocks occurred in April and May of last year, and yet mean reversion corrected it. We’re optimistic that such a turn will occur again, which means that now might be an ideal time to accumulate cyclicals.

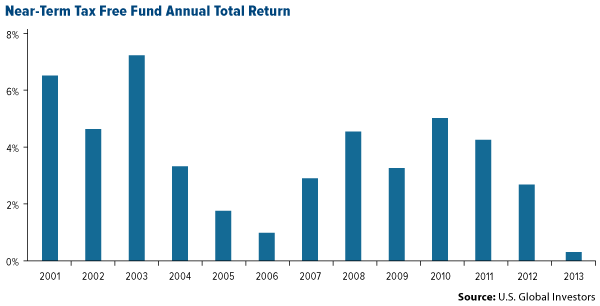

Another way to potentially capitalize on our nation’s successes is U.S. Global Investors’ Near-Term Tax Free Fund (NEARX), which invests in high-quality, U.S. municipal bonds. A significant portion of the fund is invested in health services, public schools and higher education, three of the 12 pillars that the WEF assesses. To keep these services operational and efficient, state and local governments rely on funding from the very bonds we invest in, which in turn improves Americans’ livelihood as well as the businesses they run.

Another way to potentially capitalize on our nation’s successes is U.S. Global Investors’ Near-Term Tax Free Fund (NEARX), which invests in high-quality, U.S. municipal bonds. A significant portion of the fund is invested in health services, public schools and higher education, three of the 12 pillars that the WEF assesses. To keep these services operational and efficient, state and local governments rely on funding from the very bonds we invest in, which in turn improves Americans’ livelihood as well as the businesses they run.

Although past performance is no guarantee of future results, NEARX has delivered positive tax-free income for the past 13 years. The fund seeks preservation of capital and has an attractive floating $2 net asset value (NAV) that has demonstrated minimal fluctuation in its share price.

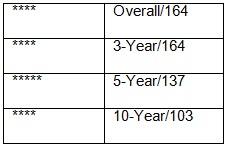

Because of its risk-adjusted returns, NEARX has earned the coveted five-star rating from Morningstar* for the five-year performance period and four stars overall. Check out its performance here.

To learn more about how you can help keep the United States competitive, I encourage you to request an information packet.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Morningstar ratings based on risk-adjusted return and number of funds

Category: Municipal National Short-Term Funds

Through: 09/30/2014

Bond funds are subject to interest-rate risk; their value declines as interest rates rise. Tax-exempt income is federal income tax free. A portion of this income may be subject to state and local income taxes, and if applicable, may subject certain investors to the Alternative Minimum Tax as well. The Near-Term Tax Free Fund may invest up to 20% of its assets in securities that pay taxable interest. Income or fund distributions attributable to capital gains are usually subject to both state and federal income taxes. The Near-Term Tax Free Fund may be exposed to risks related to a concentration of investments in a particular state or geographic area. These investments present risks resulting from changes in economic conditions of the region or issuer. Though the Near-Term Tax Free Fund seeks minimal fluctuations in share price, it is subject to the risk that a decline in the credit quality of a portfolio holding could cause a fund’s share price to decline. Stock markets can be volatile and can fluctuate in response to sector-related or foreign-market developments. For details about these and other risks the Holmes Macro Trends Fund may face, please refer to the fund’s prospectus. Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio.

Morningstar Ratings are based on risk-adjusted return. The Morningstar Rating for a fund is derived from a weighted-average of the performance figures associated with its three-, five- and ten-year (if applicable) Morningstar Rating metrics. Past performance does not guarantee future results. For each fund with at least a three-year history, Morningstar calculates a Morningstar Ratingä based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund’s monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in the distribution percentages.)

The Global Competitiveness Index, developed for the World Economic Forum, is used to assess competitiveness of nations. The Index is made up of over 113 variables, organized into 12 pillars, with each pillar representing an area considered as an important determinant of competitiveness: institutions, infrastructure, macroeconomic stability, health and primary education, higher education and training, goods market efficiency, labor market efficiency, financial market sophistication, technological readiness, market size, business sophistication and innovation.

The Tax Foundation’s International Tax Competitiveness Index (ITCI) measures the degree to which the 34 OECD countries’ tax systems promote competitiveness through low tax burdens on business investment and neutrality through a well-structured tax code. The ITCI considers more than forty variables across five categories: Corporate Taxes, Consumption Taxes, Property Taxes, Individual Taxes, and International Tax Rules.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the funds mentioned as a percentage of net assets as of 09/30/2014: Burger King (0.00%), Medtronic (0.00%), Chiquita (0.00%), Apple, Inc. (4.35% in All American Equity Fund, 4.56% in Holmes Macro Trends Fund), The Priceline Group, Inc. (3.00% in All American Equity Fund, 3.03% in Holmes Macro Trends Fund), Tesla Motors, Inc. (2.09% in All American Equity Fund, 2.93% in Holmes Macros Trends Fund).

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content. Past performance does not guarantee future results.

********

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. Fund portfolios are actively managed, and holdings may change daily. Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

More from Silver Phoenix 500