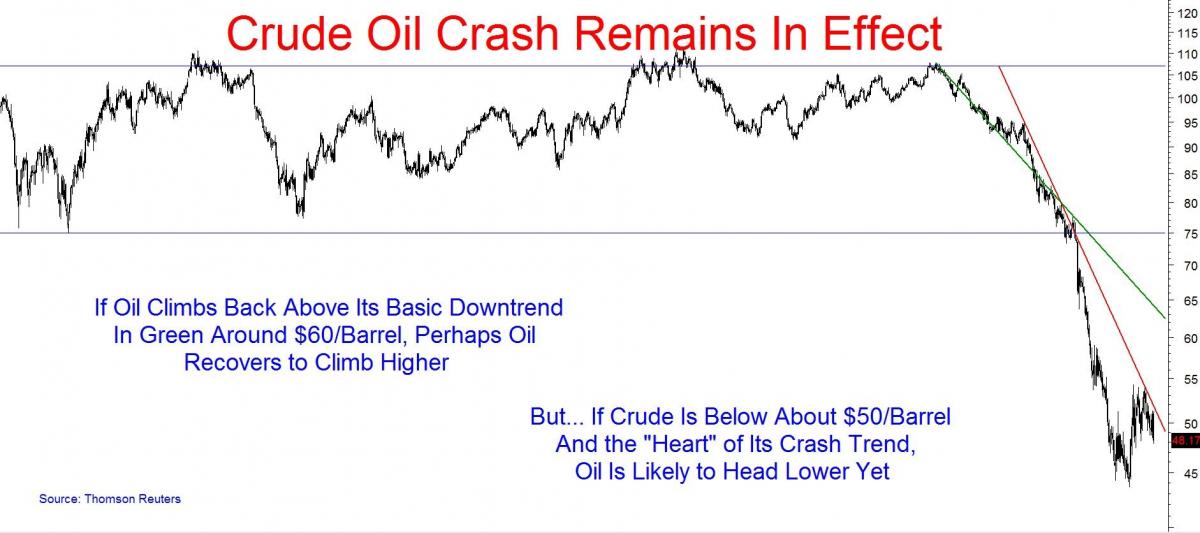

Oil: Will It Go Lower Yet?

Crude oil’s various charts suggest that the effects of its recent crash have yet to play out fully and that crude oil may drop to between $30 and $35/barrel in the near/medium-term and perhaps much lower over the long-term.

A continued decline in crude oil could prove to be a tailwind for consumers, and thus for the U.S. economy with consumer spending accounting for about 70% of GDP. However, this could be outweighed by the possibility of potential ripple effects carrying through into the bond and currency markets and, eventually, into the mainstream equity markets. It would not be surprising to us, in fact, if the equity markets are disrupted by an equally violent correction as has occurred in crude oil.

Our Bottom-Line: (1) Consider avoiding/reducing long exposure to crude oil-related securities until there is significant reason to believe that a “bottom” has been found, and, (2) consider preparing to invest in a defensive manner that could go beyond sector rotation into a possible reduction of equity exposure.

GFG Market Insight – PDF

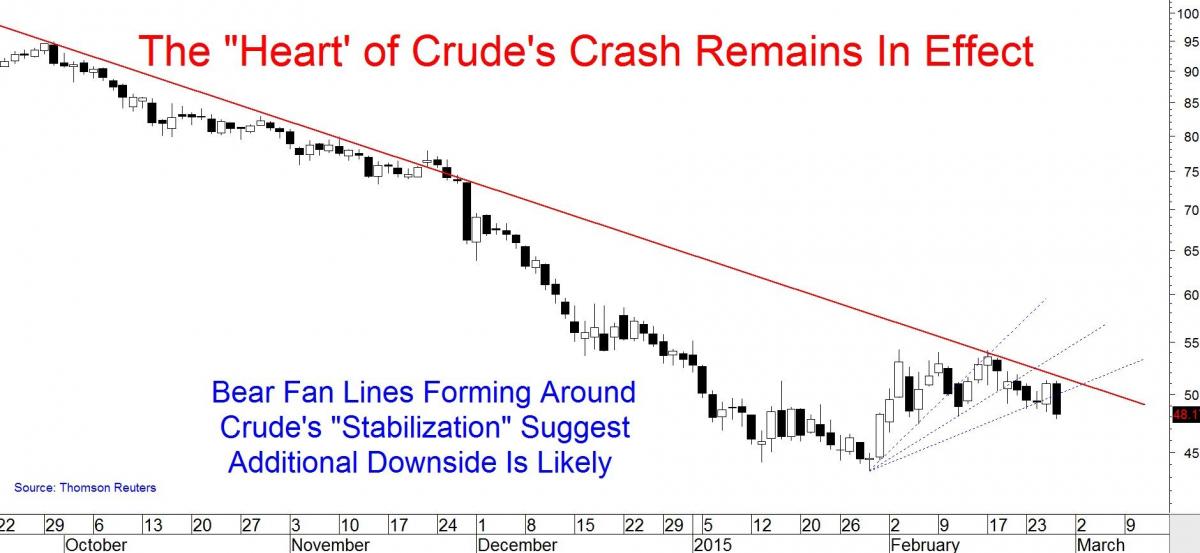

After crashing down by more than 50% from its 2014 peak in six months, crude oil has stabilized more recently around $50/barrel. It is tempting to believe that this stabilization is a sign that crude oil is setting up for a move higher, but we tend to believe that it is more likely a pause before crude oil goes even lower.

Our bearish view is based primarily on analysis of crude oil’s charts over various time frames and it suggests crude oil is likely to fall to at least $30 to $35/barrel but may find a true bottom below $15/barrel. These numbers are not thrown out lightly and so let’s turn to the charts that suggest crude oil may settle at pre-Bush era lows.

Crude Oil Near-Term

But the recent appearance of Bear Fan Lines (drawn in dotted blue) suggests that crude is more likely to make a measured move down to about $28.18/barrel.

Typically when Fan Lines appear, whether of the Bull or Bear variety, it means that the implicated reversal action is likely to take place.

In this case and not to confuse matters, the trend behind the Fan Lines is up, and thus the staged movement below the Bear Fan Lines suggests that the nascent uptrend is starting to reverse as the sellers stay in control. This is in keeping with the punishing downtrend of crude oil’s crash.

It is important, however, to recognize that the very appearance of some buying support in recent weeks suggests that there could be a bitter bull/bear battle in the near/medium-term as crude trades in a volatile but somewhat directionless manner.

Above about $60/barrel on a weekly closing basis and the bulls may “win” take control of the near-term sideways trend for what could be a real move higher, but below about $50/barrel on a weekly closing basis and the sellers may usher in the next phase of the crude oil crash.

It is worth noting that aggravated sideways battles seem typical among commodities before a sudden and violent move down, in our view, and this may prove true too of GFG Market Insight – PDF GFG Market Insight 02 27 2015crude oil such that another potential leg down seems to come out of “nowhere.”

Turning to the true medium-term, crude’s crash is made that much more stunning when shown as an absolute collapse from a long-established sideways trend. It is the speed out of that neutral trading range that explains why crude oil’s true downtrend is well above that of its crash downtrend as shown by the very generously drawn trendline in green.

Source: Thomson Reuters

Crude Medium-Term

All of this is to say that the sellers “won” the medium-term sideways battle and have been in total control of crude oil for eight months now.

And despite the near-term congestion or aforementioned “pause” and something that does show some life on the part of the buyers as discussed above, there is no question that the sellers are in control of crude oil at this time. This remains true so long as that stunning downtrend is in effect as measured by its trendlines.

One good technical reason to think that crude oil’s medium-term downtrend may remain in effect is shown by the long-term quarterly chart on the following page.

Displayed well by this chart are the various paths of crude oil’s long-term uptrend over the last 32 years as shown by the several ascending trendlines.

At this time, it is unclear where crude will find support to recover and climb higher. There is a possibility that this platform was found recently as shown by the green trendline around $44/barrel and one that we discussed in December as a “best case scenario” for crude oil’s decline when it had not yet cracked below $50/barrel.

Source: Thomson Reuters

Crude Long-Term

Perhaps this will prove true, but we doubt it.

At a minimum, this quarterly chart suggests that crude is likely to drop to one of the three trendlines below its current position at about $39/barrel, $28/barrel or about $13/barrel.

Interestingly, making the best case for a continued decline in crude oil are the Bear Fan Lines created by the uptrend that started in 1998.

As was discussed earlier, it is very rare for such a defined uptrend reversal to stop and reverse before dropping well below the trendline marking the third stage of the uptrend reversal and one created in this case by crude’s recent crash.

Plus, from a truly old school technical perspective, most of the unmarked patterns plaguing crude oil’s charts at this time suggest that its minimum decline will be to at least $35/barrel if not much lower. This includes the massive Symmetrical Triangle behind crude’s crash that is clearly resolving to the downside.

Overall, then, crude oil’s charts make a compelling case, in our view, for a continuation of its collapse and a possibility that suggests oil may go lower yet.

********

Investment Advisory Services offered through Greenbush Financial Group, LLC. Greenbush Financial Group, LLC is a Registered Investment Advisor. Securities offered through American Portfolio Financial Services, Inc. (APFS). Member FINRA/SIPC. Greenbush Financial Group, LLC is not affiliated with APFS. APFS is not affiliated with any other named business entity. Abigail Doolittle is a registered representative with Americn Portfolio Financial Services, Inc. Information in this illustration has been obtained from sources believed to be reliable and are subject to change without notification. The information presented is provided for informational purposes only and not to be construed as a recommendation or solicitation. Investors must make their own determination as to the appropriateness of an investment or strategy based on their specific investment objectives, financial status, and risk tolerance. Past performance is not an indication of future results. Investments involve risk and the possible loss of principal. Any opinions expressed in this discussion are not opinions or views of American Portfolio Financial Services, Inc. (APFS) or Greenbush Financial Group, LLC. Options expressed are those of the writer only. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not ensure against market risk. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

More from Silver Phoenix 500