Orphaned Silver Is Finding Its Parent

Introduction

So far this year, the story in precious metals markets has been all about gold. Speculators have this idea that gold is a hedge against inflation. They don’t question it, don’t theorise; they just assume. And when every central bank issuing a respectable currency says they will print like billy-ho, the punters buy gold derivatives.

These normally tameable punters are now breaking the establishment’s control system. On Comex, the bullion establishment does not regard gold and silver as money, just an idea to suck in the punters. The punters are no longer the suckers. With their newly promised infinite monetary expansion, central banks are confirming their inflationary fears.

What makes it worse for bullion bank trading desks is that the banking system is now teetering on the edge of the greatest contraction of bank credit experienced at least since the 1930s, and banks are determined to rein in their balance sheets. We normally think of bank credit contraction crashing the real economy: this time, banks are reining in market making activities as well, and that includes out-of-control gold and silver trading desks, foreign exchange trading, fx swaps and other derivatives —anything that is not a matched arbitrage or an agency deal on behalf of a genuine customer.

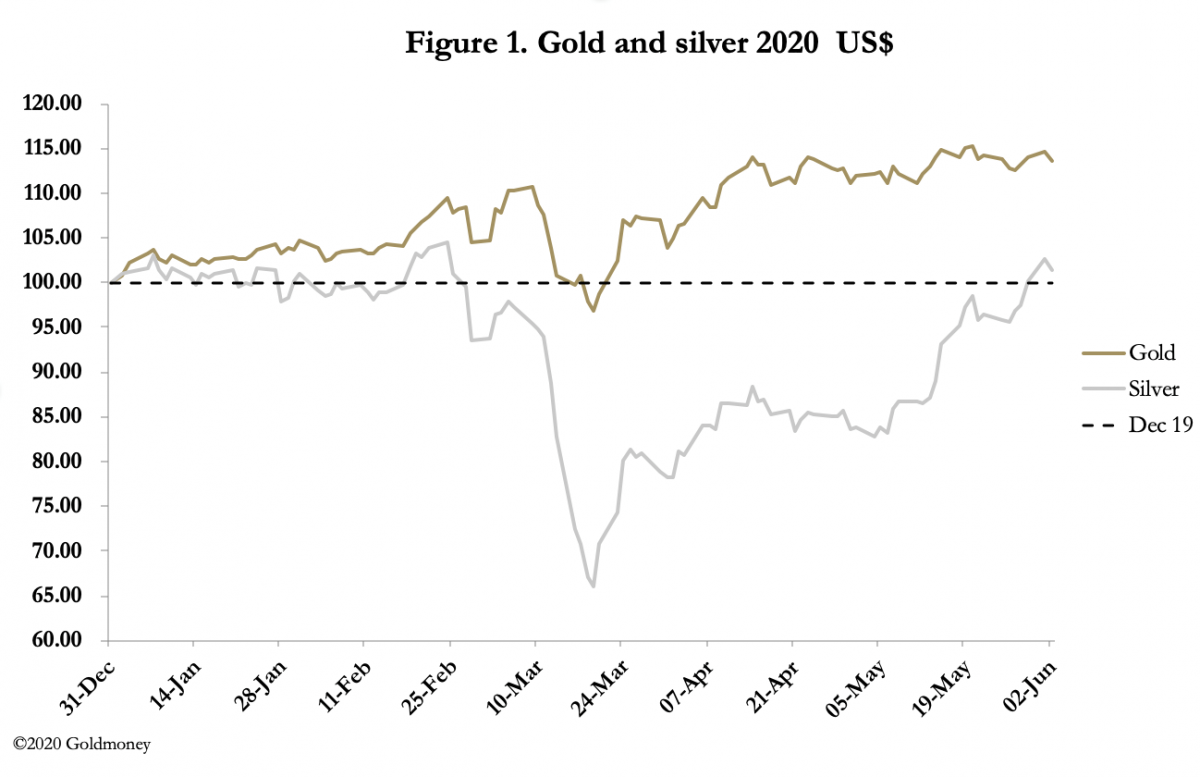

Initially, the focus on gold left silver vulnerable. Figure 1 shows how the two metals have performed in dollar terms so far this year, indexed to 31 December 2019. When the bullion banking establishment tried one of its periodic smashes in mid-February, it reduced Comex gold futures’ open interest from just under 800,000 contracts to about 480,000. The price of gold bounced back strongly to be up 14% on the year and the bullion banks are still horribly net short. But silver crashed, losing 34% and has only just recovered to be level on the year so far.

For the punters, in a proper gold bull market silver is seen as just a leveraged bet on gold. They are less interested in the dynamics that cause a relationship to exist than they are on the momentum behind the price. For now, active traders are looking for entry points in both metals to build or add to their positions in a bullish but overbought market.

This is just short-term stuff, and much has been written on it about gold. We are generally unaware today that silver has been money for ordinary people more so than gold and in that sense still has the greater claim as a circulating medium. It is therefore time to devote our attention to silver.

A brief history of monetary silver

Silver has a similar history to gold of being money. Following the ending of barter, communities worldwide adopted durable metals – gold, silver or copper, depending on local availability — as the principal medium of exchange. And until the 1960s this heritage, with respect to copper and silver, was still reflected in the coinage used in most nations. The British currency is still known as sterling because since the reign of Henry II (1154–1189) money was silver coinage of sterling alloy, comprised of 92.5% silver, the balance being mainly copper.

Silver was the sole monetary standard, sometimes with gold on a bimetallic standard, for most regions from medieval times until the nineteenth century. Sir Isaac Newton reset the silver standard against gold in 1717, and it was because the British government overpriced gold and failed to adjust to the consequences of changing mine supplies, principally the subsequent expansion of gold supply from Brazil, that British commerce moved towards a gold standard during the eighteenth century.

We look in greater detail at these events later in this article.

As international trade developed, gold for trading nations assumed greater significance, leading eventually to the adoption of the British sovereign coin as the gold standard in the early nineteenth century.

In colonial America, silver was the principal circulating currency in common with that of Britain at the time, but following Newton’s introduction of a silver standard for the pricing of gold, similar practical relationships between the two metals existed for trade in nearly all Britain’s colonies; in America’s case at least until independence was formally gained by the Treaty of Paris in 1783.[i]

When Alexander Hamilton was Treasury Secretary, the US introduced a bimetallic standard with the first coinage act in 1792 when the dollar was fixed at 371.25 grains of pure silver, minted with alloy into coins of 416 grains. Gold coins were also authorised in denominations of $10 (eagles) and $2.50 (quarter eagles). The ratio of silver to gold was set at fifteen to one. All these coins were declared legal tender, along with some foreign coins, notably the Spanish milled silver dollar, which had 373 grains of pure silver making them a reasonable approximation for the US silver dollar.

However, not long after Hamilton’s coinage act was passed, the international market rate for the gold/silver ratio rose to 15.5:1, which led to gold being drained from domestic circulation, leaving silver as the common coinage. Effectively, the dollar was on a silver standard until 1834, when Congress approved a change in the ratio to 16:1 by reducing the gold in the eagle from 246.5 to 232 grains, or 258 grains at about nine-tenths fine. An additional adjustment to 232.2 grains was made in 1834. After a few years, gold coins then dominated in circulation over silver, the circulation of which declined as it became more valuable relative to gold. Gold discoveries in California and Australia then increased the quantity of gold mined relative to silver, making silver even more valuable relative to gold coinage thereby driving it almost totally out of circulation. This was remedied by an act of 1853 authorising subsidiary silver coins of less than $1 to be debased with less silver than called for by the official mint ratio and less than indicated by the world market price.

Under financial pressure from the civil war, in 1862 the government issued notes that were not convertible either on demand or at a specific future date. These greenbacks were legal tender for everything but customs duties, which still had to be paid in gold or silver. The government had abandoned the metallic standards. Greenbacks were issued in large quantities and the United States experienced a substantial inflation.

After the war was over Congress determined to return to the metallic standard at the same parity that existed before the war. It was accomplished by slowly removing greenbacks from circulation. The bimetallic standard, measuring the dollar primarily in silver, was finally replaced with a gold standard in 1879, reaffirmed in 1900 when silver was officially relegated to small denomination money.

In Europe, most countries on a silver standard moved to gold after the Franco-Prussian war (1870–1), when Germany imposed substantial reparations from France which were paid in gold, and Germany was then able to migrate from a silver to a gold standard. Other European nations followed suit.

More recently, silver circulated as money in Arab lands in the form of Maria Theresa dollars, which had circulated widely in the Middle East and East Africa from the mid-nineteenth century and were still being used in Muscat and Oman in the 1970s.

These are just some examples of silver’s use as money in the past. It lives on in base metal coins today, made to look like silver. Now imagine a world where fiat currencies are discredited: gold or gold substitutes will almost certainly return as the money for larger transactions, and silver will equally certainly return as money for everyday transactions. Bimetallism might not return as official policy due to the frequent adjustments required, but history has shown that a relatively stable market rate between gold and silver is likely to ensue, and silver more than gold will ensure widespread distribution of circulating metallic money.

Supply and demand factors

Analysts are currently grappling with the effects of the coronavirus on supply and demand in their forecasts for the rest of this year. Silver mines have been affected by changes in grades and production shutdowns. According to the Silver Institute, in 2019 less than 30% of mine supply was from mines classified as primarily silver, the rest coming from lead/zinc, copper, gold mines and “others” in that order of importance. Miners of lead/zinc, copper and others made up about 56% of global silver mine supply, so that a decline in global economic activity automatically leads to a decline in silver output from base metal miners.

At the same time, falling industrial demand for silver throws a greater emphasis on investment to sustain demand overall. Last year, non-investment demand was 806 million ounces, while investment was estimated at 186 million, a relationship which in a deep recession will require a significant increase in investment demand to absorb the combination of mine, scrap and available above-ground stocks. Identifiable above-ground stocks are estimated at 1,651 million, a multiple of 1.67 times 2019 demand, and 8.9 times 2019 investment demand.

For 2020 and beyond, I am very bearish for the global economy for reasons stated elsewhere. If I am right, current estimates for mine supply, of which over half is dependent on base metal mines, will prove optimistic. But silver demand for non-investment usage is likely to decline even more, in which case investment demand will probably need to at least double if silver prices are to rise in real terms.

An interesting point is found in the comparison with gold, where above-ground stocks are many multiples of mine and scrap supply. Stock-to-flow comparisons have been popularised recently by the cryptocurrency community as a measure of future monetary stability, compared with that of infinitely expandable fiat currencies. A high stock-to-flow signals a low rate of inflationary supply. Silver has a very low stock to flow ratio due to the low level of above-ground stocks. But it is a mistake is to rely on this measure of monetary stability for a metallic money when the lack of physical liquidity should be the main consideration.

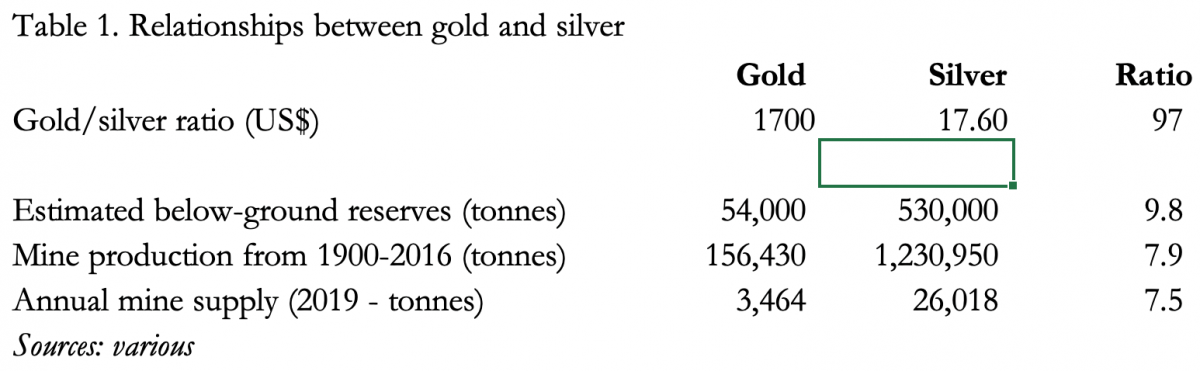

At current prices, silver’s above-ground stock is worth only $31bn, compared with gold’s at over $10 trillion. With this relationship of 323 times of gold to silver’s above-ground stock values and an annual mine supply ratio of only 8 times as many silver ounces to that of gold, it appears that if gold returns to its traditional monetary role, silver will turn out to be substantially undervalued. “If” is a little word for a very big assumption; but given the unprecedented and coordinated acceleration of monetary expansion currently proposed, an ending of the current fiat currency regime and a return to gold and silver as monies is becoming increasingly likely.

The relationship with gold in the numbers above suggest that a bimetallic standard today on mine supply considerations alone would be at almost half Isaac Newton’s 1717 exchange rate. Obviously, the issue is not so simple and will be settled by markets. But looking at some other facts suggest the gold/silver relationship is due for a radical rethink. Table 1 below lists some of the relevant ones.

The clear outlier is the gold/silver ratio.

How Newton decided the gold to silver ratio

It is natural to assume that the greatest scientific genius of the day derived a clever means to settle the gold/silver ratio when he was Master of the Royal Mint in 1717. Not so. He looked at existing exchange rates, how silver was disappearing from circulation in favour of gold at that time and set an initial rate to stop it. Furthermore, he recommended the rate be revised, most probably downwards, in the light of how trade developed. The point was that Britain operated a silver standard of money and both Newton and Parliament wished to retain it. It was, after all, the established money for day-to-day transactions.

To understand the monetary debates at the time, it will be helpful to commence with a guide to the composition of pre-decimal British money and coinage. There were 20 shillings to the pound (£), and twelve pence to the shilling. Silver coins were crowns (5 shillings) and half crowns, being 2 shillings and 6 pence, written 2s. 6d. There were silver coins of lesser value, but they are not relevant to this discussion.

Over a century before Newton, in 1601 a pound weight of old standard silver was coined into £3. 2s. 0d. in crowns and fractions thereof and remained the mint price of silver until 1816, a period lasting over two centuries. In 1670, a pound in weight of gold was coined into £44. 10s. 0d., represented by gold pieces of ten and twenty shillings. That was the equivalent of 14.35 times the value of silver. A monetary pound of twenty shillings was called a guinea, because when they were first struck in 1663 the gold came from the Guinea Coast of Africa, and it was set at 44 ½ to a pound of silver in weight because it was thought that it would be a stable rate of exchange.

There were some adjustments to the price of gold until it was finally fixed in 1717 at the new ratio of £46. 14s. 6d. to the silver standard of £3. 2s.0d. This moved the guinea from £1 in silver to £1. 1s. 0d, or 21 shillings. The crude ratio was now 15.07 to 1; but allowing for the differences in fineness between the slightly purer sterling silver (92.5%) compared with Crown gold coinage at 22 carats (91.67%), the actual ratio was 15.21 to 1.

This rate of exchange was introduced during Isaac Newton’s tenure as Master of the Royal Mint from 1699. In 1696 he had been previously appointed Warden of the Royal Mint to improve the state of silver coinage, and he organised the Great Recoinage in 1696–9.

In setting the price of gold, Newton found that gold, having been fixed as high as 22s. in 1699, had been too expensive compared with its silver value in Europe, particularly Holland, Germany, the Baltic States, France and Italy. Not only did he recommend setting the gold guinea at 21s, but he also recommended the rate be kept under review for a possible change to 20s 6d. That review did not take place.

Trade between Britain and the Continent was increasing, and whatever the rate, merchants had a preference for gold over silver because it was more practical for large payments when they were made in specie, which was normal practice at the time. While Britain remained on a silver standard, for commercial purposes it had increasingly moved to gold, silver being relatively expensive at the rate set and therefore progressively driven from active circulation relative to inflows of gold. The problem was that neither Newton nor Parliament accepted there was more than one currency: silver was the money and gold just a commodity whose price was to be set.

Because silver was valued about 5% more relative to gold in the European countries mentioned in the penultimate paragraph above, silver flowed abroad despite the ban on the export of coinage, and conversely gold flowed into Britain. Furthermore, gold mining output from Brazil began to have an impact on Britain’s monetary system following Newton’s 1717 conversion, due to diplomatic and commercial ties between Britain and Portugal. The bulk of this Brazilian gold, estimated by Fay at about 23 million ounces between 1720–1750, ended up being shipped to London, helping it to become the European monetary centre, taking that mantle from Amsterdam.

We can conclude that it was a combination of Newton overpricing gold, thereby driving silver into Europe and gold into London, and the discovery of Brazilian gold that turned Britain onto a commercial gold standard, even though officially it remained on a silver monetary standard for ninety-nine years after Newton’s fixing. And finally, in 1816, gold was declared the sole standard measure of value, and no tender of silver coin was legal for transactions valued at over forty shillings. By 1821, Britain was on a gold standard in law as well as fact.

From 1601–1816 we learn that silver’s role as money gradually evolved towards a subsidiary role to gold. Gold was the money of merchants and goldsmiths. The latter acting as custodians of gold evolved into banks, so high finance was almost exclusively gold. But silver was always there as money, be it for lesser transactions. And if today’s state-issued unbacked fiat currencies disappear, silver is bound to have a monetary role again alongside gold, because having a lower value and greater abundance of supply it can be more widely circulated.

That being the case, those who believe state currencies are on their way to monetary destruction will accumulate silver as a practical version of sound money, noting that the current gold/silver ratio at about 96 times is over seven times that of its monetary rate in every country that operated a silver or bimetallic standard. Furthermore, those who fear their governments will confiscate gold might observe there is a lesser chance of them confiscating silver and attempts to confiscate gold would probably increase demand for silver anyway.

The current market position for silver

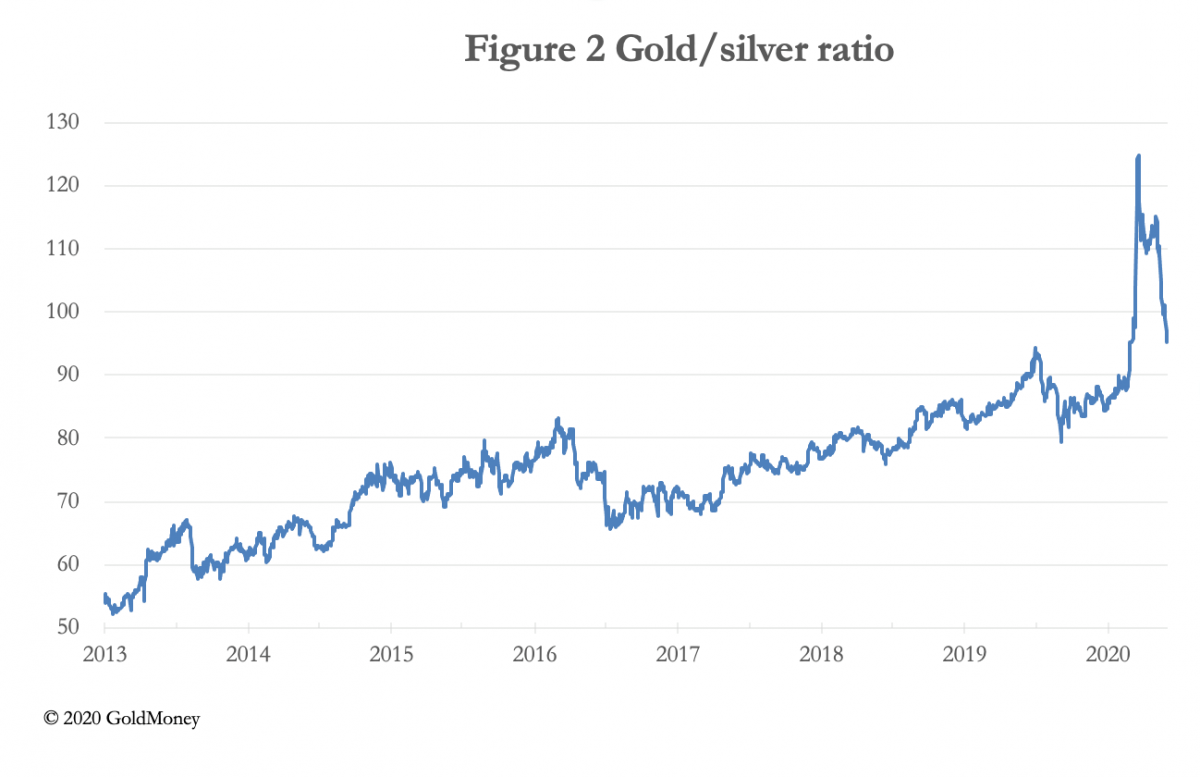

Since the price of gold began to increase from August 2018, silver has lagged, its moneyness broadly ignored. Figure 2 shows how this has been reflected in the gold/silver ratio.

On 19 March a ratio of 125 was the highest ever seen, marking the most extreme undervaluation for silver. Since then, the ratio has fallen rapidly to its current level of 97. For it to fall further a continuing advance in the gold price may be required, because in current financial markets higher gold prices would be associated with economic conditions and monetary policies heading to a substantial, if not catastrophic deterioration in the purchasing power of fiat currencies.

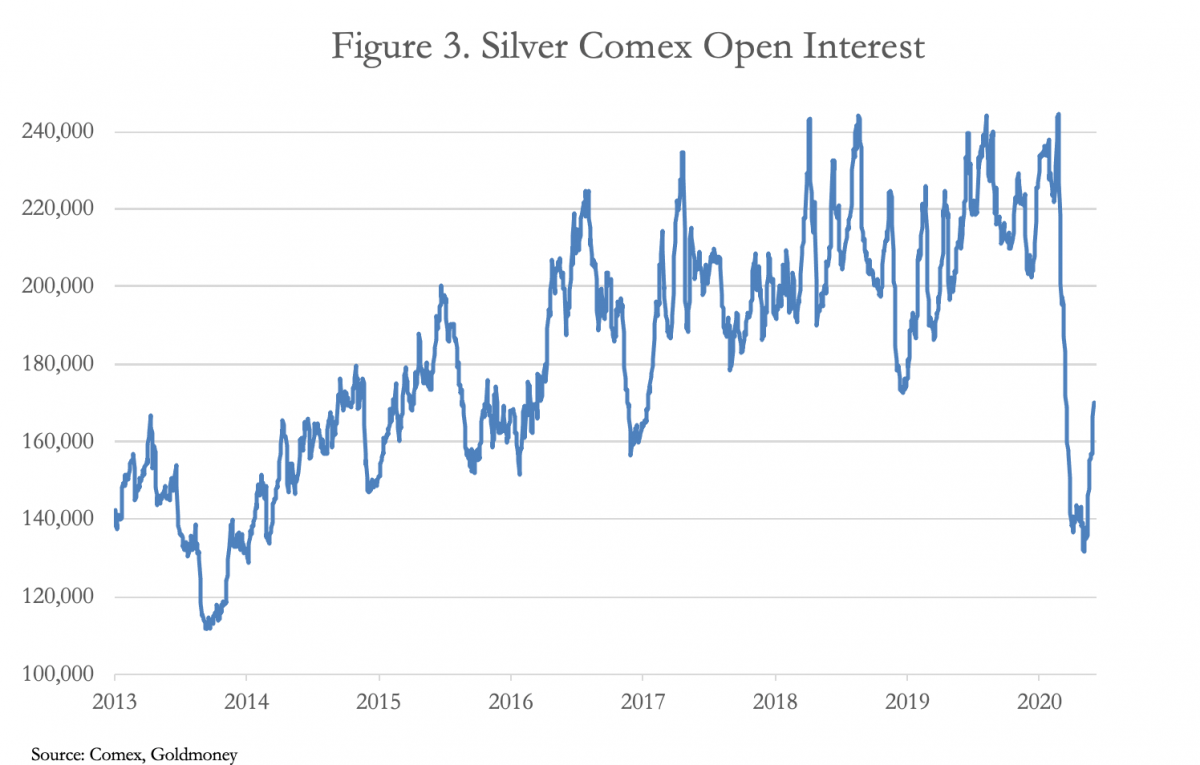

Additionally, traders manning bullion bank desks are generally finding their trading limits being reduced due to a combination of unfavourable trading conditions and pressure from their superiors limiting bank credit expansion generally. When the coronavirus paralysed China and was going to do the same to other nations, and the inflationary response became obvious, it led to a concerted bear raid by the bullion banks to balance their gold and silver positions on Comex before matters got even further beyond their control. The effect on silver’s open interest is shown in Figure 3.

Open interest was driven down to levels not seen for nearly seven years, after the silver price had fallen from a high of nearly $50 an ounce in 2011 to $18 in 2013, a price level only just now being reclaimed. From open interest’s height at 244,705 contracts on 24 February to its low at 181,830 on 4 May, contracts for 314,375,000 ounces of silver have been closed down, which compares with investment demand for the whole of last year estimated by the Silver Institute at 186,000,000 ounces. This contraction amounts to the synthetic equivalent of 20% of the Institute’s estimate of above-ground silver stocks.

Vaulted silver in LBMA vaults was 1,170 million ounces in February, the bulk of the 1.651 million recorded by the Silver Institute. The ownership of that silver is not declared but is likely to be a mixture of industrial users, investors (including ETFs) and bank dealers’ liquidity. In practice, banks keep liquidity at a minimum level consistent with the desk’s trading limits, and we know from developments in other derivative markets that trading limits are tending to contract.

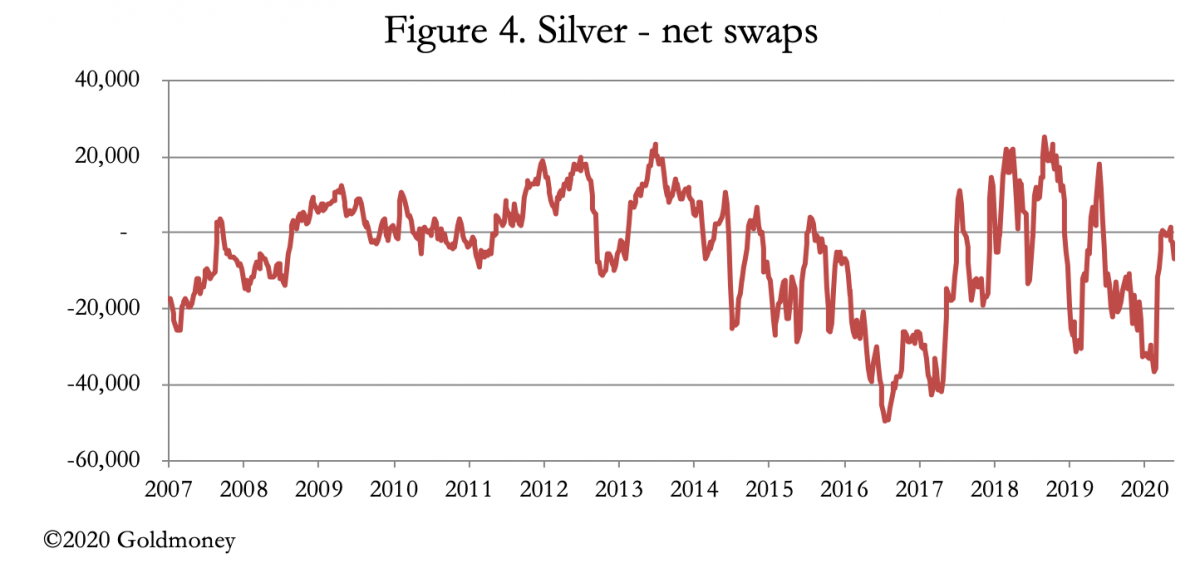

Figure 4 shows the latest available data for the net position of swap dealers, effectively the bullion banks trading desks.

The last commitment of traders’ figures, for 26 May, shows a net short position of only 6,652 contracts; therefor swap dealers positions are almost level. This is a different situation from the gold futures contract where the swaps are currently short a net 182,864 contracts representing the equivalent of 569 tonnes worth $31 billion, almost a record and a major headache for the bullion banks.

In conclusion, having been left behind while monetary events have been focusing on the gold price, silver is now beginning to catch up. The spike to a gold/silver ratio of 125 appears to have marked a major turning point in the relationship, and silver can therefore be expected to continue to outperform gold as the fiat money situation deteriorates. Traders at the bullion banks appear to be avoiding short positions in silver futures, in which case a rising price will see them withdrawing liquidity instead of supplying additional contracts to the buyers.

The global economic and monetary situation is dire, due to both the coronavirus and because the credit cycle was already turning down in late-2019. The amount of monetary debasement deployed by central banks in an attempt to save their economies promises to be unprecedented to the point where total monetary destruction will be an increasingly likely outcome.

That being the case, the attraction of silver over gold is to be found in a substantial fall of the gold/silver ratio, as it dawns on markets that the end of fiat money is nigh.

Alasdair Macleod

HEAD OF RESEARCH• GOLDMONEY

Twitter: @MacleodFinance

MOBILE: +44 7790 419403

Goldmoney

The Most Trusted Name in Precious Metals tm

NEW YORK | ST. HELIER | TORONTO

Publicly Traded Symbols: CA: XAU | US: XAUMF

© 2020 GOLDMONEY INC. ALL RIGHTS RESERVED. THIS MESSAGE MAY CONTAIN CONFIDENTIAL OR PRIVILEGED INFORMATION. IF YOU ARE NOT THE INTENDED RECIPIENT, PLEASE ADVISE US IMMEDIATELY. THIS MESSAGE IS FOR GENERAL INFORMATION ONLY AND SHOULD NOT BE CONSTRUED AS AN OFFER OR SOLICITATION OF AN OFFER TO BUY SECURITIES OR ANY OTHER FINANCIAL INSTRUMENTS. WE DO NOT PROVIDE TAX, ACCOUNTING, OR LEGAL ADVICE, AND RECOMMEND THAT YOU SEEK INDEPENDENT PROFESSIONAL ADVICE IF NECESSARY. WE CONSIDER INFORMATION IN THIS MESSAGE RELIABLE BUT WE DO NOT REPRESENT THAT IT IS ACCURATE, COMPLETE, AND/OR UP TO DATE AND IT SHOULD NOT BE RELIED ON AS SUCH. OPINIONS EXPRESSED ARE OUR CURRENT OPINIONS AS OF THE DATE APPEARING ON THIS MESSAGE ONLY AND ONLY REPRESENT THE VIEWS OF THE AUTHOR AND NOT THOSE OF GOLDMONEY INC OR ITS SUBSIDIARIES UNLESS OTHERWISE EXPRESSLY NOTED.

Notice: This email may contain confidential or privileged information. If you received this email in error or believe you are not the intended recipient, please notify the sender immediately and delete this email without forwarding or opening any attachments. Thank you for your cooperation and attention.

*********

More from Silver Phoenix 500