Perceived Vs. Actual Risks: The Key To Success

Perceived risk is a subjective assessment of risk or uncertainty, based on our limited perspective. Others' perceptions will influence ours, and actual probabilities of adverse events may differ significantly. The market is often a key determiner of perceived risk. A recent sell-off, or misunderstood earnings news, or persistent negative "sector sentiment" can all be indicators of a high level of perceived risk. When such events occur, this can open the door for some great buying opportunities, especially when Mr. Market's perception is wrong about the risk factor, and when the fundamentals are strong.

In fact, many times, Mr. Market will perceive some securities as risky, regardless of their fundamental factors. At the same time, the market may view a company as extremely low risk; however, its fundamentals display otherwise, or vice versa. A critical element of value investing is determining when perceived risk compared to actual risk offers an advantageous trade-off.

For example, in the case of a market sell-off in an entire sector where some significant companies have outstanding fundamentals, those picks are ideal for value investing. When those picks also have a dividend yield that has been increased due to the sell-off, it moves into "high yield" investing territory. Consider two examples, one from the past and one from the present.

A High-Yield Investment from the Past

To give you an idea of what we are looking for, take Digital Realty Trust (DLR). Today, DLR trades at $136, however, back in May of 2013 many people thought that $70 was a high price. At the time, Jonathon Jacobson of Highfields Capital Management LP released this article on Bloomberg urging investors to short the security. This caused the share price to plunge and the yield to upsurge (as can be seen in the chart below). Soon, the price was such that the yield - which had been a steady 4% - had sharply increased to over 6%.

The price, which peaked at just over $72 in late April 2013, had dropped to just under $50 by that November, with a significant decrease right at the end of October. Perceived risk was extremely high.

A closer examination of the company's operations revealed that the company's actual risk was very low. Future results proved that Jacobson’s article was incorrect on several points. Those who purchased DLR shares at that time and overlooked the siren call of his hedge fund's recommendation received an extremely attractive yield at a great price. Meanwhile, the hedge fund is likely to have benefited from the fact that a significant number of institutional investors followed their advice.

DLR paid a quarterly dividend of $0.78 per share in 2013. The next year, it was increased to $0.83 per share. Investing in the company while the market regarded it with disfavor was a great investment. Between July 2013 and July 2014, one could purchase shares with a yield of over 5%, and at times even over 6%. The average share price was around $54 and the average yield was 5.8%. Using the dollar cost averaging method, where you buy a fixed dollar amount of shares at regular intervals, would likely improve those values. A hundred shares purchased around that time would give you a quarterly dividend payment of $78. As of today, those shares have a quarterly dividend of $116.

However, you might say that we are in 2021, not in 2013. And DLR trades around $136 these days, and while $1.16 is a great quarterly dividend when the share price is in the $50s, or even below $70, when the share price is $136, that doesn't produce a lot of income. So, which companies currently pay a generous, healthy, and well-covered dividend, yet they’re out of favor with the market today?

One of Our Top Picks for 2021: NEWT

Newtek Business Services (NASDAQ: NEWT) is a BDC (Business Development Company) that was perhaps the most effective among its peers at turning the lemons of COVID into lemonade. NEWT currently yields 7.8%. NEWT has always been one of the more creative and innovative BDCs and that has led to it producing outstanding returns since its IPO. One of the main drivers for its success is that it is an internally-managed company, whereby the management owns 4.5% of the company's shares, which is significant.

Let's take a look at this security to explain the importance of knowing the difference between perceived and actual risk.

NEWT is no ordinary BDC: The vast majority of its income isn’t the result of holding loans as they mature, but the result of loan origination (including the "Paycheck Protection Program" or PPP loans, and SBA loans). NEWT sells most of the loans and immediately books its profits, so it carries very little credit risk. In 2021, NEWT will get a big boost from the new stimulus with more PPP programs and SBA loans, and huge growth from loan origination.

Additionally, NEWT provides comprehensive business and electronic services and solutions to small businesses, in conjunction with its lending activities. The "secret sauce" of its success is that it's able to cross-sell its services to its clients, in addition to getting significant referrals to new businesses. This has resulted in very fast growth.

The perceived risk here is that investors take a look at NEWT's valuation and think that it is expensive because its price is trading at a huge premium to its NAV (Net Asset Value) compared to other BDCs. However, the fact is that despite NEWT being classified as a BDC, its profitability has little to do with that of a typical BDC. Almost all BDCs are lenders and make money on their "net interest spread", and therefore are bond-like instruments and price/NAV is very significant.

However, in NEWT’s case, the vast majority of its income consists of "loan origination", loan servicing fees, and dividend income from its small business service units. So this company carries very little "interest rate risk" and should therefore be valued based on its Price/Earnings ratio rather than its price/NAV ratio. Today NEWT trades at just 12 times its forward P/E ratio, which is cheap for a fast-growing company. Remember, based on its business model and profitability, this is NOT a BDC-like company.

Fundamentally, NEWT’s actual risk is low, despite the perceived risk. NEWT is set to have a stellar year in 2021 and see its 10% dividend yield grow significantly, thus rewarding shareholders with more income. NEWT will be one of the biggest beneficiaries from the big stimulus spending and the recovery of the small and medium-size businesses which represent the heartbeat of the U.S. economy.

Value Investing Means Recognizing Risks

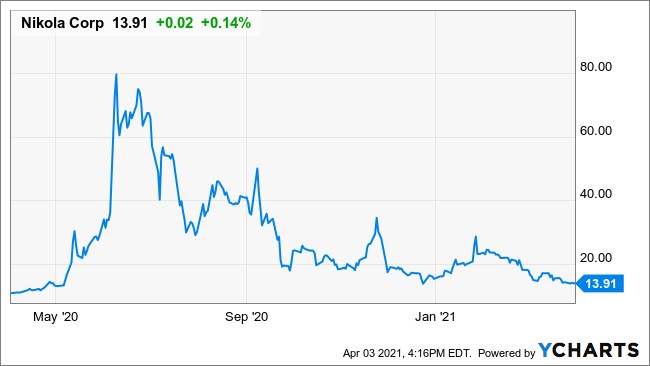

Value investment often entails defying public opinion. Even if the fundamentals scream to the contrary, high positive sentiment always leads to low perceived risk. Although the company has nothing to show for the hype, Nikola (NKLA) had huge amounts of positive sentiment in the electric vehicle sector.

As investors woke up to this fact, many were burned. Value investors must look past the noise of public opinion and into the rational land of fundamentals. This is where actual risk can be assessed.

Dividend Stocks Pay Off

Dividends have the added advantage of offering continuous reassurance when they come in. Investors get some relief from anxiously watching share prices, with the encouragement of dividends received. When you realize that a company's real risk is low and that the market's perception of risk is distorted in some way, you can stop pursuing high-actual-risk, low-perceived-risk investments due to the fear of missing out. This also stops you from selling a perfectly good investment out of panic because others are afraid to keep it.

This actively demonstrates that you can confidently buy on dips without fear. This also justifies you holding on to very profitable companies that others are afraid of due to perceived risk, so that they end up losing out on big capital gains.

When companies offer a dividend you like, and the actual risk is low, buying when you have cash available is the best course of action. There's no need to gamble or time the market to get the "highest" yield. Nobody knows when something will rise or fall - not you, not me, not anyone else.

Working on being able to see through perceived risks and evaluate actual risks takes experience and skill. No one gets it exactly right every time. We're here to help with our years of experience trading in the market.

You've got this. We can assist you. Don't be afraid of taking a risk because someone else thinks it's dangerous. Don't fall prey to irrational exuberance; instead, be aware of the risks. Please feel free to join our investment community to help you learn faster. If you don't want to join, you should still read our articles here, because our goal is to not only find opportunities but also to educate investors of all levels.

Final Thoughts

Investors in the accumulation phase will have regular and steady cash deposits from both dividends and additional deposits. Finding stocks that are trading at a discount or a good price and buying them will grow one's income over time. Even investors who are using most of their dividends to live on and pay their expenses, will from time to time have some cash to invest. They too can use that extra cash to add to dividend-paying stocks, to further boost their portfolio’s income.

Buying high-dividend stocks when the prices are cheap can add an upside to your income growth. The more you invest in dividend stocks, the more your future income rises. Buy cheap dividend stocks today as the valuations are very attractive! Keep in mind that there are many benefits to investing in dividend stocks.

*********

Rida Morwa recently joined the ElliottWaveTrader.net analyst team, bringing his hugely popular High Dividend Opportunities service, the largest-known service for income investors and retirees, with over 4000 members, and featuring a model portfolio with a 9-10% overall dividend yield. Free 15-day trial available here.

More from Silver Phoenix 500