Revenge Of The Kress Cycle

Throughout most of 2014, economists were convinced that the threat of deflation had been successfully bypassed thanks to Fed intervention. Indeed, many celebrated economic forecasters have been loudly cheering the mostly solid-looking economic data throughout most of this year. But as Yogi Berra once said, “It ain’t over ‘til it’s over.”

The Kress 60-year cycle of inflation and deflation, known as the Super Economic Cycle, was scheduled to bottom this October. The bottom of the cycle may well be in, but the deflationary pressure it has helped create hasn’t bottomed yet. If the downward spiral of commodity prices generated by the final “hard down” phase of the cycle this summer and fall isn’t reversed soon, we may end up seeing “Revenge of the Kress Cycle” coming to a theater near you.

Put another way, the incessant meddling and intervention by the U.S. Federal Reserve in recent years may have staved off the deflationary impact of the final years of the 60-year cycle after the credit crash. But as Mr. Kress himself was wont to say, “The Fed ultimately can’t beat Mother Nature and Father Time.” The years of artificial suppressing the natural cycle of deflation may have created a cyclical backlash, a counter-wave if you will, that could witness a confluence of falling prices across several major financial markets around the world.

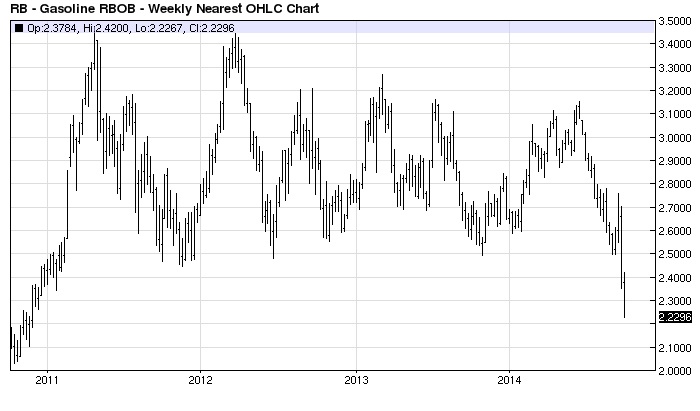

There have definitely been premonitions of such a deflationary backlash in just the last few weeks. One of the most conspicuous of proofs that deflationary currents are at play is the drastic decline in petroleum prices. Consider that gasoline prices have been plunging and are now at their lowest level in almost four years.

Since oil and gas prices are among the most important variables in determining prices of all sorts of goods, it stands to reason that as oil prices fall it will eventually lower prices on the retail level. It has long been the observation of top cycle analysts that a failure of the oil price to decline in a meaningful fashion before long-term deflation reaches its nadir would do irreparable damage to the economy once the next long-term inflation cycle kicks off. If retails prices enter a renewed inflation cycle at a high level, the return of cyclical inflationary pressures down the line will only serve to strain the economy in the form of higher living costs. Seen from this perspective, the plunge in oil and gas prices is a blessing in disguise.

Oil isn’t the only major commodity to suffer the ravages of deflation. Prices for a large basket of commodities have continued to slide in recent months. The Dow Jones Commodity Index has fallen over 10% year-to-date since commodities peaked in late June. Most losses to commodity prices have come since then, which corresponds to the final descent of the Kress cycle. Falling demand and prices for commodities has hurt countries which rely heavily on industrial exports, including China and many European countries.

Europe’s economic powerhouse Germany, for instance, has been particularly hard hit by the sanctions imposed upon Russia in the wake of the Ukraine crisis. Manufacturing orders for Germany dropped 5.7% in August, which is the lowest level in over a year. The country’s industrial production plunged 4.3% in August to the lowest reading since January 2013, according to Ed Yardeni.

In the wake of these recent developments, economists have modified their forecasts and are predicting deflation in the euro zone as EU monetary policy remains tight. ECB president Mario Draghi has made attempts at raising prices by hinting at a U.S. Fed-style QE initiative, but so far his plans have been stymied as policy makers in Germany refuse to endorse it. For now the European Union remains mired in an economic malaise with no stimulus effort on the immediate horizon.

Assuming Mr. Kress’s dictum that “the cycles will always prevail” is true, let’s examine some possible scenarios for the final resolution of the long-term deflationary cycle. The first possibility is that of a Kress cycle compression. Simply stated, this scenario would mean that most of the deflationary damage has already been done and that the short-term will only witness some residual damage, followed by gradual recovery in equity prices as well as oil prices.

The next possibility is that of a Kress cycle inversion. An “inversion” is a term used by Mr. Kress to describe what happens on rare occasions when a major cycle bottom essentially transforms into a top, leading to an extended decline beyond the time frame of the original cycle. An example of this was seen in the final stage of the credit crash of late 2008. While the worst of the damage was seen in the third and fourth quarters of 2008 when the 6-year Kress cycle was bottoming, there was additional spillover damage into the first quarter of 2009 before stock and commodity prices put in their final lows. The (temporary) failure of the 6-year cycle bottom to reverse the downside momentum in late 2008 was due to a lack of confidence among market participants. It took reassurance from the Fed and from Washington in the form of massive stimulus before investors felt confident enough to commit to buying once again.

Currently, investors are perhaps waiting for the U.S. elections next month before making major commitments in the financial market. Meanwhile, foreign investors aren’t budging until they see the promised stimulus efforts from Europe’s central bankers and policy makers. If this “wait-and-see” attitude persists it could give credence to another Kress cycle inversion, just as it did in 2008.

The market may also be waiting to see if the Fed reverses course on its stated intention of raising interest rates sometime next year and instead introduces more stimulus measures if the deflationary pressure continues. Certainly much more in the way of stimulus is expected of Europe’s and Japan’s central banks, and aggressive policy actions from both regions will likely be seen in the coming months.

Meanwhile there is a growing realization on Wall Street that perhaps the winding down of the Fed’s quantitative easing initiative was premature. If the Kress cycle inversion scenario is realized and prices continue to slide, the Fed will be confronted with the possibility that emergency stimulus measures are needed to reverse the damage and prevent full-blown deflation.

If recent market developments have done nothing else, they have proven the celebrations of economists and pundits over the “death of deflation” to be woefully premature. Before the Fed’s vision of a return to “normal” inflation can be realized, it’s clear that more work lies ahead.

********

Mastering Moving Averages

The moving average is one of the most versatile of all trading tools and should be a part of every investor’s arsenal. The moving average is one of the most versatile of all trading tools and should be a part of every investor’s arsenal. Far more than a simple trend line, it’s a dynamic momentum indicator as well as a means of identifying support and resistance across variable time frames. It can also be used in place of an overbought/oversold oscillator when used in relationship to the price of the stock or ETF you’re trading in.

In my latest book, “Mastering Moving Averages,” I remove the mystique behind stock and ETF trading and reveal a completely simple and reliable system that allows retail traders to profit from both up and down moves in the market. The trading techniques discussed in the book have been carefully calibrated to match today’s fast-moving and sometimes volatile market environment. If you’re interested in moving average trading techniques, you’ll want to read this book.

Order today and receive an autographed copy along with a copy of the book, “The Best Strategies For Momentum Traders.” Your order also includes a FREE 1-month trial subscription to the Momentum Strategies Report newsletter:

http://www.clifdroke.com/books/masteringma.html

Clif Droke is a recognized authority on moving averages and internal momentum, two valuable tools which have enabled him to call most major stock market turning points from 1997 through the present. He is the editor of the Momentum Strategies Report newsletter, published three times a week since 1997. He has also authored numerous top-selling books, including “Mastering Moving Averages.” For more information visit www.clifdroke.com

More from Silver Phoenix 500