Review: World Silver Survey 2025

The Silver Institute recently released its highly anticipated annual World Silver Survey 2025 (WSS). It’s one of the few deep reviews of the silver markets, and it’s compiled by Metals Focus for the Silver Institute.

With the benefit of hindsight, the authors look back at 2024 and give us their final numbers for silver supply and demand. In addition, they provide their outlook for 2025.

I will summarize what I think are the key points and trends, and where my views differ.

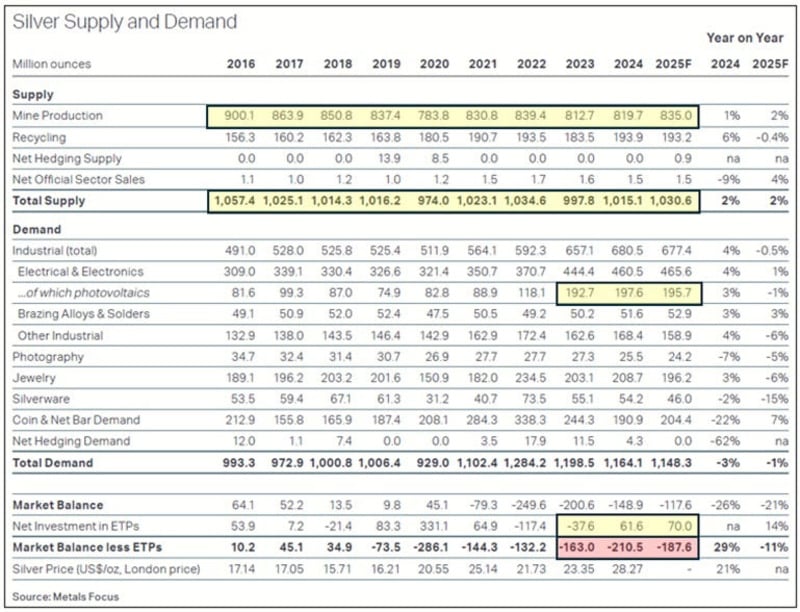

For reference, here are the supply and demand data for the past 10 years from the Survey:

Supply

Silver supply came in nearly flat, up just 2% over 2023. Mine output gained 1%, while recycling was up a more significant 6%. However, recycling represents only 19% of overall supply, with mining accounting for the rest.

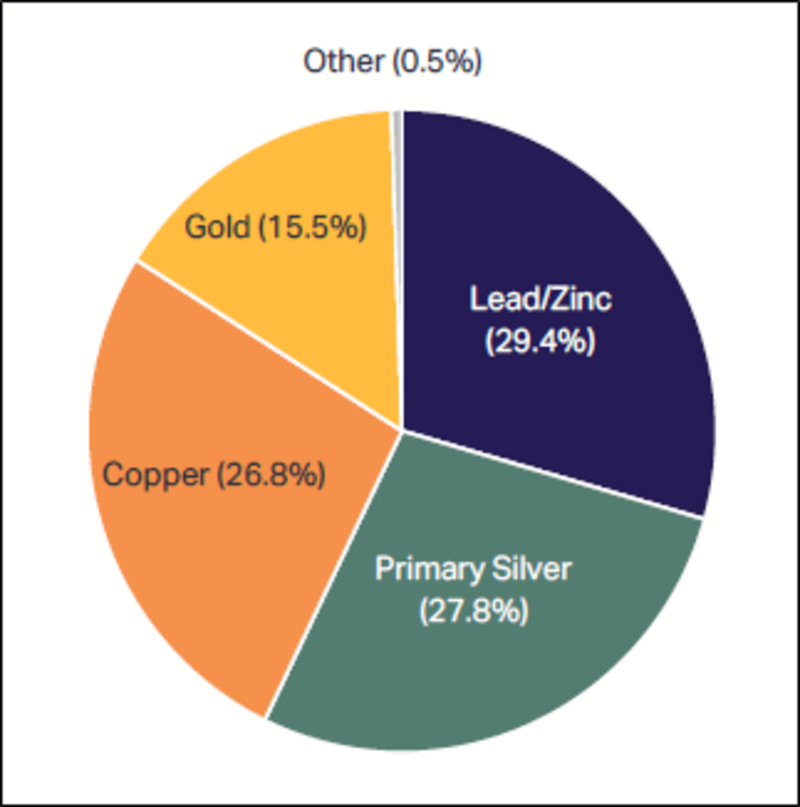

Interestingly, supply from primary silver mines continues to fall, down 2%. This chart shows silver mine production by source metal last year:

The Survey forecasts mined output to rise again this year by 2% as Mexico, Chile, and Russia grow production. Notably, Bolivian silver production reached a record high of 47.9 Moz.

It seems most of the rise in silver production was a byproduct of higher gold production. Strong and rising gold prices would explain higher gold output. Fully 72% of silver output was derived as a byproduct, with lead and zinc leading the way.

Silver production costs were down, with cash costs at $7.64 (down 15% over 2023) and AISC at $14.58 (down 13% over 2023), mainly due to higher byproduct metals prices. Intuitively, we might expect higher silver production as profits are attractive at current prices. But high silver prices do little to motivate miners who produce silver as a byproduct.

Recycling supply of silver was up 6%, mostly from industrial sources, and more specifically from the processing of spent ethylene oxide catalysts. There was also growth in jewelry scrap (+8%) and silverware (+11%). Higher silver prices and challenging economic conditions likely led some to sell their silver.

Demand

The Survey indicates that overall demand was down slightly in 2023 and again in 2024 (-3%). The biggest contributor here is coin and bar demand for physical silver (-22%), as well as photography (-7%) and silverware (-2%).

Total industrial demand was up 4% to reach 680.5 Moz, though it’s expected to be nearly flat (-0.5%) in 2025.

The WSS sees overall electrical and electronics (including solar) to be up 1% this year, solar down -1%, photography -5%, jewelry -6%, and silverware -15%. They expect coin & bar demand to be up 7%.

Here’s one area where I differ with the Survey. They indicate that demand from solar (photovoltaics) came in at 197.6 Moz for 2024. Their forecast back in April last year was for 232 Moz. I think the actual demand was closer to their forecast.

Recent research by BMO Capital Markets says they see solar consuming 246 Moz silver this year, up 5.5% from 2024. That would peg 2023 demand at 233 Moz, which is nearly exactly what the World Silver Survey had forecast for 2024.

The WSS has forecast solar demand for silver at 195.7 for 2025. BMO has forecast a rise to 261 Moz. That’s a difference of 33%. I believe that the BMO forecast is likely to come in closer to actual.

The WSS argues that silver loadings – the amount of silver required for each solar panel – will continue to fall, outweighing gains in cell production.

On the other hand, BMO notes that since 2016, the International Energy Agency has significantly underestimated the growth of solar power, which has grown at an annual compound rate of 20% since 2011 and is likely to continue at that pace through 2030. BMO expects overall solar power demand will outweigh thrifting.

BMO also points out that China’s domination of the solar panel market has driven prices down significantly. And despite the U.S. applying tariffs on Asian solar panels to counteract dumping, most of the rest of the world will find such low prices too attractive to overlook.

With the new trend towards deglobalization and self-reliance, the desire to use solar for energy independence will be irresistible.

As BMO explains it, “While some countries (notably the U.S.) will seek to counter Chinese cell dumping to support local industry, we expect that the opportunity to rapidly expand clean energy generation with limited upfront capex will be too enticing to resist for most of the world,” the analysts said.

“As such, we see solar as a market that is effectively not demand-constrained for the foreseeable future.” [emphasis mine]

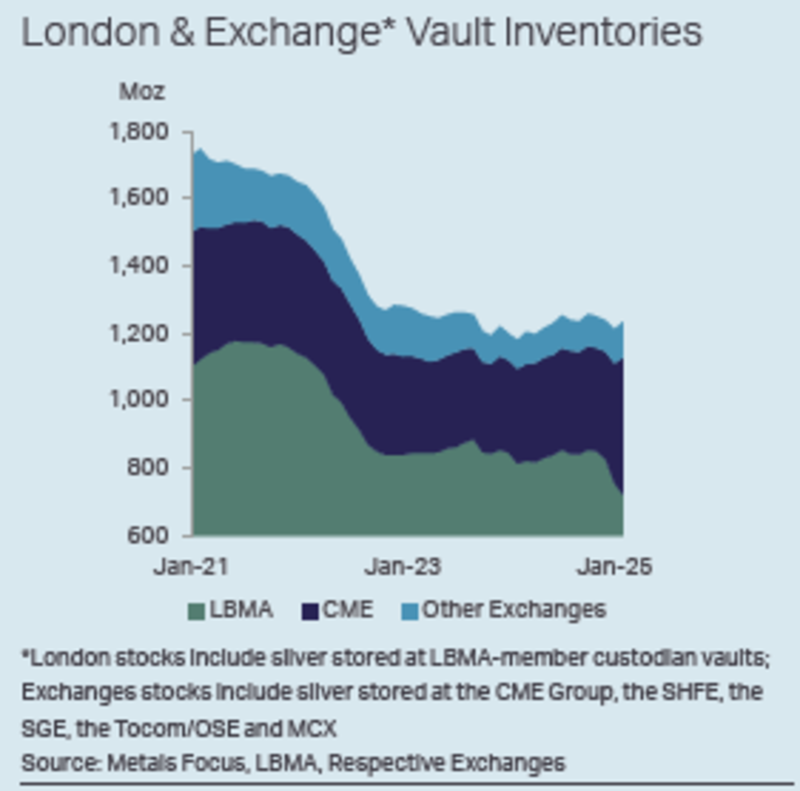

Of course, this again begs the question of why silver hasn’t rallied to much higher levels. The Survey points out that above-ground silver stocks – mainly in London, New York, and Shanghai – have been gradually depleted, helping to meet the ongoing silver deficits of the last four years.

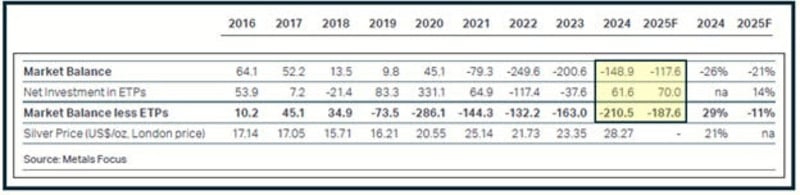

It’s also worth noting that Metals Focus, the group that produces the annual Survey, lists demand from silver ETFs (ETPs) as a separate line item that is not included in overall total demand. The argument is apparently that the silver in ETPs is not consumed, so is technically available to meet demand.

And yet investment demand in coins and bars form is included in overall demand. This makes no sense to me because that silver is not consumed either. It remains available to come back to the market at any time.

My biggest takeaway on this topic is the following. If you consider net investment in ETPs, then the deficit in 2024 was 210.5 Moz, the second highest on record, and the forecast deficit for 2025 is 187.6 Moz, which would be the third highest on record.

Key Takeaways

There are a few key takeaways from the World Silver Survey.

· The authors believe that there is a risk to silver demand from US tariffs that could lead to supply chain disruptions and lower economic growth globally. They feel that would weigh on industrial, jewelry, and silverware demand, but expect physical investment could rise as safe haven demand jumps.

I essentially agree with that conclusion, but feel that industrial demand could bounce back quickly as central banks move to cut interest rates, launch quantitative easing, and governments announce large stimulus programs to counter economic slowdowns.

· Although the past four years have seen a significant supply deficit, the report does not expect mine production to provide any real relief, as they see that peaking in 2026, then falling as several mines reach the end-of-life.

This is a key point as it suggests that deficits will need to be met from above-ground inventories. I think this will mostly happen at much higher silver prices.

One other important takeaway is the swing in net investment in ETPs (see line 2, above table). While that was -37.6 in 2023, it swung to +61.6 in 2024. That’s nearly a 100 Moz swing higher, and the forecast is for another +70 Moz into ETPs this year. If that’s the case, then ETPs will drain available secondary supplies from exchanges and private holdings.

That suggests that ongoing deficits will increasingly have to be met from private holdings as exchange inventories dry up.

In an interview with Kitco News, Metals Focus Managing Director Philip Newman indicated that even after five years of supply deficits, the market remains far from equilibrium: “Ultimately, we still think there's a few years left of a deficit and that should prove to be price positive, even though in the short term we could continue to see some volatility.”

Newman further stated, “…Even in a recession, I don’t think you are going to see demand fall off a cliff. There is always some risk, but I do see some resilience in the silver market.” And he added that economic uncertainty could restart investment demand as silver’s safe-haven status is rediscovered.

In my view, we are looking at ongoing deficits and stronger demand than the WSS is forecasting, likely from both industrial and investment demand.

With that in mind, I expect the silver market’s constrained supplies coupled with robust demand to help drive new highs this year and for many more ahead.

If you found this information insightful, please be sure to subscribe to Peter Krauth's Silver Stock Investor HERE.

********

More from Silver Phoenix 500