Show Me The Stocks, Not The Cash, Say Optimistic CEOs

In early March, I made the case that there’s no greater vote of confidence in a company’s growth prospects than when its top officers put some skin in the game and buy their own company stock. Among the examples I used were Warren Buffett, who owns millions of shares in Berkshire Hathaway; Elon Musk, who purchased over $100 million worth of Tesla stock in 2013; and myself, the largest shareholder of U.S. Global Investors.

Another example of how bullish an executive is on his own company is when he chooses to forego a base salary entirely and instead be compensated in company stock.

The most recent chief executive officer to receive such compensation is American Airline’s Doug Parker.

The most recent chief executive officer to receive such compensation is American Airline’s Doug Parker.

In a letter to employees, Parker wrote:

Going forward, I have asked our Board to restructure my compensation such that I will no longer receive a base salary or an annual bonus. Instead, all of my primary compensation will be paid in AAL stock. This stock will have to be earned over time, and will also have to be earned by performance. I believe this is the right way for my compensation to be set—at risk, based entirely on the results achieved, and in the same currency that our shareholders receive.

Parker has such confidence in his own company and the industry in general that he’s willing to place a huge portion of his financial security in its hands. This, along with American’s recent addition to the S&P 500 Index, should make investors’ ears perk up.

He’s not the only CEO who’s switched to stock.

Fellow airline executive Maurice J. Gallagher Jr. of Allegiant Air has also passed on cash, receiving a little over half a million dollars in stock and options in 2013 alone.

The late, great Steve Jobs was famously paid $1 a year to serve as CEO of Apple—which we own in our All American Equity Fund (GTBFX) and Holmes Macro Trends Fund (MEGAX)—taking his real payment in company shares. In February 2011, a few months before his death, it was reported that Jobs owned about 5.5 million shares in Apple stock, which at the time was worth a little over $2 billion.

Another notable example is Larry Ellison, co-founder and former CEO of computer technology company Oracle, also held in GBTFX. In 2013, Ellison was the most highly compensated CEO out of the 300 who were featured in the Wall Street Journal/Hay group CEO Compensation Study. During his final full year of work at Oracle, he received $67.3 million—nearly all of it in stock options.

Another notable example is Larry Ellison, co-founder and former CEO of computer technology company Oracle, also held in GBTFX. In 2013, Ellison was the most highly compensated CEO out of the 300 who were featured in the Wall Street Journal/Hay group CEO Compensation Study. During his final full year of work at Oracle, he received $67.3 million—nearly all of it in stock options.

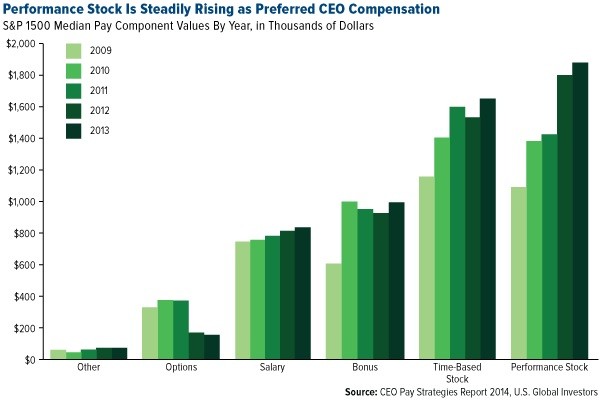

Stock has been steadily growing in importance as a form of compensation for the most successful CEOs. Between 2009 and 2013, performance stock for those leading S&P 1500 Index companies rose 52 percent, the largest increase of any other type of payment. Compared to all other methods, in fact, performance stock is now the most-preferred, according to executive compensation consultancy firm Equilar.

Stock isn’t just good for executives; it’s also good for shareholders.

In a 2010 study piece that appeared in the NYU Journal of Law & Business, Villanova University Business Law Professor Richard A. Booth writes that “stock options are indeed the best form of incentive compensation yet devised” for CEOs. His reasoning: “[I]t is the supposed duty of the directors and officers to maximize stockholder value. In practice, there are few situations in which that duty is enforced as a matter of law. Options fill the gap.”

Although options are a specific type of security, giving the holder the right to buy or sell shares at a later date, they’re used here as a proxy for the broader argument that stock helps executives better align their interests with shareholders’.

Despite Greece, Investors Still Bullish on Europe

You might have noticed that Greece has been in the headlines a lot lately.

Many global investors are anxious to see how the drama unfolds, as the beleaguered Mediterranean country, strapped for cash, is staring down billions of euros in upcoming bailout loan repayments, not to mention salaries and pensions. On May 12, Greece will owe the International Monetary Fund (IMF) 0.8 billion euros, and between the end of July and beginning of August, 7 billion euros in bond payments become due to the European Central Bank (ECB), according to Wood & Company.

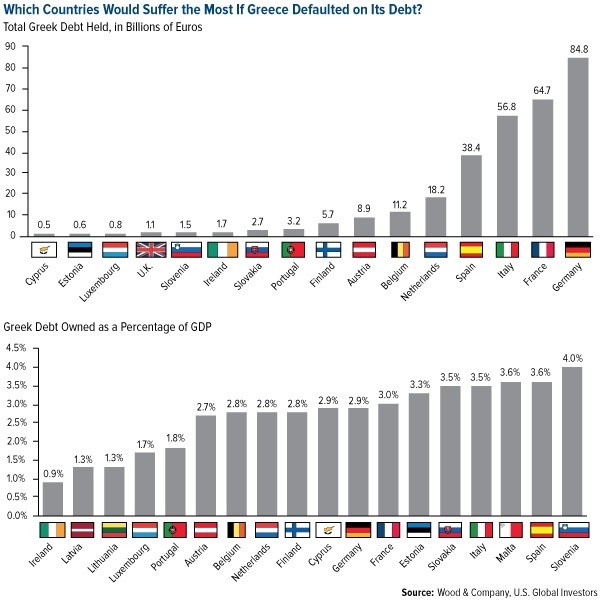

Below you can see which countries would be impacted the most were Greece to default on its obligations. Although Germany holds the greatest amount of Greek debt—over 84 billion euros’ worth—Slovenia would be hurt the worst, as 4 percent of its GDP is tied up in the country’s debt.

Rightfully so, investors are wondering about the implications of a so-called “Grexit” from the eurozone. We don’t expect this to happen, as it would be too great of an economic, political and psychological blow to Greece. The IMF takes the same position. To be clear, the country is indeed running out of cash, and it won’t be able to pay its pensioners and creditors without a deal.

Despite all of the negative press, global investors, including us, are increasingly bullish on both Greece and the eurozone in general. We closely monitor technical indicators such as credit default swap (CDS) spreads, moving averages and money flow, and we’ve seen some promising market moves lately. For instance, Greek banks’ five-day moving average just crossed above both the 20- and 60-day moving averages.

So far this year, investors have added $223 million to a Greek exchange-traded fund (ETF), with short interest on the product falling to its lowest level since April 2013.

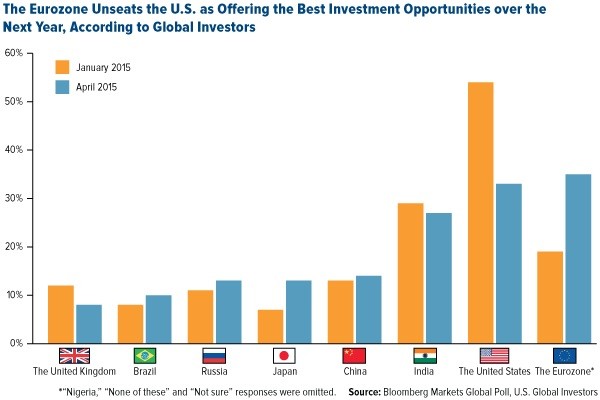

Among 1,280 Bloomberg subscribers, 35 percent recently singled out the eurozone as the one market that will offer the best investment opportunities over the next year, an increase of 16 percentage points since January.

This is all good news for our Emerging Europe Fund (EUROX). We recently added to our Greek position and are now equal-weighted with its benchmark, the MSCI EM Europe 10/40 Index.

To get a better handle on what’s happening in Greece, check out Visual Capitalist’s infographic on the subject.

USGI Portfolio Manager Ralph Aldis Named a TopGun

USGI Portfolio Manager Ralph Aldis Named a TopGun

Last week we learned that Ralph Aldis, portfolio manager of our Gold and Precious Metals Fund (USERX) and World Precious Minerals Fund (UNWPX), was voted into the American Society of TopGun Investment Minds in the U.S. Metals and Mining category by capital markets performance measurement firm Brendan Wood International.

According to the firm’s press release, this honor recognizes investors considered to be “optimal leaders of thought in the industry during the past year.”

Of course, we already knew this about Ralph. As many of you know, the past three and a half years have been among some of the most challenging for metals and mining investing. But under Ralph’s expert management skills, USERX currently holds four stars overall from Morningstar, among 71 Equity Precious Metals funds as of 3/31/2015, based on risk-adjusted returns.

I would be remiss not to recognize all of the support behind Ralph and our other talented portfolio managers. We’re fortunate to have a dedicated team of world-class analysts who often work long hours into the evening researching both macro and micro economic trends and assisting in investment analysis. Ralph’s job would be near-impossible without their tireless efforts.

Congratulations, team!

********

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Past performance does not guarantee future results.

Morningstar ratings based on risk-adjusted return and number of funds

Category: Equity Precious Metals

Through: 3/31/2015

Morningstar Ratings are based on risk-adjusted return. The Morningstar Rating for a fund is derived from a weighted-average of the performance figures associated with its three-, five- and ten-year Morningstar Rating metrics. Past performance does not guarantee future results. For each fund with at least a three-year history, Morningstar calculates a Morningstar Rating based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund’s monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in the distribution percentages.)

Stock markets can be volatile and share prices can fluctuate in response to sector-related and other risks as described in the fund prospectus.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio. The Emerging Europe Fund invests more than 25% of its investments in companies principally engaged in the oil & gas or banking industries. The risk of concentrating investments in this group of industries will make the fund more susceptible to risk in these industries than funds which do not concentrate their investments in an industry and may make the fund’s performance more volatile.

Gold, precious metals, and precious minerals funds may be susceptible to adverse economic, political or regulatory developments due to concentrating in a single theme. The prices of gold, precious metals, and precious minerals are subject to substantial price fluctuations over short periods of time and may be affected by unpredicted international monetary and political policies. We suggest investing no more than 5% to 10% of your portfolio in these sectors.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The S&P 1500 Composite is a broad-based capitalization-weighted index of 1500 U.S. companies and is comprised of the S&P 400, S&P 500, and the S&P 600. The index was developed with a base value of 100 as of December 30, 1994. The MSCI Emerging Markets Europe 10/40 Index (Net Total Return) is a free float-adjusted market capitalization index that is designed to measure equity performance in the emerging market countries of Europe (Czech Republic, Greece, Hungary, Poland, Russia, and Turkey). The index is calculated on a net return basis (i.e., reflects the minimum possible dividend reinvestment after deduction of the maximum rate withholding tax). The index is periodically rebalanced relative to the constituents' weights in the parent index.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the All American Equity Fund, Holmes Macro Trends Fund, Emerging Europe Fund, Gold and Precious Metals Fund and World Precious Minerals Fund as a percentage of net assets as of 3/31/2015: Berkshire Hathaway Inc. 0.00%, Tesla Motors Inc. 0.00%, American Airlines 0.00%, Allegiant Travel Company 0.00%, Apple Inc. 4.03% in All American Equity Fund and 5.34% in Holmes Macros Trends Fund, Oracle Corporation 1.00% in All American Equity Fund.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

More from Silver Phoenix 500