Silver’s Low Reconfirmed?

China has torn up the precious metals world of stats since 2008, with its accumulation of gold to dethrone the USD as the favoured currency for settling contracts in the burgeoning new world and era of Asia.

As if any further drivers were domestically required, stocks in China can only be a catalyst for upward-spiking local demand this year, as those key short term drivers (housewives) lose faith in their favoured casino, returning instead to their favourite investment.

The 1-year chart of the Shanghai index below reflects the wild volatility since Friday, as part of a top-to-bottom smash of ~25% just since June 15! The housewives' stampede will have been part of the market's discounting of this coming October's announcement of China's true gold holdings.

The pursuant 10-year chart of the index illustrates just how extreme the retracement has been of the post-2007 debacle, and why it is reasonable to conclude that the risk is to the downside, evidenced by the Elliott analysis that Wave-5 (final wave per Elliott), which began in February 2015 likely ended last month (the Wave began in early 2014).

This interpretation if further supported by the 1-year chart on which we see a smaller wave-5 ending last month. Based on Elliott, support areas are found in the zone of the previous wave-4, which suggests that we have already seen a completed short term correction though, based on the same rule, no true support kicks in until the 3000 zone (10-year chart).

(Regarding the analysis of the preceding in relation to global currencies and equities, please see the DOW article being published concurrently with report, entitled, "Dow 1987 Redux?")

In any event, regarding China's holdings-related news, be certain that the discounting of October's announcement will have been relatively minor compared to what will have followed over the coming 1-3 years.

Do know the operative word to be, "relatively."

As of 2001, I have been forecasting $3,500 as a major long term level. The only thing that has changed since identifying the secular trough has been the reasonable arguments of many intellectuals as regards where the metal could go -- as part of the global resetting of hard and fiat currency pricing.

The scary fact is that some of those analysts and forecasters of $10,000 and $100,000 appeared on the scene long ago and are extremely well-reasoned in their arguments....and were among the few to have been very early, not bashful to be seen as self-serving nutsos when, in fact, they were simply being academic.

Meanwhile, as regards my favourite global investment, India's importation of silver over the first 4 months of 2015 represents a pace that would consume a third of this year's world's mine supply (last year, I discussed India's unfolding and massive preference for the "cheaper" PM).

Previous years' and months' market reports and articles have noted the almost perfect 6-months cycle lows in silver, which goes back over a decade. The explanation for its existence is the role of managers' window dressing, as per their bonus schedules.

After having played my part in the popularization of the cycle, I forecast and identified the lows of last May and November (2014).

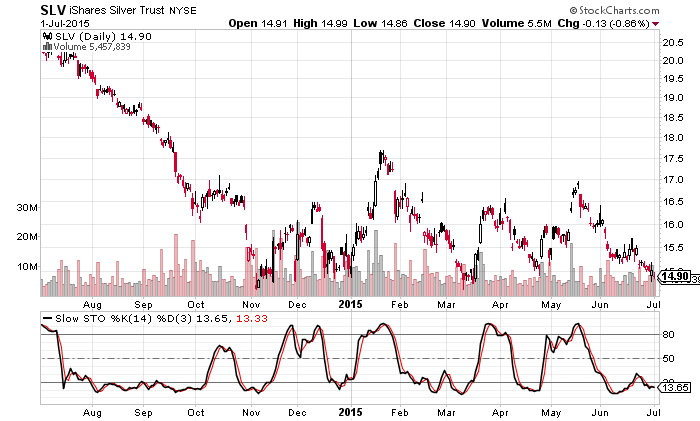

For that reason, I again felt that this low could occur in May, though, as we can see, the SLV's lowest close occurred today (July 1), though the price bottom was indeed on the last day of the month when it registered a bullish outside day reversal.

The gold chart (not shown) is not so close to its bottom, while the silver chart is reasonably near to its November low. As well, the silver volatility chart, VXSLV (not shown), troughed in August 2014 when silver made its final spike down.

At the time, I noted and do reiterate here that volatility will trend and soar with the underlying security. This is due to the fact that the marketplace has recognized that silver's future is higher.

Therefore, the premium curve must discount bull moves, not bearish activity (especially since JPMorgan's apparent "cornering" of this illiquid asset with its historic long position, provides secure underpinning for the un-invested hedge fund managers).

As well, the marketplace must determine the premium curve in light of the law of diminishing returns.

Silver is on the 15th floor of a 500-storey building (longer term, there are those who argue that $500 will still not have been the peak).

Citing the same bullish arguments concerning scarcity and commercial need, I have restricted my forecasts to $150 and $500, longer term, and then beyond to 2025.

First, a correction of price valuation to inflation-adjusted highs, before advancing to the true demand level for the metal that is made more precious by way of its usefulness, respectively.

My most successfully employed momentum indicator has always been the slow stochastic; the classically-defined divergences have been powerful supporters of the 6-month cycle.

ANY move up now confirms the buy signal (extreme right of above 1-year SLV chart above), while the below-contemplated flush-out would merely provide an unnecessary and almost cliché cyclical liftoff.

Meanwhile, a break above the downtrend channel dating back to the 2011 peak (see 10-year chart above) could engender some hairy action, with respect to which one may take the attitude of "when, not if.''

STRATEGY

If the SLV provides a flush-out under $14.70 (basis SLV), then the market would experience the most bullish event possible. Apart from the beautiful stochastic divergence (see 1-year SLV chart above), it would signal an intense desire for a major player to buy even more before a massive rally.

In such cases, a bank (for instance) "runs the stops" to create a new low, however briefly. Such events create offers above the market so as to sell into a subsequent bounce, since a new low creates a desire to sell.

However, since the sellers are essentially exhausted (before the stops were run to create the temporary new low), running the stops also creates the increased possibility of an island reversal to kick off the bull market in earnest.

In other words, after running the stops, there would be no stock left, except for the new offers that come in at higher prices as a result of the psychological effect of having seen new lows over the preceding hour, say.

Again, after flushing out silver's price by running the stops, the next available batch of offers exists above the market for the purpose of selling into a rally that would follow the flush out.

This is how "island reversals" are created.

Remember, this is not a forecast; after all, the last day of the half-year already passed yesterday (Tuesday). I write this to help investors take advantage and not get fooled. Such a flush would also be consistent with silver again bottoming after gold.

However, with the SLV's low only 20 cents away, note how EASILY a powerful bank could run the stops and exaggerate the bullish stochastic divergence with a same-day reversal to close higher.

Looking at the SLV's 10-year chart, note how 2008's break to new lows ultimately left behind disloyal bulls who would greatly regret having sold, with such regret being experienced sooner rather than later, as well.

CONCLUSION

One may employ strategies that bring together bullish views on the precious metals, with a bearish stance on equities, while favouring the 4 creditor currencies (Switzerland, Hong Kong, Norway and Singapore) at selected buy points. If deemed too complicated, one may simply have a combination of individual positions, as opposed to complex futures and options cross trades.

Having witnessed all of the major secular and cyclical turning points over the past 33 years - both at highs and lows - in U.S., Japanese and Chinese equities, currencies and, of course, the precious metals, I have concluded thus:

There has never been so lucrative an opportunity for profit, nor a need so great for hedging.

Simply, then, today's matters are comprised of extremes. Take full advantage or be victimized by them, and remember:

Whether hedging, investing or speculating, the most efficient, profitable and leveraged plays happen to be those themes which are also the most conservative.

********

LEGAL NOTICE: This market letter is the work product and intellectual property of Mr. Sidney Klein. It arises out of his training and profession as an international expert on financial equities. It is a private correspondence from Mr. Klein to his subscribers. Any person who copies or otherwise disseminates this letter becomes subject to international criminal and/or civil prosecution under the Universal Copyright Convention and the Berne Convention for the Protection of Literary and Artistic Works. Nearly all countries in the world have signed both of these Conventions and have pledged to enforce them through their own legal systems. In addition, Interpol may be called upon to assist in the international enforcement of these Conventions through its processes of arrest and extradition. If you are the recipient of a copy of this market letter, whether through the internet or by facsimile, you should immediately report to Mr. Klein the name of the person or entity who sent it to you. Send your email to sidklein@sidklein.com.

DISCLAIMER: This market letter is intended to assist in the dissemination of information to private subscribers. The information contained herein represents Mr. Klein's best efforts in good faith to advance knowledge to his clientele, but there can be no implied guarantee as to its accuracy or completeness. The information is given as of the date appearing on this market letter, and Mr. Klein assumes no obligation to update the information or advice on further developments relating to the information provided herein. No solicitation to buy or sell securities is intended, and none should be inferred. Investments are inherently risky, but investment risk itself is a function of individual preferences. Thus any opinions, recommendations, or judgments expressed in this market letter are of necessity abstract and general. They must be modified, accepted, or rejected by individual subscriber/investors whose risk averseness cannot be known to Mr. Klein.

More from Silver Phoenix 500