The Slow Grind Higher Above The Early June Stock Highs

The S&P 500 upswing extended gains, yet retreated before yesterday's closing bell. To a certain degree, the accompanying bullish signals lost their luster too. The air is getting thinner as stock prices cut into the late-Feb bearish gap. Has this been the turning point in the great bull run, or just a modest preview of more fierce battles to be fought?

I'm definitely leaning towards the latter possibility. Far from having thrown cold water on the bull run, it's a gentle test of the bulls' resolve. In today's analysis, I'll lay out quite a few good reasons why, and also discuss the signs pointing towards caution.

S&P 500 in the Short-Run

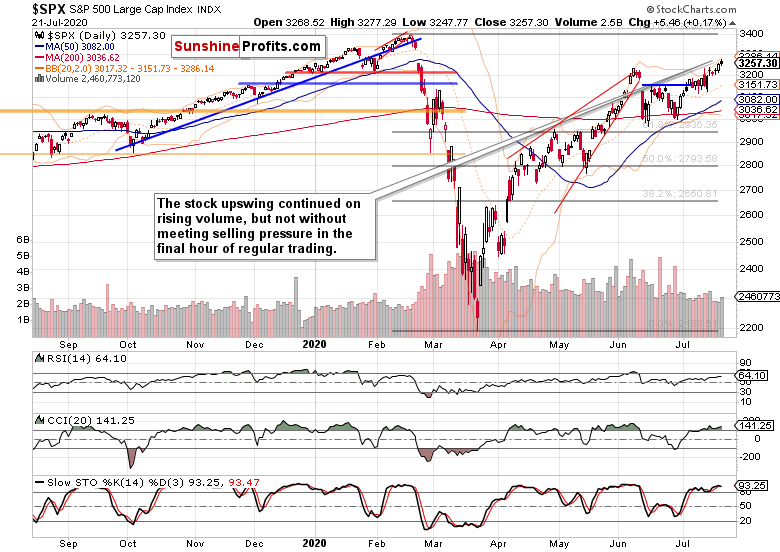

I’ll start with the daily chart perspective (charts courtesy of http://stockcharts.com ):

Stocks have peeked above the early June highs some more yesterday, and the daily volume has risen too. The candle's shape though isn't universally bullish in its interpretation, and that's because of the upper knot.

It means that the bears stepped in, and enjoyed partial success in driving prices lower. Will the selling attempt continue in the short-term? It's possible, but the volume examination doesn't attest to high chances of it to succeed lastingly.

The benefit of the doubt still remains with the bulls – and it's not only because of the credit market action.

The Credit Markets’ Point of View

High yield corporate bonds (HYG ETF) scored some more gains yesterday, but met with selling pressure before the closing bell too (this and many more charts are available at my home site). The modestly rising daily volume shows that no fierce battle has been fought so far.

Both the leading credit market ratios – the high yield corporate bonds to short-term Treasuries (HYG:SHY) and investment grade corporate bonds to longer-dated Treasuries (LQD:IEI) support each other's upswing – and that points higher for the S&P 500 as well.

On a daily basis, stocks wavered against the HYG:SHY ratio – wavered as in refused to continue outperforming to the same degree as in recent days. That's a short-term cause for concern merely though.

I consider it to be just a daily fluctuation that lacks further implications for now. The bulls have the initiative to deal with that constructively over time.

Encouragingly, the ratio of high yield corporate bonds to all corporate bonds (PHB:$DJCB) is slowly rebounding – and that points to more risk-on sentiment returning to the market place.

Spotlight on Smallcaps, Emerging Markets and the Dollar

The Russell 2000 (IWM ETF) performance yesterday is in line with the S&P 500 one – and it's as well a sign of selling pressure emerging. Both sides aren't however overly committed to action as the measured rise in volume shows. The bulls still remain in the driver's seat and can overcome yesterday's obstacle if they push just a little harder.

Emerging markets (EEM ETF) continue defending the high ground well. When I look at the below chart of the dollar, this bodes well for stock markets around the world, and also for the currently lagging ones, which are the U.S. ones.

A word of caution regarding the USDX though, as that's arguably the leading sign calling for some caution right now. While I am not calling for one, I wouldn't be too surprised if a short-term consolidation (a reflexive rebound) happened relatively shortly. The quickening pace of recent downswing as the latest long red candle shows, raises such possibility. Remember, no markets move up or down in a straight line.

S&P 500 Sectors in Focus

Technology (XLK ETF) gave up quite some of its Monday's gains, but that's not enough to qualify as a reversal. The volume examination certainly doesn't support that conclusion at the moment.

With healthcare (XLV ETF) retreating from its new 2020 intraday highs yesterday, it was the financials (XLF ETF) that assumed the leadership among the sectoral heavyweights. This would be consisent with the unfolding rotation into undervalued plays after Monday's tech return to shine.

Consumer discretionaries' (XLY ETF) or materials (XLB ETF) didn't see strong moves on a closing basis yesterday, leaving the industrials (XLI ETF) and especially energy (XLE ETF) as the more eye-catching choices. With energy helped by the daily upswing in oil prices on relenting new lockdowns speculation, it leaves us with a tepid but still unfolding rotation into former laggards intact.

And as such rotations mark the health of bull markets, the takeaway is an optimistic one for the current run higher.

Summary

Summing up, the S&P 500 retreat into yesterday's closing bell doesn't appear to be a game changer, making the case for a daily consolidation likely. Not even the U.S. – China tremors have a disproportionate impact on the 500-strong index these days, playing second fiddle to stimulus and vaccine expectations. The summer doldrums' initiative remains with the bulls as the improving daily market breadth shows. Despite the uptick in put/call ratio, greed is making a steady but slow return into the market place, which calls for cautious approach to risk management. I would say that seeking short-term mispricing in order to capitalize on such temporary imbalances is the preferred course of action. In doing so, let's keep in mind that the trend remains up – the slow grind higher rules these days.

Thank you for reading today’s free analysis. I encourage you to sign up for our daily newsletter - it's absolutely free and if you don't like it, you can unsubscribe with just 2 clicks. If you sign up today, you'll also get 7 days of free access to the premium daily Stock Trading Alerts as well as our other Alerts. Sign up for the free newsletter today!

Monica Kingsley

Stock Trading Strategist

Sunshine Profits: Analysis. Care. Profits.

* * * * *

All essays, research and information found above represent analyses and opinions of Monica Kingsley and Sunshine Profits' associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Monica Kingsley and her associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Ms. Kingsley is not a Registered Securities Advisor. By reading Monica Kingsley’s reports you fully agree that she will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Monica Kingsley, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

*********

Monica Kingsley is a trader and financial markets analyst. Checking dozens of charts daily, she integrates their messages with economics and in-depth experience. Trade calls and writing are her cup of tea as much as studies in market histories. Having been at the financial markets when the Great Recession arrived, she experienced many bull and bear markets - be it in stocks, bonds, gold and silver. https://www.monicakingsley.co