Stormy Weather Dead Ahead

Anyone familiar with navigating the Great Lakes by either sail or by piston knows the value of a barometer and by default the peril of failing to heed one. The word itself is well-known to market historians through phrases like “the stock market is a barometer, not a thermometer” referring to the ability of falling stock prices to many times lead the economy into recession. However, since the market crash of October 1987, that predictive ability has been largely nullified by interventions and interference in virtually all markets in actions made commonplace by the Central Banking fraternity around the globe. Their abusive domination of the credit printing press has made the Generally-Accepted Accounting Policies (“GAAP”) just about as important in regulatory governance as the buggy whip in controlling the inertia of an automobile.

However, barometers remain useful tools in weather forecasting because of their innate ability to detect sudden changes in atmospheric (barometric) pressure which occurs as a low or high pressure zone arrives to displace the other. Known as “fronts”, these large masses of differing air pressure systems carry with them unsettled weather and where there occurs a faster and larger than expected drop in the barometer, the bigger and more intense the pending storm.

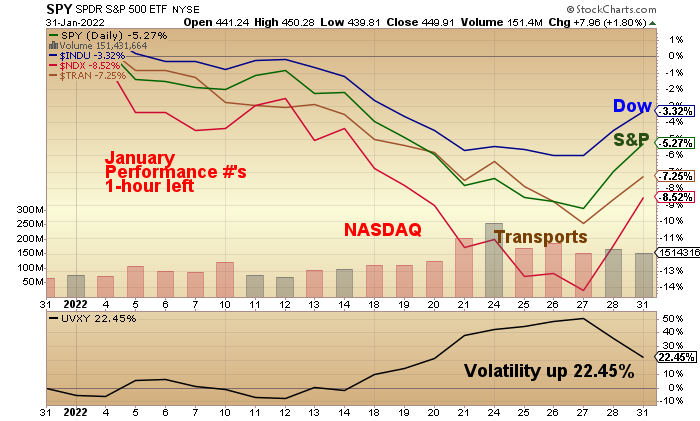

As I have been highlighting for the past thirty days, the January Barometer has finally (but not surprisingly) registered a sell signal for the year with the “First Five Days”, an early-warning indicator, followed by the “Mid-Month Indicator” both turning negative despite a sharp rally in stocks over the final five sessions. To be sure, sentiment has shifted quickly to the downside and bottom-callers are now springing up out of the bodybags to tell us that “The Fed is trapped!!!!!” and that this rally is foreboding a Fed “pivot” that will allow the 2009-2022 bull market to resume because, after all, even at the lows of a week ago, we were barely in “correction” territory (> -10% from the highs). I, for one, beg to differ.

In boating, the biggest mistake you can make is when you see nothing but blue sky ahead and nary a cloud in the sky as your barometer starts to plunge. The sun is beaming down and the water is flat and everyone is up on the bow with suntan oils and radios blasting and there is absolutely zero warning that there is anything out there that could spell “trouble” – except of course, the barometer.

In my early years boating, that exact scenario unfolded but luckily, I had an experienced boater as a companion in the next vessel and as the jocularity of the day threatened to turn into boater debauchery, he told me to go to a vacant VHS channel after which he instructed me to follow him into a little-known cove where we rafted off and then tied onto shore as the winds went dead and the sounds of the birds and insects went very, very quiet. With the barometer scraping along at seven o’clock, it took less than twenty minutes for the clouds to roll in, the winds to move to gale force, and the seven other boats exposed to the elements to go screaming for shelter.

Just as Richard Russell would tell me that in a bear market, “he who loses least is the victor”, in a Great Lakes storm, “he who suffers least damage to their vessel is the victor” with the point of commonality being – you guessed it – the barometer. We suffered minor damage that afternoon but the point remains that we had both forewarning and shelter and still got hurt. Such is the case in all bear markets – maximal protection, minimal damage – that is my goal in 2022.

This past month has the January Barometer registering a definitive “sell” but as my great friend, market historian and technical analyst David Chapman points out, it has been impressive since 1950 but only 60% accurate since 2000 – and that is important. I would argue with Chappie (as we old guys can do with great gusto and then have a beer and talk hockey as opposed to going on social media to continue the battle) that the Fed since 2000 has adhered to the theory that the “asymmetrical wealth effect” can drive Mandate #1 (“Maximum Full Employment”), that those rising stock prices validated their tactics, as stock market profits would fuel jobs. Well, they got the jobs but with it, a direct confrontation of Mandate #2 (“Price Stability”) and now that they have ceremoniously announced their intention to focus on #2, how can stocks survive a Fed policy shift?

If it was the asymmetrical wealth effect of rising stock prices that fueled employment, I contend that it was also the magic “bid” provided by the Fed that kept stocks levitated all through the DotCom crash and the GFC and during the COVID crash all in the name of “maximum full employment”. Now, that policy mandate and that “bid”, by default, has evaporated.

Which brings me to my “Trade of the Year 2022”…

In the era of rising credit demand and demographic growth that is normally associated with the post-war era commonly assailed as the “BabyBoomers”, the “Silent Generation” that fought and won WWII and then came home to the rewards associated with victory which included – well – sex. Sex coupled with marriage resulted in a population boom beyond anything that the world up to then had seen and as a product of that generation, I can tell you that, looking back, we Boomers were SOOOOO lucky.

However, I digress.

Some of you will recall the week in April 2020, when oil futures traders got caught “offside” on the long side resulting in spot crude futures going out at minus USD $38 per barrel – a negative number for crude oil delivery – which meant that both storage and usage were absent. That was a complete function of the financialization of markets and had no bearing whatsoever where you or I could actually buy FOR DELIVERY a carload of crude oil. If you were trying to “game” the refineries, you could do it but at the end of the day, a barrel of crude for immediate delivery was around USD $20/bbl. while a barrel of crude with no intention of delivery penalized the speculator and rewarded the end-user. This mechanism, sans central bank shenanigans, is a wonderful method of delivering true price discovery for all things produced and traded en masse.

Crude oil prices are a true “price discovery” domain to the Saudis and the Russians as they are increasingly-dominant in the world crude market. They care not about the input costs to Western economies. They care only about revenues to sheiks and oligarchs controlled by chess-masters like Vlad the Outfoxer. We are now led to believe that the oligarchs that control Western banking have determined that now and only now is inflation a problem. Now that they have seen ten-twenty-fold increases in their net worth comprised primarily of assets used as collateral for the member banks (real estate and paper assets like corporate bonds and stocks), and now that they have been suitably forewarned of a shift in policy, the new narrative is to have the financial news networks shift from “all-time highs” (in stocks) to the Consumer Price Index as a means of mollifying the masses into a sedated financial stupor.

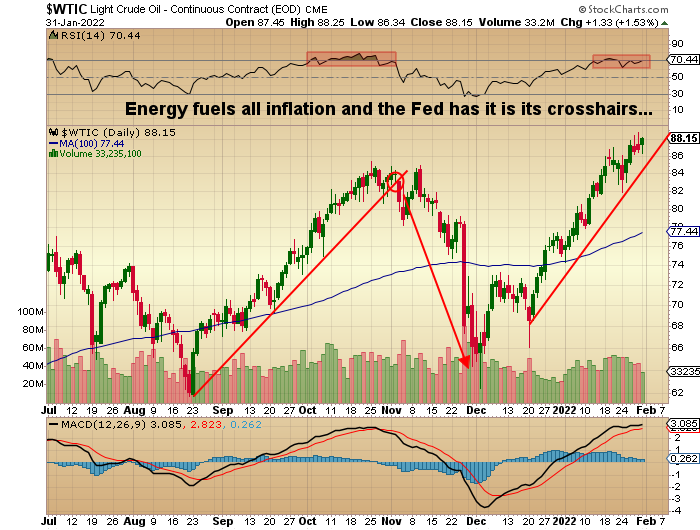

The problem remains that if you want to crush inflation, you cannot have energy prices scraping along the ceiling of fifteen-year highs because virtually everything that gets produced must be lifted, manufactured, transported or flown to an ultimate end-buyer and the more it costs to deliver the finished goods to the end-buyer, the greater the cost of production and the accompanying CPI/PPI accelerator.

My number one trade for the first quarter and quite possibly 2022 is to fade the move in crude oil. From the technical perspective, it is overbought and over-owned. From the narrative perspective, everyone has ten reason why it is going to USD $150-200/bbd. but no one has a clue what happens to input costs and P/E multiples if and when that happens. Lastly, it is the sovereign and mortal enemy of the not only the Fed, but it is also the number one enemy of the U.S. military because it at once both empowers and enriches Vladmir Putin and his roving gang of oligarch henchmen.

If the true mandate of the global bankers has actually shifted from “maximum full employment” to “price stability”, they must and will shut down this bull move in crude oil and natural gas. By doing so, they move to achieve both domestic monetary and foreign policy objectives pertaining to both inflation and Russia.

As a sexagenarian with a great many stories to tell and scars to reveal, all you have to do in this type of market environment is survive. The days of bragging at the eighth tee block as the tour bus golfers from Taiwan search for their balls in the woods are over. The days of holding court at the Chamber of Commerce luncheon and tripping the light fantastic about your surge in net worth due to a timely excursion into cryptocurrencies should be replaced with quiet reflection with family about “safety of principal” and “no-risk yield”. That said, if you must play in the equities sandbox, gold and silver mining stocks right down the ladder from boring senior producers to wild-eyed Yukon explorers represent terrific value right now. (I should add IF there is such a thing as “value”.)

Since we are all major-league holders of gold and silver equities, a mistake shorting oil will be offset by a sharp upside reaction in the metals. Call it a hedge; call it a trade. I am betting on the Fed.

That has been a high-probability trade since 1979…

Disclaimer

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

*********