The US Dollar Is Sinking

share

share

share

share

share

share

share

share

share

share

The rally in the value of the US dollar that had kicked off in February 2018 after the sell-off since December 2016 ran out of steam at 102.82 on March 20 – purely by chance, of course, this was the same day the DJIA had bottomed just before Wall Street started its miraculous 48% levitation on Monday 23 March. The dollar held close to 100 until the end of May, then fell further to end at a new intermediate low at 93.32 on Friday. Is the weaker dollar the primary driver of the gold price?

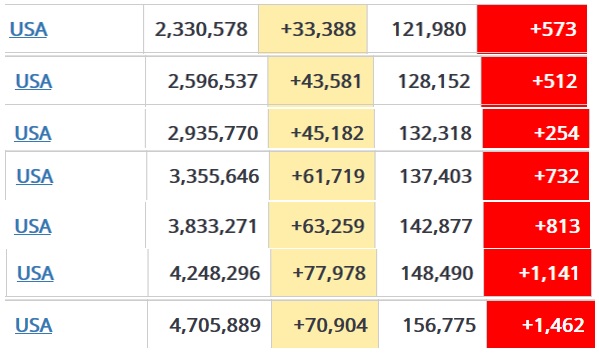

The weekly statistics on COVID USA below show a disturbing trend with both the number of cases and of new deaths on the increase during the past five weeks. The number of daily deaths a month ago was lower, breaking the trend, but then made up for it later. These increases contribute to global totals of more than 18 million cases, more than 6 million still active cases and almost 690 000 deaths.

The numbers for the last week are from Friday. The trend to have lower numbers on weekends continue and the Friday number appears more in line with the trend for the week. If one were a conspiracy theorist, there is much scope to speculate about the reasons(s) for lower weekend numbers in the weekly pattern. A macabre explanation would be that hospital staff make sure that dicey patients do not make it into the weekend when a smaller number of essential staff is on duty!

Luckily we are not conspiracy theorists, because we make certain that all the facts speak for themselves. As the saying goes, “You are not paranoid if THEY really are out to get you!”, as we know all too well what happened during the past 20 years.

The decline in the value of the dollar largely overlaps the recent months of bullish behaviour by the precious metals since the end of May. While few people will argue that there is no cause-effect relationship between the value of the dollar and rising metal prices, the important question is whether this relationship means that signs of increasing scarcity of gold and silver and general fear about the future state of the economy are not also driving prices of the metals higher.

There are at least two ways of answering that question. The first is to look at the relative changes in the dollar and in the prices of the metals since late in May this year. The dollar declined by 7.1% from a high of 100.47 in mid-May to Friday’s close at 93.321. The price of gold improved during about the same period from near $1683, where it had spent longer than a month, to $1965 – an increase of 16.8%. The price of silver, the laggard, improved from $17.34 late in May to end at $24.07 on Friday, for a gain of 38.8%.

Both metal prices by far outperformed the loss of value by the dollar. Unless there is significant gearing in the dollar-price of metal relationship in favour of both the metals, the metal prices had other drivers that carried their prices higher. It is clear that the term ’laggard’ ought not to be applied to silver anymore; it is trying really hard to catch up to gold – and with gold already at new all time highs, silver has a long, long way to go to equal gold’s performance.

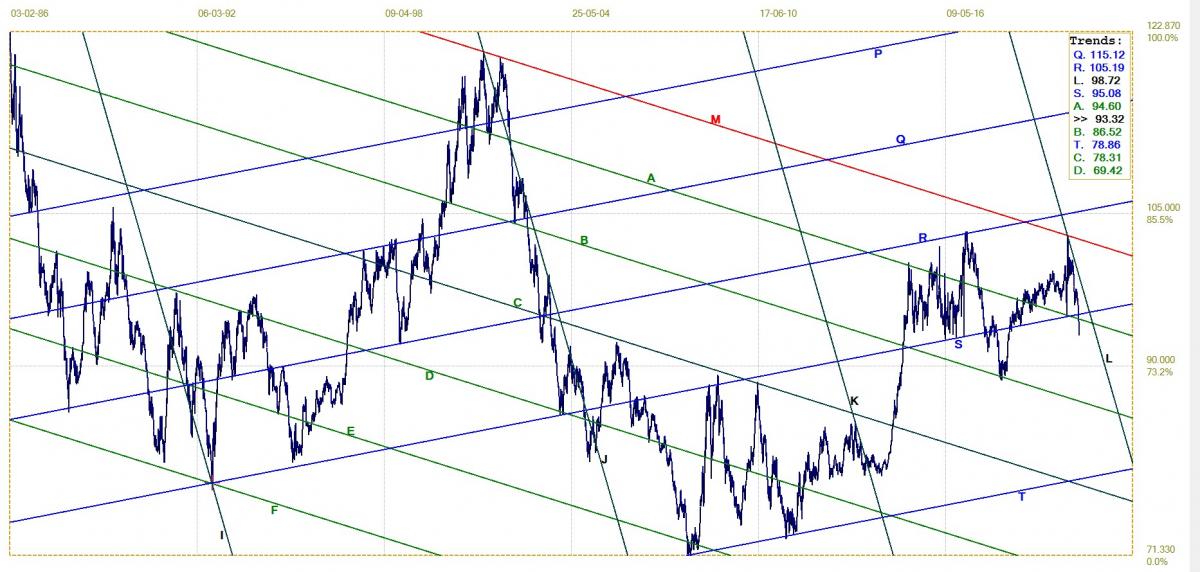

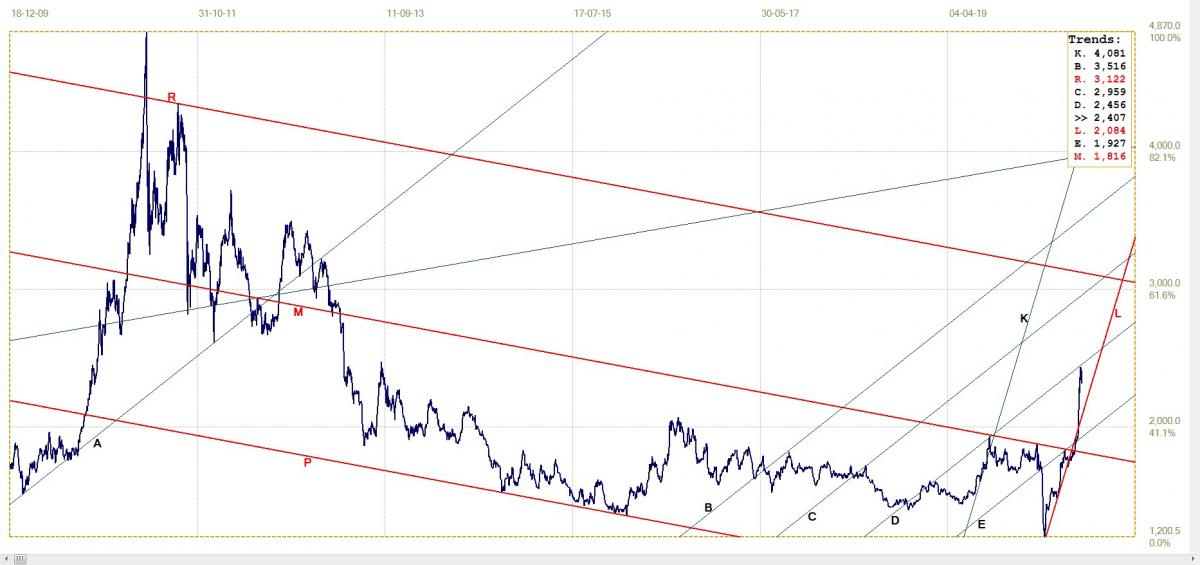

The chart below of the full history of the daily close of the dollar index (DXY) shows some quite amazing channel formations. All the trend lines are located so that they pass close to significant trend reversals. Channels FE, ED and DC all have the same width to within a fraction of 1%. The same applies to channels CB, BA and AM as well as to channels PQ, QR and RS. Accurate equal spacing of so many channels on one chart is a rarity, in particular because the one channel pair that stands out as not fitting the pattern is channel RST with a channel ratio of 384:616, which is close to the 382:618 of the Fibonacci ratio.

The analysis presents two channel sets with different gradients of opposite sign, to form a grid that is similar to the well known Gann analysis. Except that here the gradients of the trend lines all have been derived from the master gradient, M. Only the locations where they are placed are optional their gradients are pre-determined by the master gradient’s unique definition tangent to the top spikes.

While another trend line can be added between lines S and T to be possible support for the euro, the accurate ratio of channel RST implies that, should the structure of the chart be maintained, the dollar is likely to test one of trend lines B (86.52) or T (78.86) in due course. That would take the dollar lower from the close on Friday by another 7.3% or 15.5%, depending on which line is to act as support.

If the decline extends to test support at line C (78.31), the existing bullish pattern of channels will be broken to warn of further weakness to come. Line D (69.42) will become the next level of support, with further downside within the bearish pattern of channels if line D does not hold.

Dollar Index (DXY) Daily close. Last = 93.321

Technically, therefore, the overall pattern of behaviour of the dollar index since its inception in 1986 makes provision for the large decline in the value of the currency if the anticipated hyperinflation, in certain quarters at least, is realised.

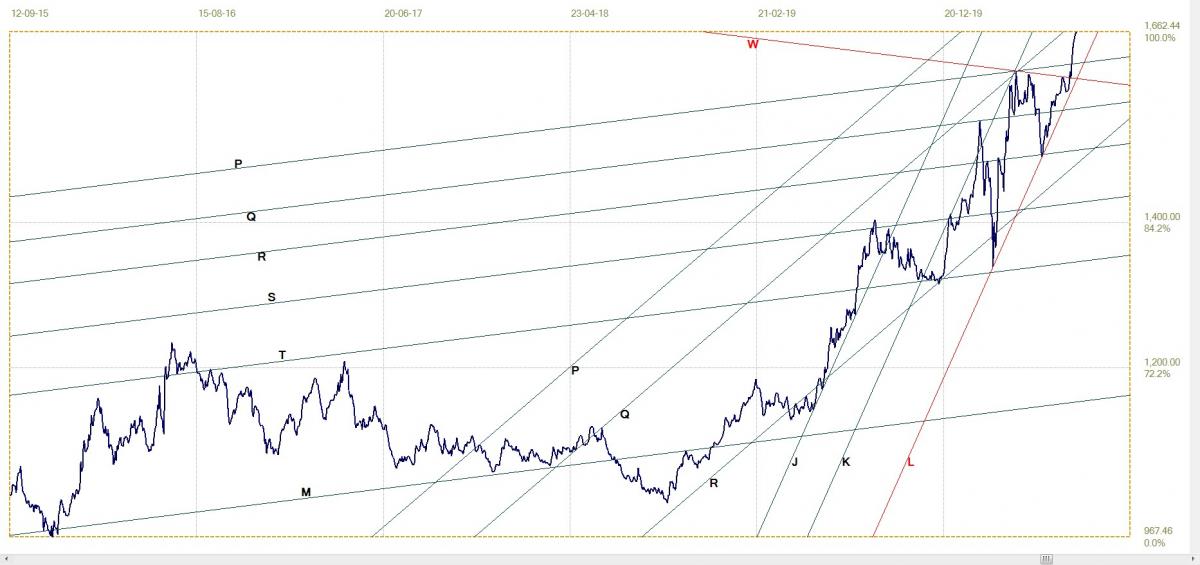

The euro and the prices of gold are affected in rather similar fashion by changes in the value of the US dollar. This relationship affords the means for an estimate of the inherent strength of the gold price. Since late May the euro has changed from $1.09 to $1.1776 for a gain of 8%, not too different from what the dollar has lost. The price of gold in euro over the same time frame went from €1490 to €1662 for a gain of 11.5%. This makes it clear gold has experienced intrinsic growth since May, even if dollar softness is responsible for much of the rally in the price of gold. The implication is that the scarcity of the metals has not yet sparked full buyer interest.

The NASDAQ closed not far below its all time high on Friday. So far, charts shown last week still indicate an accurate long term high in this index.

The yield on the US 10-year Treasury note has reached a new low at 0.533%. while the price of crude moved mostly sideways to break through technical support as a signal that lower demand is expected as the economy suffers.

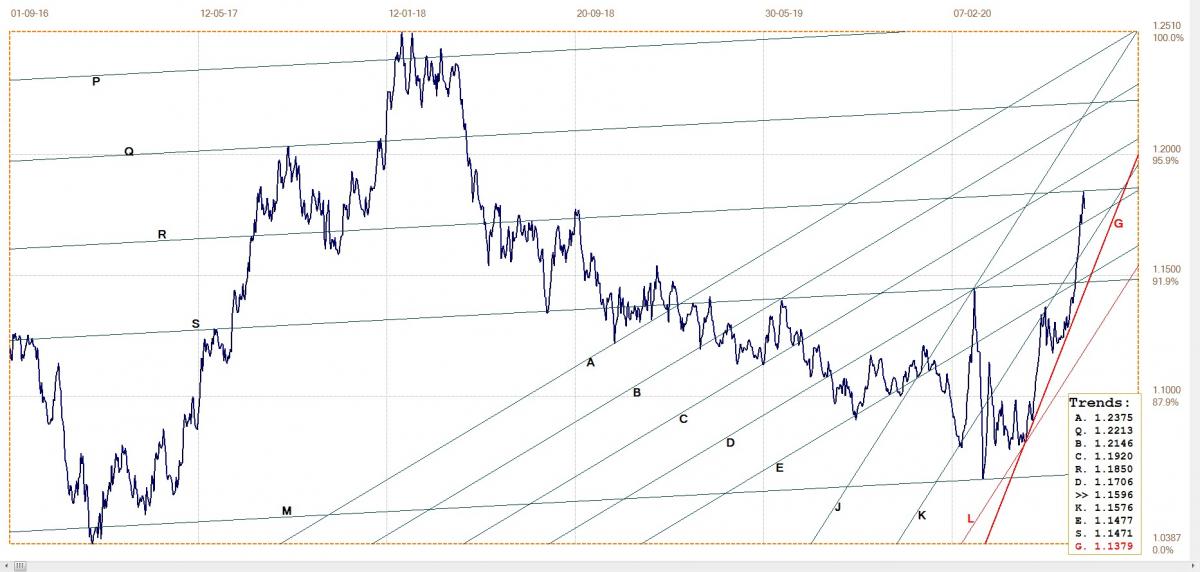

Euro–Dollar

A stronger euro is a primary cause of the decline in the dollar index. The rally off a recent low held in bull channel JKL and also above steeper trend line G ($1.1379). The euro held closely to the steeply rising wedge KG – a chart pattern that more often than not completes five legs to be followed by a reversal out of the wedge. Here, as happens less often, the price broke out of the wedge at the end of leg 4 to extend the trend steeply higher.

After two previous failed attempts to break above line S ($1.1471), this time the euro broke cleanly higher, but then only as far as the next line in the set PQRS. The reversal off line R ($1.1850) is well clear of the primary steep support along line G and it would not surprise of the euro now spent some time while consolidating.

Euro–dollar, last = $1.1776 (www.investing.com)

DJIA Daily close

Wall Street has sustained it’s amazing feat of levitation beyond what even the most pessimistic Bear could have foreseen, but it is starting to look as if the realities of the economy is starting to make inroads on the powers that be behind the levitation – be they normal market forces (or would ‘abnormal market forces; be better?) or intervention from official quarters – so that support is no longer as persistent.

The fact that daily volumes recently dropped mostly below the 3-months average of 442 million Dow 30 shares per day, shows that short sellers and any investors who have decided to take profit and seek out the sidelines are not yet eager to act. All except really die-hard bears have caught the momentum bug during the past four months and its effects are still lingering. There must be a significant shock of some kind to shake the last bullish sentiment out the market. Will really terrible financial results, much worse than expected, perhaps do the job?

DJIA, last = 26428.32 (money.cnn.com)

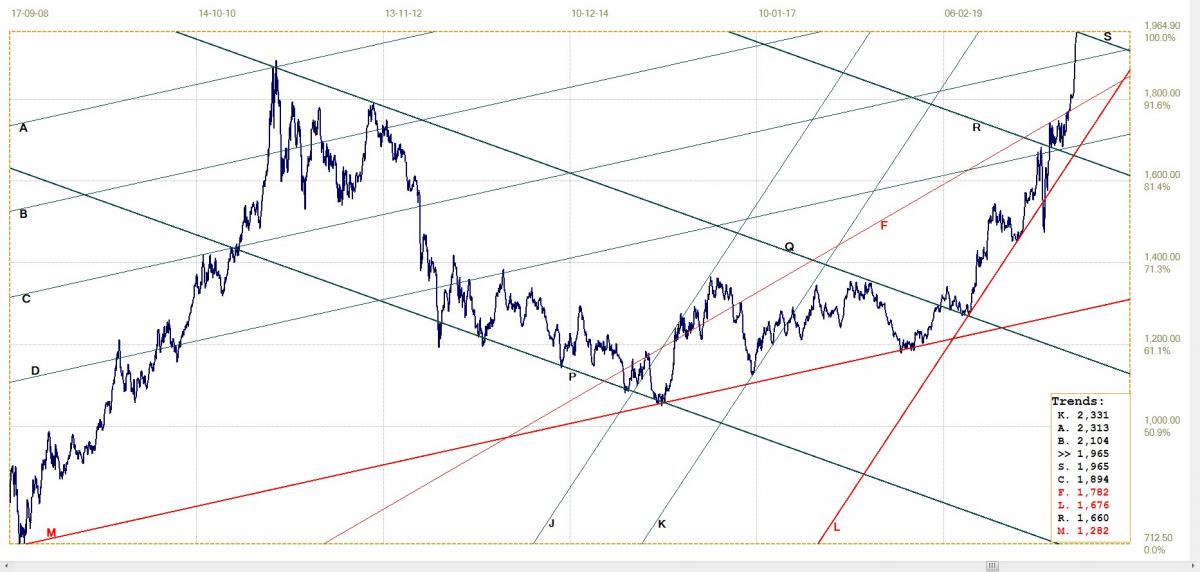

Gold London PM fix – Dollars

The price of gold in terms of the London PM fix shook off its lethargy for a while, but then spent much of last week trying to sustain the momentum. This fell short of what was hoped for a week ago. The reason for this slow-down was, of course as at the end of each and every month, the effect of Comex shenanigans on the market.

The steep run up in metal prices also boosted the open interest, which meant that, as expiration dates approached, the Big banks faced significant losses. As always, their solution was to suppress prices on critical days. In this they were assisted by speculators – who have so often seen good profits vapourise when prices suddenly plummet – who had decided to rather take profit and smile to trade another day.

Gold nevertheless ended on a high nor last week, with Friday’s PM fix right at line S ($1965) and the day close later a few dollars higher.

The channel ratios of channels PQR and QRS are close to 500:500 and 382:618 – important ratios of channels that are strong, respectively evenly divided and in the Fibonacci ratio. This too might mean that, like the euro, the price of gold price could see a period of consolidation. The ratios also implies that a sustained break higher should be viewed as a significant event to confirm the bull markets.

Gold price – London PM fix, last = $1965,90 (www.kitco.com )

Euro–gold PM fix

Euro gold price – PM fix in Euro, last = €1661.72 (www.kitco.com)

The skew triple top clean at line W (€1598.7) and into channel AB (€1634) is proof that the dollar price of gold is doing much better than simply riding higher on the back of a weaker dollar, as discussed earlier. The price has held well in the steep bull channel KL (€1568) and the bull trend is intact while line L holds.

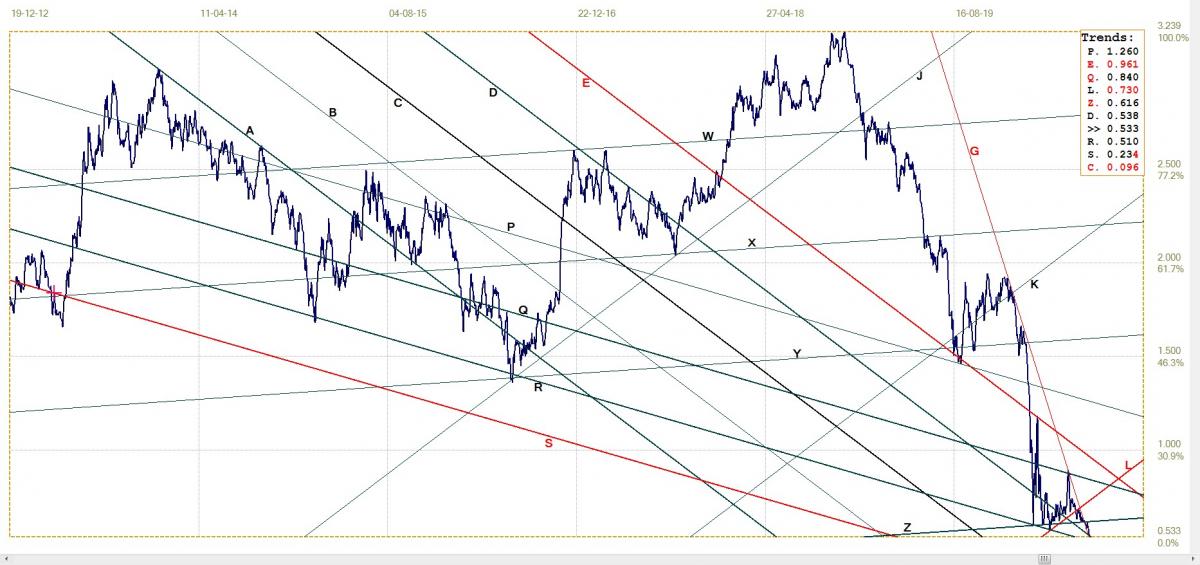

Silver Daily London Fix

Silver daily London fix, last = $24.07 (www.kitco.com)

The chart clearly shows the sad story of silver post 2011. The price plummeted from the high London fix at $47.7 in April 2011 is stages until it settle in bear channel PM where it remained from April 2013 – when the gold price was hit for $200 in one day! until it was “fourth time lucky”, to a break above line M again in early July after longer than 7 years in the doldrums.

Now if we could get a repeat of the 2010-2011 bull market when the price of silver took off from $10.80 in August 2010 and reached $48.70 eight months later in April 2011 – but failed to hold. In principle, though, this should be quite possible. At the moment the fundamentals for silver are much better than 20 years ago, with supply under pressure and greater manufacturing demand for the metal while the dollar is 24/7 shifts at the printing works.

To achieve this performance will require more acceleration; the price must increase at a steeper rate than that of channel KL – as it had started to do since the break above channel PM. The higher rate of increase will then have to be kept up for at least the next few months. Which is not impossible at all given what is known of the fundamentals! And if Wall Street should go into a decline . . .

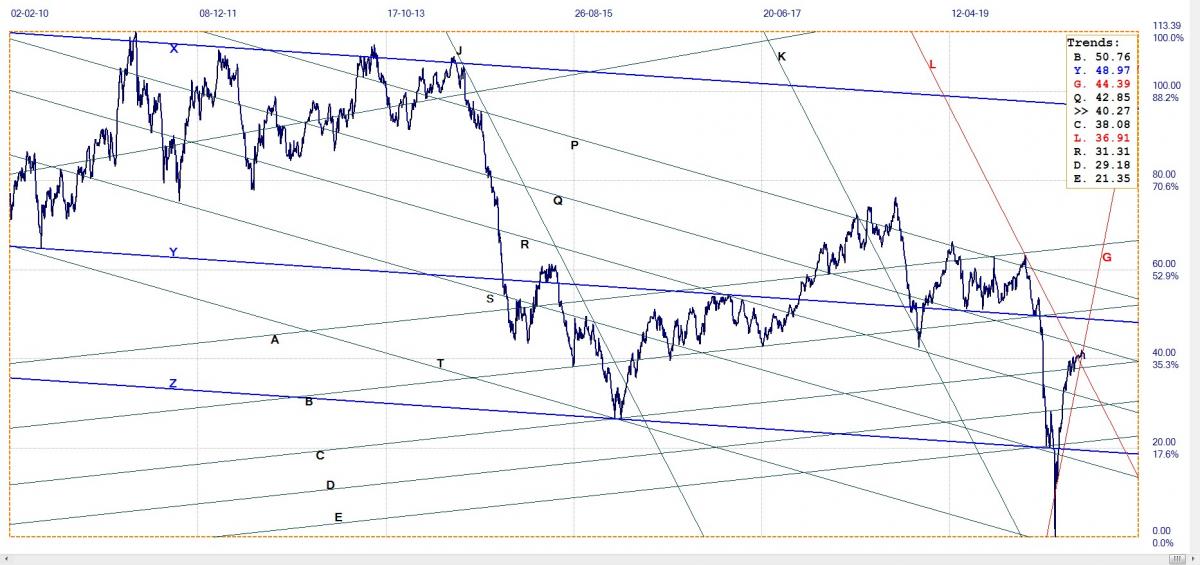

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 0.533% (www.investing.com )

The yield on the US 10-year treasury note ended last week at a new low value. It held above line Z (0.616%) of the strong channel WXYZ and line L (0.730%) of the other strong channel JKL for some time which helped to keep the yield above the key 0.6% level. When it failed to hold in channel KL it easily broke below channel YZ as well to slip lower along line D (0.538%). The yield may now even be in the early process of breaking well below this steep trend line.

Unless the fundamentals change soon, which technically does not seem likely after the yield had failed to hold above lines L and Z, a challenge on line R should happen quite soon, even if line D should hold. The yield has a big mountain to climb before it can go negative, but the prospect for still lower yields looks good at the moment.

West Texas Intermediate crude. Daily close

After managing to break above steep bear channel KL (23.91) as a display of new strength, the price of crude tried so hard to repeat the achievement by holding to the support of steep line G ($44.9). It managed to hold for 2-3 days, but by then the price had moved too far above the $40 mark which had clearly become a level of significant resistance. The race higher to $40 was with long steps, buit as soon as the price had broken higher it became a struggle to creep higher with small steps.

On evidence of the break below line G it now looks technically as if the price will slip lower again, probably to below line C ($38.08). That would fit the fundamentals of the moment, with more indications that there will not be a V- shaped recovery.

WTI crude – Daily close, last = $40.27 (www.investing.com )

*********

share

share

share

share

share

More from Silver Phoenix 500