Why 1% Interest Rate Hikes Won't Fix + 6% Inflation

The US Federal Reserve announced this week what many market participants were expecting — a series of interest rate hikes starting next year.

On Wednesday a majority of the Federal Open Market Committee (FOMC) forecasted three quarter-point rate increases in 2022, a tightening of monetary policy after holding borrowing costs near 0% since March 2020.

The new projections would see interest rates rise to 0.75% by the end of next year, with another three increases slated for 2023 and two more in 2024, bringing the federal funds rate to 2.1% by the end of that year.

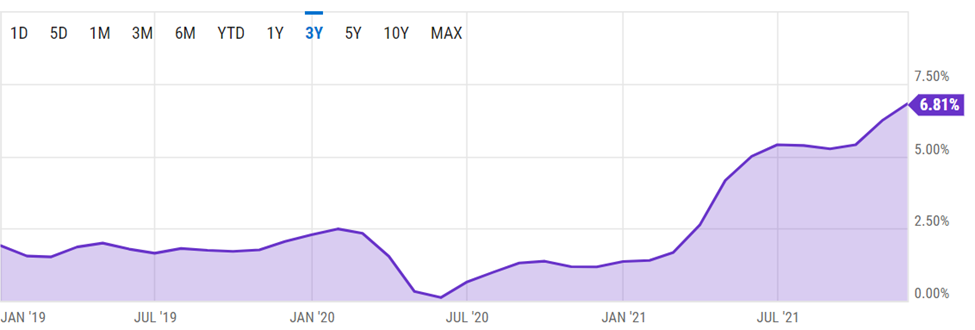

The Fed is reacting to higher-than-expected inflation which officials previously argued would fade as supply chain pressures owing to covid-19 eased. Instead inflation has soared, with the US Consumer Price Index reaching a 30-year high of 6.8% in November fanned by a continuation of the pandemic, supply chain bottlenecks and strong demand for goods and services amid unprecedented fiscal and monetary policy support.

US Consumer Price Index YoY, Y Charts

The pace of the rise suggests the US Federal Reserve is well behind the curve in controlling price increases, led by “the essentials” of food, transportation and shelter.

Energy costs recorded the biggest gain, 33%, including a 58% increase in gasoline and a 25% increase in natural gas; shelter costs rose 3.8%, the most since 2007; and food prices vaulted 6.1%, the highest since October, 2008 (the CPI for meat rose 16% year over year).

Food inflation. Source: Trading Economics

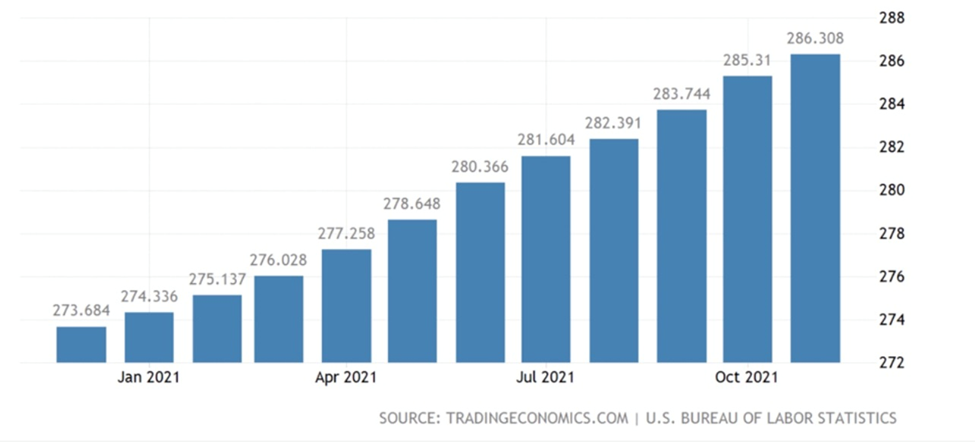

CPI housing utilities. Source: Trading Economics

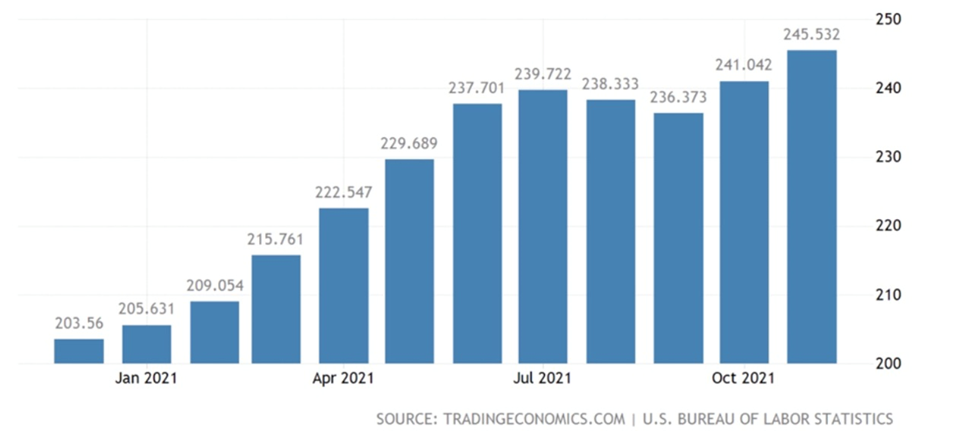

CPI transportation. Source: Trading Economics

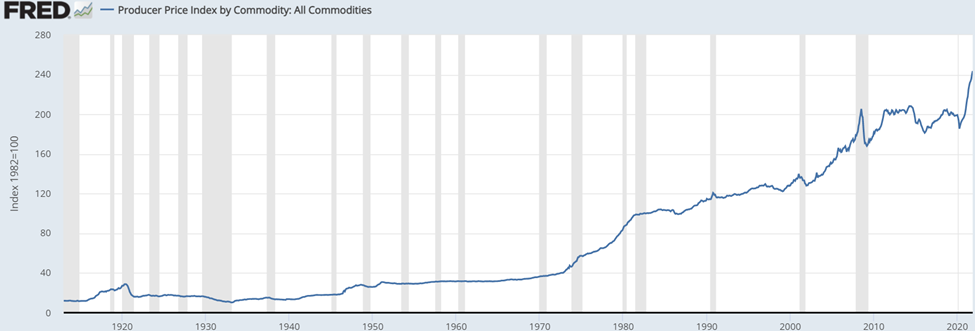

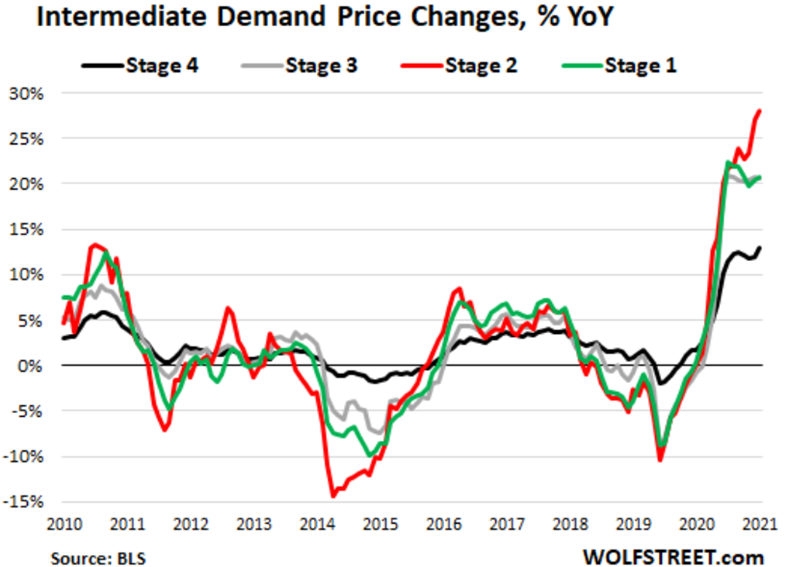

The producer price index in November climbed 9.6% from a year earlier, the largest in figures going back to 2010, and well above October’s 8.6%.

Further up the producer price pipeline, inflation is raging at 28%, notes Wolf Street.

Excluding food and energy, the inflation metric known as core CPI went up 4.9% compared to 4.6% in October, the highest since June, 1991.

It’s important to note, the Federal Reserve doesn’t count food and fuel in its regular inflation forecasts, preferring the “PCE inflation” metric. As the name suggests, the Personal Consumption Expenditures price index measures changes in the prices of consumer goods and services. Thus the Fed is deliberately understating the real inflation rate (how they can exclude food and gas prices is beyond comprehension) which have actually increased about 10% year over year and are heading higher.

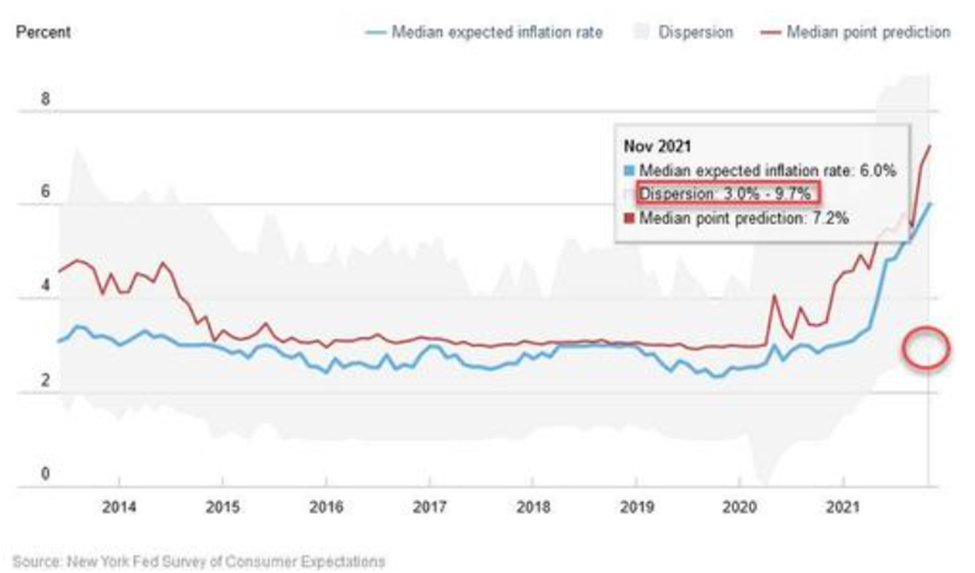

The New York Federal Reserve’s November survey of consumer inflation expectations hit a new all-time high of 6%, up from 5.6% in October, with at least a quarter of survey respondents seeing inflation surging to double digits.

Zero Hedge reports consumers now expect most expenditures to rise by around 10% in the coming year, with gasoline prices expected to go up 9.1%; food prices to increase 9.2%; medical costs to climb 9.6%, rent to rise 10%; and the cost of a college education expected to surge 9.1%, the highest since 2015.

This is a far cry from the central bank’s PCE inflation estimate for 2022 of 2.6%.

The Fed’s governing body also said it will double the pace at which it is scaling back its monthly purchases of Treasuries and mortgage-backed securities (the so-called “taper”) to US$30 billion a month, meaning the quantitative easing program will end in early 2022 rather than mid-year as previously planned.

In our last article we argued the taper will not quell rising prices, and in this article we will attempt to show that modest interest rate adjustments of less than 1% will have little to no effect on skyrocketing inflation.

The Federal Reserve is severely constrained in how much it can raise interest rates, due to ballooning debt. The national debt is now over $29 trillion, and heading higher, much higher. The Fed can telegraph its intentions all it wants, the fact remains that at such unsustainably high debt levels, the interest payments will eventually cripple the federal government.

According to the Committee for a Responsible Federal Budget, each 1% rise in the interest rate would increase FY 2021 interest spending by roughly $225 billion at today’s debt levels. On a per-household basis, a 1% interest rate hike would increase interest costs by $1,805, to $4,210.

For round numbers, let’s just say a 0.75% interest rate hike would increase the interest costs per household by $1,400.

The latter will hit the consumer right in the pocketbook, as will higher interest rates on mortgages, car loans and credit cards, which will all go up following the rise in the federal funds rate.

Corporations will also feel the squeeze. The interest on their loans will increase, forcing them to hike prices. Again the consumer pays. In the worst cases, companies will lay off staff, hurting workers and pushing the most vulnerable into severe economic hardship.

Food

Does the Fed really think that raising interest rates by <1% is going to stop food inflation? Skyrocketing prices of everything from meat and eggs to dairy and pasta, both in Canada and the United States, is only partially due to supply chain disruptions.

Food inflation is also being driven by record-high fertilizer prices and climate change.

Higher input prices are usually passed onto the buyer of meat, fruits and vegetables, for the rancher/ grower to preserve his profit margin. In November the Green Markets North American Fertilizer Index hit a record high, rising 4.4% to US$1,094 per ton, surpassing the previous week’s record and its 2008 peak.

According to BNN Bloomberg, the fertilizer market has been pummeled this year due to extreme weather, plant shutdowns and rising energy costs — in particular natural gas, the main feedstock for nitrogen fertilizer.

Modern farming simply cannot do without fertilizer; its higher cost must be borne by producers and so higher food prices are likely going to be “baked in” for several years. Everyone from ranchers to farmers, greenhouse growers and orchardists will be affected.

As for climate change, we know that higher temperatures lower crop production, droughts like we experienced this past summer ruin crops and cause feed prices to soar, leaving ranchers no choice but to cull their herds. The prices of staple crops like corn, wheat and soybeans have all tracked higher.

Desertification, a process whereby land in arid or semi-dry areas becomes degraded is a global issue with more than half of Earth’s arable land affected. Currently 12 million hectares of arable land is lost to drought and desertification annually. The issue is said to affect 1.5 billion people in over 100 countries.

Desertification is made much worse by climate change.

Ranching and farming, through extensive energy inputs like diesel fuel, lights, heating, etc., generate high amounts of carbon dioxide. Farming also releases methane from cows and cow manure, and nitrous oxide from fertilizers. Both are heat-trapping greenhouse gases.

We can’t forget fish and shellfish. As the ocean warms it causes acidification, which stunts the growth of corals. The destruction of coral reefs is a major problem, since they provide critical habitat and food for so many species in the reef ecosystem. If current rates of temperature rise continue, the ocean will become too warm for coral reefs by 2050.

World fisheries are in a state of collapse — caught between plagues of jellyfish, overfishing, nutrient pollution, bioaccumulation of toxics in marine mammals, carbon emissions turning our oceans acidic, the oceans’ phytoplankton declining by about 40% over the past century, dead zones, garbage patches, increasing ocean temperatures and changing currents — our entire marine food chain seems to be in peril.

We at AOTH know that climate change is not going to stop, the Earth is going to warm until it starts to cool, as it has done in natural cycles for millions of years. As long as it does, food prices across the board are practically guaranteed to rise.

Grocery shoppers are also being hit with shrinkflation, whose effects are mostly borne by the poor and working poor.

According to The National Post shrinkflation is paying the same amount for a product, say a box of cereal, but getting less. Manufacturers do this to offset increasing input costs without increasing prices. A 2014 study published in the Journal of Retailing reported consumers are four times as sensitive to price differences as they are to changes in package size. Though consumers often express frustration when they notice downsized products these negative reactions are typically short-term. When manufacturers surprise people with higher price tags, however, they tend to lose market share: “There’s less of a risk to shrinkflation than to increase prices.”

Shelter

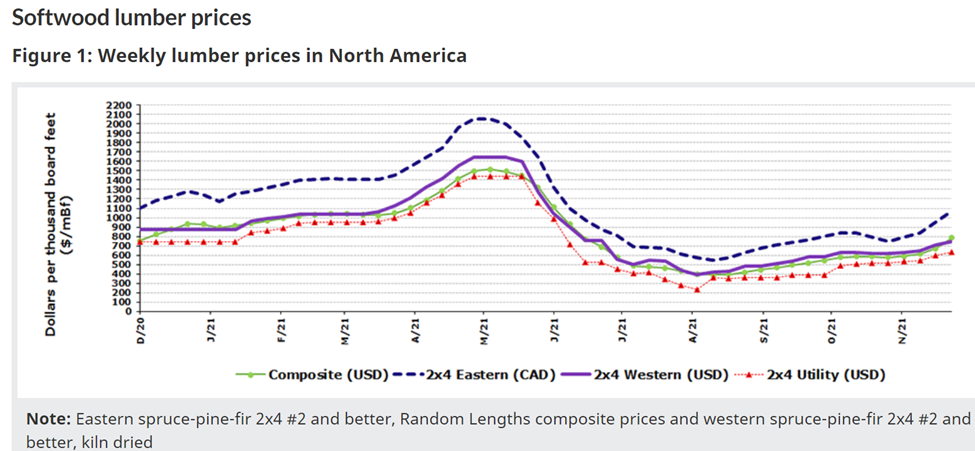

Anyone who tried to build or remodel a wood-framed house this year faced a horrible shock — lumber prices literally went through the roof. From a year ago this past June the popular building material rocketed 377%, partly due to high demand for renovations by covid-bound homeowners. Normally priced between $200 and $300 per thousand board feet, lumber futures hit an all-time high of $1,500 in March of this year and while they fell as low as $450 in October, lumber has bounced back up to $1,119, as of time of writing.

US lumber futures. Source: Trading Economics

In British Columbia there has been a lot of press about the impacts of over-logging on towns like Merritt recently hit by devastating floods. In 2018 Grand Forks launched a class-action lawsuit against the BC government and several timber companies, alleging that excessive logging caused the displacement of thousands of people and millions of dollars in property damage.

Ripping out too many trees and root systems leaves the land exposed and vulnerable to flooding. The “atmospheric rivers” we saw moving across the Pacific Northwest dumping record-breaking amounts of rain will only become more frequent as the planet continues to warm, causing unstable weather.

Before the atmospheric rivers we had the “heat dome” which sucked all the moisture out of the forests leaving them vulnerable to forest fires.

Out-of-control wildfires, evacuation orders, and dangerous to breathe smoke that blankets communities for weeks, are now annual events in the BC Interior. According to the CBC, nearly 8,700 square kilometres of land were burned in 2021 due to wildfires, making it the third worst year on record.

Lumber prices will likely be pressured in coming years with regular forest fires, along with a shorter logging season. When humidity and temperatures reach a certain point, it becomes too dangerous to log and the bush gets shut down. Climate change can also reduce the amount of logging being done in the fall, when roads are late to freeze up, and in spring, when the thaw, or “breakup”, comes sooner than normal.

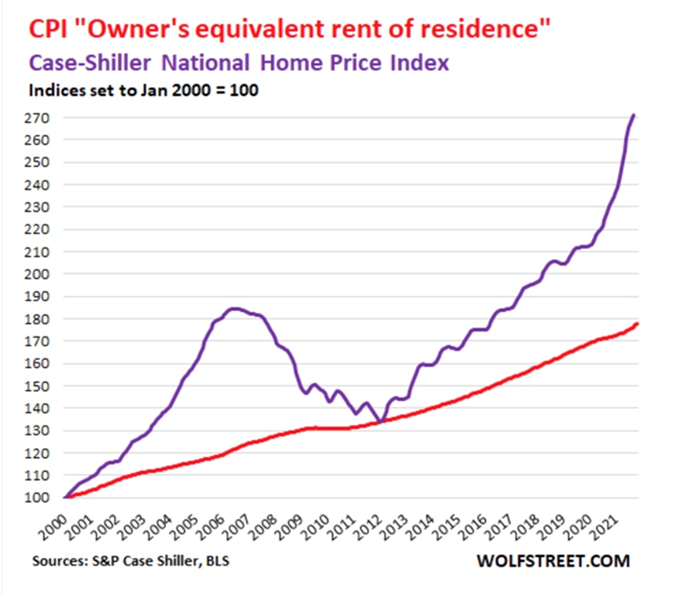

Wolf Street reports “actual home prices have spiked by historic amounts,” with the Case-Schiller Home Price Index which tracks price changes of the same house over time, soaring 20% year over year. The “owner’s equivalent of rent” which measures the costs of home ownership (red line in graph below) is also tracking higher.

Transportation

This year China and Europe experienced an energy crisis.

Flooding across China’s key coal-producing provinces, resurgent demand for Chinese goods in the wake of pandemic easing, and market distortions including power rationing and price controls, were behind an energy shortage that pushed coal and natural gas prices to record highs.

In Europe, a colder-than normal last winter depleted natural gas inventories, causing electricity prices to soar, as demand from rebounding economies surged too fast for supplies to match, BNN Bloomberg reported.

Oil reportedly extended gains to the highest in three weeks, Thursday, as US crude stockpiles dropped the most since September, and the dollar gained, bolstering commodities.

The usual energy market dynamics are being overshadowed by the global transition from fossil-fueled energy generation to renewable power sources namely wind, solar and hydro.

As governments and institutional investors divest themselves of funds that traditionally flowed into fossil fuels, i.e. coal/ oil & gas producers, or pipeline infrastructure, they are trying to bring on renewables to replace the lost output.

However, with no easy way to store the energy generated from renewables, utilities are finding they must continue to utilize “dirty” coal and natural gas, despite commitments to lessen their dependence on fossil fuels to fight climate change.

The problem was made worse this year by low output of hydro and wind power sources, due to unexpectedly low wind speeds and little rainfall.

********

More from Silver Phoenix 500