Why Bad News Is Good News In Europe: 7 Charts Showing What You Really Need To Know

There’s little denying that the U.S. economy is on the upswing since the recession. Manufacturing is strong, jobless claims are falling and wages are rising. Delta Airlines, which we own in our Holmes Macro Trends Fund (MEGAX), recently announced that it will be giving its 80,000 employees $1.1 billion in profit sharing, while Wal-Mart, held in our All American Equity Fund (GBTFX), unveiled plans to hike its minimum wage to $9 an hour in April.

Indeed, things are shaping up here in the U.S., but unfortunately this has not been the case in Europe. From Greek drama to Russian aggression, bad news seems to be the order of the day.

Until now.

Because of central banks’ monetary easing, weakening currencies and low fuel costs—courtesy of the American fracking boom—Europe is finally showing signs that it’s ready to turn the corner and set a path toward lasting economic recovery.

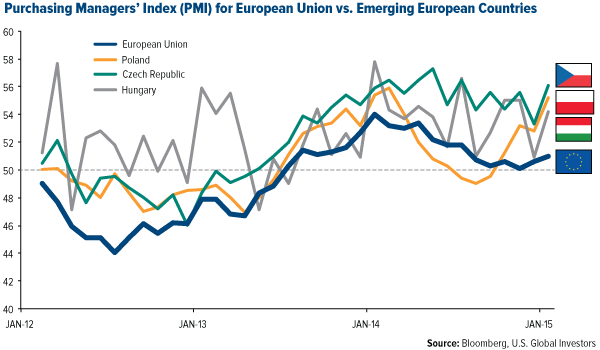

- Emerging Europe PMIs Swinging Up

The Purchasing Managers’ Index (PMI), as I’ve often said, is a highly effective tool that we use to forecast manufacturing activity six months out. Any reading above 50 indicates growth in manufacturing; anything below, contraction. This allows us to manage our expectations and get a good sense of where to position our funds.

As you can see, the European Union (EU) as a whole has recently improved, but emerging countries such as the Czech Republic, Poland and Hungary are posting very solid numbers in the mid-50s range. Much of this is due to low fuel costs and weaker currencies, which make exports more attractive.

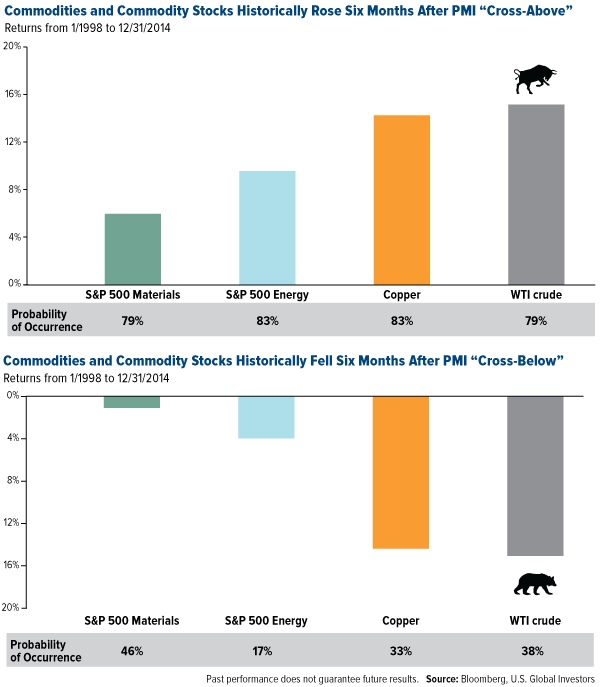

2. Growth in the Eurozone Is Good for the Globe

Our investment team’s research has shown that when the one-month reading for the global PMI crossed below the three-month moving average, there was a significant probability that materials, energy and commodities would fall six months later. Conversely, when it crossed above, manufacturing activity would ramp up, which greatly improved the performance of commodities such as copper and crude oil, not to mention the materials and energy sectors.

It’s very welcome news, then, to see growth in the eurozone, since its PMI readings are factored into the global score. Last week we learned that the preliminary Flash Eurozone PMI advanced to 53.5 for the month of February. This is huge. Not only is it a seven-month high for the eurozone, but it’s also nearly in line with the U.S. reading, which came in at 54.3. Even France—a perennial and disappointing laggard in manufacturing—posted its best results in three-and-a-half years.

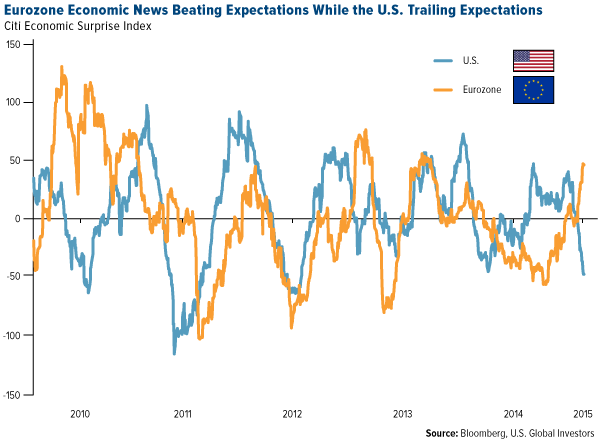

3. Surprise! Europe Is Beating Expectations

The Citi Economic Surprise Index, simply put, tells you if a country or region’s economic news is beating—or, conversely, falling below—analysts’ expectations. The higher the number, the more it indicates that economic data is exceeding forecasts.

You can see above where the eurozone has surprised consensus. For most of 2014, the region was in a declining trend, whereas the U.S. was headed higher. More recently, though, we’ve seen a huge advancement in Europe, despite negative news coming out of areas such as Greece—which last week managed to strike a deal with its euro-partners to extend the Mediterranean country’s bailout program by four months.

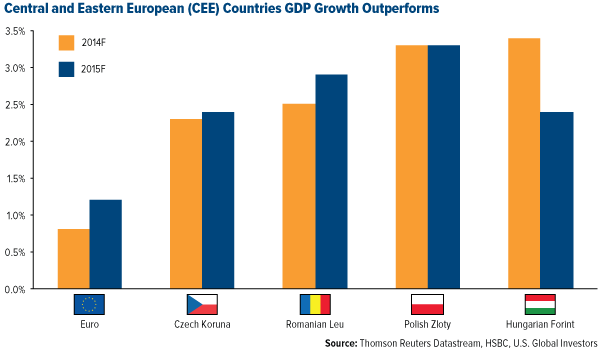

4. GDP Growing

If you look at Europe’s GDP as a whole, it’s expected to grow slightly over 1 percent in 2015. But the GDP in Eastern European countries such as the Czech Republic, Romania, Poland and Hungary is expected to grow double that or more.

These countries are benefiting from the broad recovery, for sure, but they also have their own dynamics. As emerging markets, they have more room to run and grow.

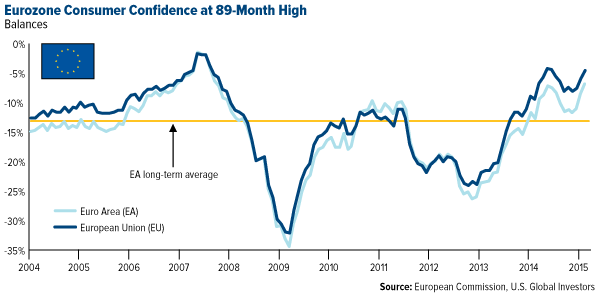

5. No Lack of Confidence in Consumption

Another sign that the European recovery is underway is the recent uptick in spending habits. Not only does the consumer confidence index (CCI) for the eurozone far exceed its long-term average, but it’s also at its highest reading since soon before the financial crisis.

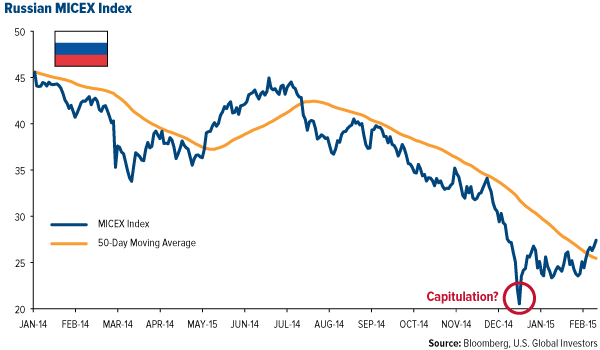

6. Russia, the Not-So-Bad News Bear?

Nearly every day we’re reminded of Russia’s political and financial troubles, but the worst is likely behind us. It appears as if Russia’s market and currency, the ruble, bottomed in mid-December. This is also the first time since the summer that the MICEX Index crossed above its 50-day moving average, breaking through resistance.

The situation in Ukraine is not pretty, but global investors understand it and are getting comfortable putting their money in Russia again because it’s inexpensive. The bad news has been priced in, and it looks as if the market is willing to move higher.

Russian credit default swaps (CDS) are also looking better. CDSs allow sellers to assume and buyers to reduce default risk on a bond. The swap spreads improved in February, indicating the market is looking past current events such as international sanctions and the ceasefire in Ukraine and seeing Russia’s risk declining in the future.

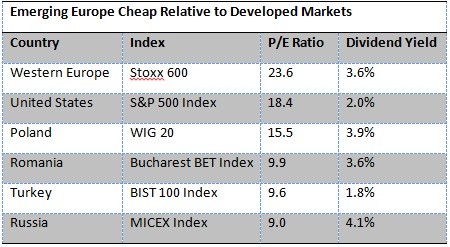

7. Low Valuations, High Dividend Yields

Emerging European equities, like Russian stocks, are trading at a big discount relative to those in U.S. and Western European markets.

Many of the emerging European countries are currently trading at less than 10 times. Therefore, you get that winning combination of low valuation and high dividend yield.

We’re definitely starting to see the early signs that Europe is reflating its economy. Attractive PMI data, positive economic surprises and growing consumer confidence all point to a strong recovery, one that should bode well for global investors in general and our Emerging Europe Fund (EUROX) specifically.

In case you missed this week’s webcast on this very topic, you can still listen to the replay on demand and download the slideshow.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Stock markets can be volatile and share prices can fluctuate in response to sector-related and other risks as described in the fund prospectus.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio. The Emerging Europe Fund invests more than 25% of its investments in companies principally engaged in the oil & gas or banking industries. The risk of concentrating investments in this group of industries will make the fund more susceptible to risk in these industries than funds which do not concentrate their investments in an industry and may make the fund’s performance more volatile.

The J.P. Morgan Global Purchasing Manager’s Index is an indicator of the economic health of the global manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The Eurozone Purchasing Managers' Index is produced by Markit and is based on original survey data collected from a representative panel of around 5,000 companies based in the euro area manufacturing and service sectors. National manufacturing data are included for Germany, France, Italy, Spain, the Netherlands, Austria, the Republic of Ireland and Greece. National services data are included for Germany, France, Italy, Spain and the Republic of Ireland. The flash estimate is typically based on approximately 85%–90% of total PMI survey responses each month and is designed to provide an accurate advance indication of the final PMI data.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The Citigroup Economic Surprise Indices are objective and quantitative measures of economic news. They are defined as weighted historical standard deviations of data surprises (actual releases vs Bloomberg survey median). A positive reading of the Economic Surprise Index suggests that economic releases have on balance been beating consensus. The indices are calculated daily in a rolling three-month window.

The Consumer Confidence Index (CCI) is an indicator which measures consumer confidence in the Economy.

The MICEX Index is the real-time cap-weighted Russian composite index. It comprises 30 most liquid stocks of Russian largest and most developed companies from 10 main economy sectors. The MICEX Index was launched on September 22, 1997, base value 100. The MICEX Index is calculated and disseminated by the MICEX Stock Exchange, the main Russian stock exchange.

The STOXX 600 Banks (Price) Index (SX7P) is a capitalization-weighted index which includes European companies that are involved in the bank sector.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The WIG20 Index is a modified capitalization-weighted index of 20 Polish stocks which as listed on the main market. The index is the underlying instrument for futures transactions listed on the Warsaw Stock Exchange.

The Bucharest Exchange Trading Index (BET) is a capitalization weighted index, comprised of the 10 most liquid stocks listed on the BSE tier 1. The index is a Price index and was developed with a base value of 1000 as of September 22, 1997.

The Borsa Istanbul 100 Index is a capitalization-weighted index composed of National Market companies except investment trusts. The constituents of the BIST National 100 Index are selected on the basis of pre-determined criteria directed for the companies to be included in the indices.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the All American Equity Fund, Holmes Macro Trends Fund and Emerging Europe Fund as a percentage of net assets as of 12/31/2014: Delta Air Lines, Inc. 1.28% Holmes Macro Trends Fund; Wal-Mart Stores, Inc. 1.14% All American Equity Fund.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time.

********

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com.

More from Silver Phoenix 500