Hitting A "BRIC" Wall

share

share

share

share

share

share

share

share

share

share

Have the peripheral BRICS hit a brick wall? After years as investor havens with stellar performance, has the luster been tarnished and something much darker started to cast a dark shadow?

The just concluded G20 Summit in St Petersburg, Russia sheds light on the seriousness of the concern surrounding the plummeting currencies in three of the BRICS (Brazil, India and South Africa).

Away from the glare of the media, the BRICS according the ChinaDaily cobbled together an emergency $100B currency reserve 'Firewall Fund'. The BRICS are obviously worried. The 1997 Asia Crisis taught emerging economies the importance of strong currency reserve positions in event that 'hot' capital flows became volatile and changed direction. Despite building currency reserves the BRICS still feel what is looming will leave them potentially exposed. As the lead BRICS member, China will inject $41 billion into the planned 'Firewall' Fund' and each of Brazil, India and Russia will ante $18 billion, with South Africa paying the remaining $5 billion.

Additionally, urgent side meetings were held separately to finalize the BRICS-led New Development Bank. Negotiated were its capital structure, membership, shareholding and governance. It was leaked that the bank will have an initial subscribed capital of $50 billion from the BRICS countries. It would appear there was more urgency to the above discussions than an escalating G20 focus on the Syrian conflict.

When participating in the main G20 session, it was clear what the BRICS agenda. There focus was the impact of the US monetary "TAPER" direction and the apparent US disregard for the global consequences. The BRICS veiled contempt towards US policy was a direct result that since 2008 they have had to fight the hot money flows that accompanied multiple US Quantitative Easing programs, with resulting rise in currencies hurting exports, while FDI artificially pushing up bond prices, creating overdevelopment and inflation pressures. Now with the US reversing course the BRICS feel the 'back lash' as money flees, investment stops, currencies plummet and rates rapidly rise. Moreover, the BRICS see themselves facing serious economic, social and political problems which they feel are not of their making. They see themselves facing a 'no win' decision of:

"Impose capital controls OR let the Fed run your economy" Jackson Hole Summit

When it came to the central discussion at the G20 regarding Syria, is it any wonder that those most vocal against US intervention were these same countries? They have lost confidence in American global leadership and policy formulation.

Speaking at a final G20 press conference, Russian President Vladimir Putin said:

"Russia, China, India, Indonesia, Brazil, South Africa and Italy came against military actions in Syria."

Putin also said: "he was surprised to see that ever more participants in the summit, including the leader of India, Brazil, the South African Republic, and Indonesia were speaking vehemently against a possible military operation in Syria. Putin cited the words of the South African President, Jacob Zuma, who said many countries were feeling unprotected against such actions undertaken by stronger countries."

Speaking on behalf of the BRICS, Chinese Vice-Minister of Finance Zhu Guangyao, said:

"We hope the US will carefully consider its decision to exit its quantitative easing policy to make more contribution to the global economy"

THE REALITY OF THE ECONOMIC DATA

What is missing from a clear understanding of the frustrations of the emerging economies and the BRICS is the reality of the economic data. Harvard Professor Ricardo Hausmann, a former minister of planning of an economically imperiled Venezuela and a former Chief Economist of the Inter-American Development Bank, has a unique background which allows him to spell out the economic realities.

Between 2003 and 2011, GDP in current prices grew by a cumulative 35% in the United States, and by 32%, 36%, and 49% in Great Britain, Japan, and Germany, respectively, all measured in US dollars. In the same period, nominal GDP soared by 348% in Brazil, 346% in China, 331% in Russia, and 203% in India, also in US dollars.

And it was not just these so-called BRIC countries that boomed. Kazakhstan’s output expanded by more than 500%, while Indonesia, Nigeria, Ethiopia, Rwanda, Ukraine, Chile, Colombia, Romania, and Vietnam grew by more than 200% each. This means that average sales, measured in US dollars, by supermarkets, beverage companies, department stores, telecoms, computer shops, and Chinese motorcycle vendors grew at comparable rates in these countries. It makes sense for companies to move to where dollar sales are booming, and for asset managers to put money where GDP growth measured in dollars is fastest.

One might be inclined to interpret this amazing emerging-market performance as a consequence of the growth in the amount of real stuff that these economies produced. But that would be mostly wrong.

Consider Brazil. Only 11% of its China-beating nominal GDP growth between 2003 and 2011 was due to growth in real (inflation-adjusted) output. The other 89% resulted from 222% growth in dollar prices in that period, as local-currency prices rose faster than prices in the US and the exchange rate appreciated.

Some of the prices that increased were those of commodities that Brazil exports. This was reflected in a 40% gain in the country’s terms of trade (the price of exports relative to imports), which meant that the same export volumes translated into more dollars.

Russia went through a somewhat similar experience. Real output growth explains only 12.5% of the increase in the US dollar value of nominal GDP in 2003-2011, with the rest attributable to the rise in oil prices, which improved Russia’s terms of trade by 125%, and to a 56% real appreciation of the ruble against the dollar.

By contrast, China’s real growth was three times that of Brazil and Russia, but its terms of trade actually deteriorated by 26%, because its manufactured exports became cheaper while its commodity imports became more expensive. The share of real growth in the main emerging countries’ nominal US dollar GDP growth was 20%.

The three phenomena that boost nominal GDP – increases in real output, a rise in the relative price of exports, and real exchange-rate appreciation – do not operate independently of one another.

Countries that grow faster tend to experience real exchange-rate appreciation, a phenomenon known as the Balassa-Samuelson effect. Countries whose terms of trade improve also tend to grow faster and undergo real exchange-rate appreciation as domestic spending of their increased export earnings expands the economy and makes dollars relatively more abundant (and thus cheaper).

Clearly, all is not as it has appeared around the globe! Consider global growth has been much of a mirage.

After a relentless 6 quarter recession in the EU and the slowing of their primary export growth market in China, Emerging Markets are hitting a brick wall.

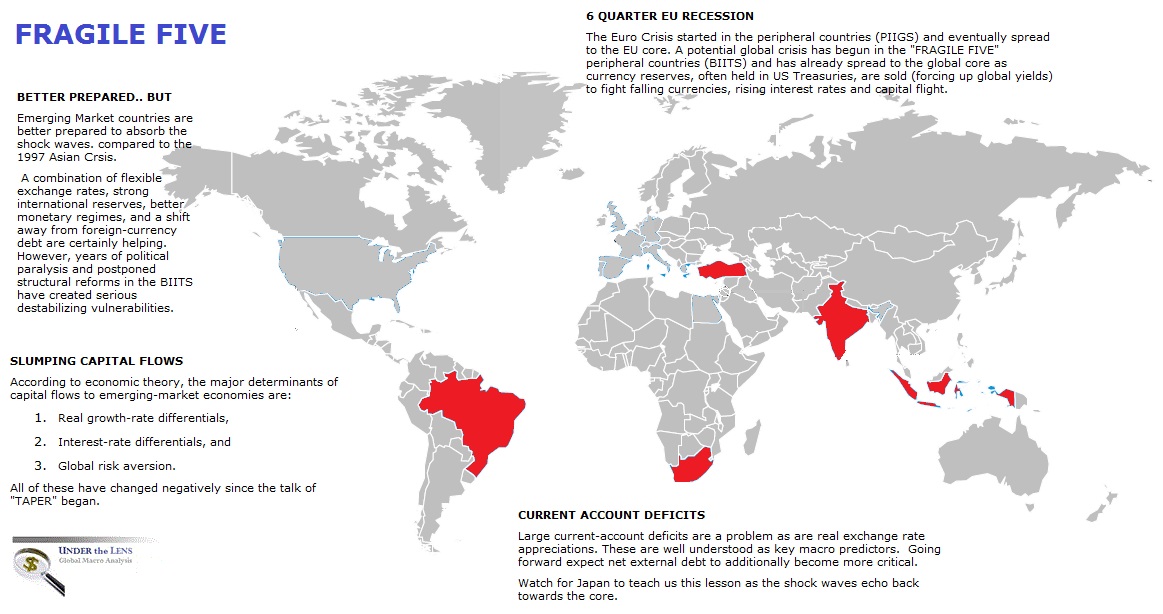

"FRAGILE FIVE"

As I have written about before, Brazil, India, Indonesia, Turkey and South Africa (BIITS) all have something very important in common, they are all peripherals to their major markets! Additionally, and maybe not by coincidence they also all have large Debt-to-GDP ratios and significant negative Current Accounts.

Many other previously fast-growing emerging-market economies – for example, Turkey, Argentina, Poland, Hungary, and many in Central and Eastern Europe – are experiencing a similar slowdown. So, what is ailing the BRICS and other emerging markets?

OVERHEATING: First, most emerging-market economies were overheating in 2010-2011, with growth above potential and inflation rising and exceeding targets. Many of them thus tightened monetary policy in 2011, with consequences for growth in 2012 that have carried over into this year.

COUPLED ECONOMIES : Second, the idea that emerging-market economies could fully decouple from economic weakness in advanced economies was far-fetched: recession in the Eurozone, near-recession in the United Kingdom and Japan in 2011-2012, and slow economic growth in the United States were always likely to affect emerging-market performance negatively – via trade, financial links, and investor confidence. For example, the ongoing Eurozone downturn has hurt Turkey and emerging-market economies in Central and Eastern Europe, owing to trade links.

STATE CAPITALISM: Third, most BRICS and a few other emerging markets have moved toward a variant of state capitalism. This implies a slowdown in reforms that increase the private sector’s productivity and economic share, together with a greater economic role for state-owned enterprises (and for state-owned banks in the allocation of credit and savings), as well as resource nationalism, trade protectionism, import-substitution industrialization policies, and imposition of capital controls.

This approach may have worked at earlier stages of development and when the global financial crisis caused private spending to fall; but it is now distorting economic activity and depressing potential growth. Indeed, China’s slowdown reflects an economic model that is, as former Premier Wen Jiabao put it, “unstable, unbalanced, uncoordinated, and unsustainable,” and that now is adversely affecting growth in emerging Asia and in commodity-exporting emerging markets from Asia to Latin America and Africa. The risk that China will experience a hard landing in the next two years may further hurt many emerging economies.

COMMODITY SUPER-CYCLE: Fourth, the commodity super-cycle that helped Brazil, Russia, South Africa, and many other commodity-exporting emerging markets may be over. Indeed, a boom would be difficult to sustain, given China’s slowdown, higher investment in energy-saving technologies, less emphasis on capital- and resource-oriented growth models around the world, and the delayed increase in supply that high prices induced.

"TAPER":The fifth, and most recent, factor is the US Federal Reserve’s signals that it might end its policy of quantitative easing earlier than expected, and its hints of an eventual exit from zero interest rates, both of which have caused turbulence in emerging economies’ financial markets. Even before the Fed’s signals, emerging-market equities and commodities had underperformed this year, owing to China’s slowdown. Since then, emerging-market currencies and fixed-income securities (government and corporate bonds) have taken a hit. The era of cheap or zero-interest money that led to a wall of liquidity chasing high yields and assets – equities, bonds, currencies, and commodities – in emerging markets is drawing to a close.

CURRENT ACCOUNTS: Finally, while many emerging-market economies tend to run current-account surpluses, a growing number of them – including Turkey, South Africa, Brazil, and India – are running deficits. And these deficits are now being financed in riskier ways: more debt than equity; more short-term debt than long-term debt; more foreign-currency debt than local-currency debt; and more financing from fickle cross-border interbank flows.

These countries share other weaknesses as well: excessive fiscal deficits, above-target inflation, and stability risk (reflected not only in the recent political turmoil in Brazil and Turkey, but also in South Africa’s labor strife and India’s political and electoral uncertainties). The need to finance the external deficit and to avoid excessive depreciation (and even higher inflation) calls for raising policy rates or keeping them on hold at high levels. But monetary tightening would weaken already-slow growth. Thus, emerging economies with large twin deficits and other macroeconomic fragilities may experience further downward pressure on their financial markets and growth rates.

BRICS elements (Brazil , India and South Africa) hit hard.

A disillusioned Sunanda Sen, a former professor at Jawaharlal Nehru University, New Delhi, recently wrote the following which reflects the plight of the peripheral BRICS.

Volte-faces, from scenes of apparent stability marked by high GDP growth and a booming financial sector to a state of flux in the economy, can completely change the expectations of those who operate in the market, facing situations with an uncertain future. Possible transformations as above, were identified by Kindleberger in 1978 as a passage from manias, which generate positive expectations, to panics, which head toward a crisis.

While manias help continue a boom in asset markets, they are sustained by using finance to hedge and even speculate in the asset market, as Minsky pointed out in 1986. However, asset-markets bubbles generated in the process eventually turn out to be on shaky ground, especially when the financial deals rely on short-run speculation rather than on the prospects of long-term investments in real terms. With asset-price bubbles continuing for some time under the influence of what Shiller described in 2009 as irrational exuberance, and also with access to liquidity in liberalised credit markets, unrealistic expectations of the future under uncertainty sow the seeds for an unstable order. The above leads to Ponzi deals, argues Minsky, with the rising liabilities on outstanding debt no longer met, even with new borrowing, since borrowers are nearing insolvency. Situations as above trigger panics for the private agents in the market, who fear possible crisis situations. These are orchestrated with herd instincts or animal spirits in the market as held by Keynes in 1936. In the absence of actions to counter the market forces, a possible crisis finally pulls down what in hindsight looks like a house of cards!

Indeed, when markets have the freedom to choose the path of reckless short-run financial investments, with high risks and high returns, the individual’s profit calculus eventually proves wrong in the aggregate, leading to a path of downturn, not just for the financial market but for the economy as a whole. This is how manias lead to panics and then to crisis in an economy.

CONCLUSION

Like the EU Crisis where the problems started in the peripherals and worked to the core. The problems of the global peripherals can likewise be anticipated to work towards the global core of economic growth.

Read the full story in this month's Global Macro Tipping Points at GordonTLong.com

Free Trials available for this issue. Sign Up

share

share

share

share

share

More from Silver Phoenix 500