Fabulously Fake Facts – “G” In GDP Stands For “Gullibility”

While glowing presidential proclamations about US GDP growth last week did nothing to prevent the stock market from rushing headlong over the cusps of a FAANG stock ledge, the market is taking a breather today. So, let’s take a breather and go back and look at why that GDP report had no bite.

Quite simply, I think stock investors looked at the surfacing of real problems in their favorite FAANG stocks and, so, failed this time to find any fun in the frivolous fiction of government factoids. GDP reportage has been fake for years, and it is no less fake under Trump than under any other president. Fake is where you find it. You can find it as much on Fox as on CNN.

Budget Mnunchkins advising the president

Larry Kudlow by Gage Skidmore [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons

JPMorgan Chief Jamie Dimon says he knows that two of Trump’s advisors assured Trump there would be no retaliation toward his tariffs. While Dimon refused to say who the two were, I will speculate that they were none other than the wacky team of Kudlow & Moore. I think Krazy Kudlow has been sniffing the ether or has returned to his cocain habit because “no retaliation on tariffs” sounds like the kind of shoot-from-the-hip garbage-bin economic assurance for which Kudlow & Moore are branded. Oh, how lucky we are to have them as the president’s chief economic advisors!

Obviously, whoever gave Trump this advice, was wrong. The president’s planners were wrong also about their statements that the Trump Tax Cuts would pay for themselves. As a result of their malconcocted plan, the Treasury Department just released new predictions that its borrowing for the remainder of the year will rise to the highest amount since the financial crisis in the second half of 2008 when borrowing set an all-time record as an attempted escape hatch from the Great Recession was quickly cut into the deflating economy.

The department has raised its second-half borrowing estimate to $769 billion, a soaring amount beat only by the $1.1 trillion of emergency spending in July-December 2008. Only, this time we are told by the administration we are not in any emergency at all; we are, in fact, in the middle of a robust economic expansion. Would someone please explain to me why a robust economy needs the second-largest semi-annual deficit spending in the history of the nation just to keep afloat?

These Treasury Dept. estimates for new debt issuance that were “quite a bit higher than our expectations,” according to one economist, didn’t stop the president’s men from making additional rosy proclamations into the nation’s thought void:

Administration officials say a stronger economy will boost government revenue and help shrink the budget deficit. Treasury Secretary Steven Mnuchin said Sunday the U.S. economy is “well on the path” for four or five years of sustained annual growth of 3 percent. (Newsmax)

Sure — just like there won’t be any retaliation for Trump’s tariffs.

The government’s necessity to expand its bond auctions due to higher fiscal spending and lower revenue is being complemented right now by the Fed’s choice to unwind from its own government bond purchases. Higher spending, lower revenue, and higher need to refinance debt that had been carried by the Fed until now — sounds like the perfect fiscal storm to me! Bear in mind that the Treasury’s auction near the end of July resulted in the government having to pay the highest interest on its two-year bonds since 2008.

In February of 2018, the thirty-year bond finally broke above its decadal (“recovery” period) downward trend line:

I wonder if Mnuchin and Kudlow get together to mnunch on the pot brownies or share a bong once in awhile. Of course, Mnuchin, another co-architect of the Trump Tax Cuts along with the Kudlow & Moore team, has to keep talking up the auto-financing of tax cuts that have benefited his own family greatly. He has to keep that belief alive in order to hold off the pitch forks a little longer so that he can complete the construction of his underground bunker mansion. Bunker mansions are the new thing of the rich, you know — seen as a necessity for the times ahead:

These are the times when the One-Percenters know they will need to protect themselves.

The “G” in GDP stands for “gullibility”

If you believe any of this stuff from the administration, I recommend you check the light on your brain charger when you plug it in at night to make sure it is actually working — that or stop sniffing the ether before bedtime with Lunatic Larry. This is all just the doctrine by which the priesthood of the One Percent keeps you lulled out of rebellion so they can continue getting richer. It is such stuff as dreams are made of, not reality.

If you think I’m just being a NeverTrumper, let’s dig into the facts about this GDP and all GDP government reportage:

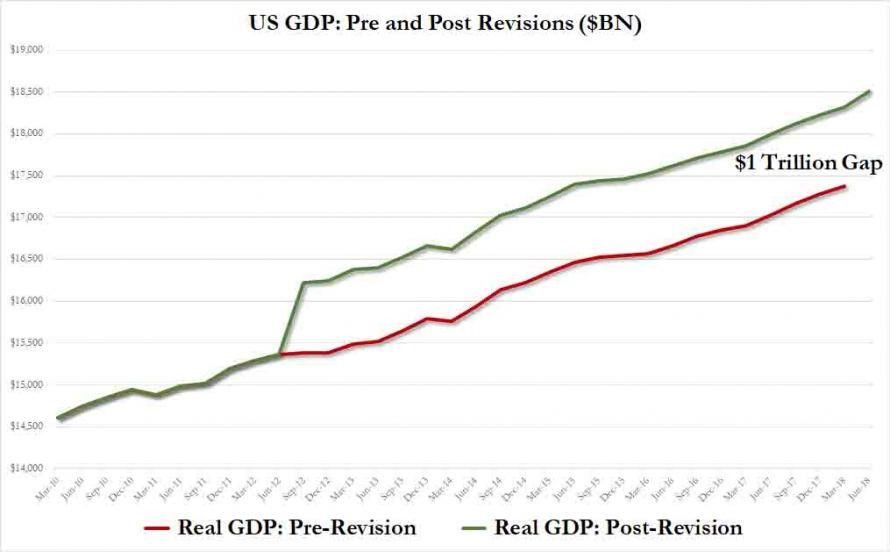

First and foremost, Q2 was the first quarter in which the government applied its new metrics for measuring GDP. Under these new metrics, the government has revised the entire economy one trillion dollars higher. Yes, Q2 showed that the economy is now percolating at the $18.5 trillion level, even though Q1 was reported as $17.37 trillion. Don’t worry, the numbers have been reconciled so that Q1 has now been revised to $18.3 trillion because no one would believe a trillion-dollar jump in just one quarter. In fact, history going back to June 2012 has been revised to a better outlook:

Don’t ask me why they felt the revisions only merited going back to 2012. Just too lazy I guess to revise all of history. The important thing as that these new metrics allow a rosier picture of everything. Of course, this is not the first time GDP metrics have been revised in order to “present a more accurate picture of the economy.” What is interesting, though, is that every time the way of measuring GDP gets revised, the results show a better image of the economy. Don’t you have to be just a little suspicious about government changes that always make things look better?

Second, and almost as important, consider what those non-retaliation tariffs by China did to GDP. You know that Chinese businessmen and businesswomen are recognized for being prudent with every penny. So, it should come as no surprise that, when China announced it would implement an non-retaliation tariff on US soybeans, that every soy sauce company in China found as much dry storage as they could find and hoarded soy beans. If you actually dig into the US GDP growth numbers for Q2, you discover this interesting fact: the largest contributor to growth was in soybean sales. Highly unusual to say the least that soybeans are a leading cause of economic growth in the US!

Who would have guessed that!? And, if they really are such a cause of economic growth, why did President Trump just implement a massive subsidy for soybean farmers?

Now, ask yourself what happens when you pull sales from a future quarter into the present. David Stockman has an answer for you:

Each subsequent quarter gets smaller for about a year.

Since the biggest contributor to Q2 GDP growth was soybean sales that were pulled into the present by all Chinese companies that wanted to remain competitive in the face of huge tariffs on their main ingredient for production, do you suppose these companies will be buying any soybeans in the next few quarters? Why do you think Trump just announced a huge government subsidy to help out soybean farmers and exacted a promise of soybean purchases from Europe? It sure isn’t because soybean growth in the national economy is going to be there when this quarter gets reported. While stocks from previous harvests have sold out, there won’t be any Chinese buyers for awhile to come. And guess who uses more US soybeans — Europe or China? I don’t think Europe is going to save us. Hence the new subsidy.

In other words, last quarter’s GDP growth will wind up becoming this quarter’s GDP shrinkage.

Third, and not too distant, consider that GDP numbers are always revised down in the quarters and even years to follow. It is not uncommon for them to eventually wind up revised down by half! They are consistently overoptimistic on the first release because the government doesn’t care what you think about GDP that is a year old. It cares what you think about today’s GDP because that is the number upon which you will be judging today’s government.

So, the numbers start in a dream and age into reality. Conservative estimates simply get in the way of Dreamliner growth because reportage on GDP has the potential to be self-fulfilling: report a high number, and people become ebullient. Happy people feel free to spend more in the current quarter, helping move that number higher in the next report.

The government always wants to get that snowball rolling. So, it does not even try to be conservative in its GDP estimate. It tries to be as positive with the numbers as it can justify. It will correct them toward getting real later when they no longer matter because they are old news. (In fact, correcting them downward later has the double-positive effect of making the next new numbers look even prettier! GDP appears to grow a half a point in the latest quarter when we revise the previous quarter down a half a point. Nice! That is more so the truth further down the road with year-on-year figures when we lose track of the fact that we’ve been adjusting the number down for a few quarters.)

It is unbelievably easy for the government to cook the first release of GDP numbers for one surprising (to many) reason: nearly the entire number is based on guesses. There are almost not factual statistics that go into the first release. Instead, the first release is the government’s compilation of estimates, many of which are inferences. As the actual facts gradually come in, the number becomes more real. And why err on the small side?

Consider, too, that the number just reported is annualized. It is a statement of “here is what annual GDP growth will be IF growth continues at the same rate as it did last quarter.” But that never happens. One quarter is up, and the next quarter is down a little. We have to stay at this level for an entire year for the economy to actually reach the president’s 4.1% growth figure.

Finally, consider the prospect that tax stimulus is expected to fade — that Q2 is expected to be the quarter that got the most bang out of the tax buck because of all the one-time repatriation taking place. The Trump Tax Cuts front-loaded all the biggest benefits into 2018 in order to get some movement happening. They don’t get better as we move into 2019.

Besides fading stimulus, we have rising debt costs becoming more likely due to that big increase by the Treasury in debt issuance that has just been announced, and we have the Fed’s planned interest-rate increases.

Reality can be a real headbanger

And I’m not talking heavy-metal music here — just a low pipe in the parking garage at head level.

Morgan Stanley claims the Q2 number (half-baked as it is) is a one-off. In fact, it is a whole bunch of one-offs all combined into one gloriously fabricated number:

An unusually large number of one-off factors appear to have boosted 2Q GDP, many of which are directly related to escalating trade concerns. As companies and countries race to secure supplies that may become expensive later on, exports have surged and inventories have swelled. If these trends are one-time adjustments (and our economists believe they are), the ‘payback’ in 2H could be significant. Enjoy the 2Q GDP number, which may be the last best print for a while….

The ‘stockpiling’ in exports could be responsible for 1.5 percentage points…. ‘Stockpiling’ also appears to be at work for US companies, albeit to a more limited extent. The inventory build in 2Q is tracking at +US$38 billion, versus a +US$10 billion rate in the prior two quarters. And what’s more interesting is the areas where those inventories are building, which have material overlaps with trade: electrical goods, machinery equipment, motor vehicles and parts. (Zero Hedge)

In total Morgan Stanley believes the combination of stockpiling in US inventories ahead of tariffs and increase in exports (for the sake of stockpiling in other nations) accounts for more than two points on that 4.1% growth number. Year-on-year, the economy actually did grow only 2.2% as compared to GDP in Q2 2017; and you have to consider that the 2017 number has already been revised lower several times in order to make that gap as wide as possible. If you take two points off of that as being due solely to tariffs, that leaves us with no year-on-year growth at all.

If Morgan Stanley’s statement about the tariff impact domestically and abroad is true, then real GDP growth actually stunk like a sack of skunks. In which case, Trump’s desire to trumpet about his success this quarter could be his demise next quarter when the number goes deeply south … just in time for elections.

Even if there had been no stockpiling, tariffs are certain to diminish economic production in the months ahead. You simply cannot make things more expensive and not diminish demand. That’s a fool’s dream.

When you consider that, in 1998 and 1999, real GDP growth (as opposed annualized numbers) was 5% and 4.7% respectively, then 4.1% is not all that great, considering it is happening in a period of the greatest fiscal-spending-tax-cutting stimulus in the history of the nation. It’s not really much to brag about, although it may seem better than the paltry Obama years. That, however, is something like boasting you are the fastest turtle to race across the Sahara. (Probably not anything near an all-time land-speed record that makes America great again when compared to its former glory days.)

Oh, and just kidding on beating the Obama years. Even Obama had two quarters where initial GDP reportage was higher than Q2 2018. In fact, Q3 2104 pushed past an annualized 5% GDP growth! (Naturally, revised lower as time flew by and projections transferred into realities.) And Obama’s last quarter of his first year (2009) came in at 5.6%, and that was deep in the pit of the financial crisis!

So, you can call 4.1% growth a boom if it makes you feel good, but it is far less than the Obama Boom, and we all know that didn’t last. (In the end, 2014 real GDP growth came in at a pathetic 2.7% for the year.) After all, that is how you make America great again — by boasting a lot until people believe you. While it might look good on a cap, you can’t eat it.

Of course Krazy Kudlow, Laughable Laffer and Moronic Moore all say the boom is on. Believe them if you want, but none of them has a respectable track record for seeing into the future; plus it is the success of their own plan they are pitching. We’ve heard this song before. Remember the “green shoots” of 2009 or the “recovery summer” promised in 2010 by the Treasury Secretary of that time, Tim Geithner? Or how about more recently, the “globally synchronized growth” of 2017? That ended before you could sneeze at it.

This recovery summer is already rapidly cooling toward the winter of our discontent. You can scoff at my warnings while banging your head on the low-hanging pipes all you want for all I care. The sound of your head will help me know where to duck in the darkness of these government fake facts.

Taking stock of today’s market action

Oh, and, lest you think the reprieve I mentioned in the stock market’s fall actually means anything, Nomura believes tomorrow will be a day of carnage. Why? For the very reason I’ve said the market will go down.

Long ago, Goldman Sachs noted,

Back in the heyday of the Fed’s QE, it had become a trader mantra: buy stocks on POMO days, or when the Fed was actively purchasing bonds in the open market, and generate risk-free, outsized returns…. “If you only owned S&P on days when the Fed conducted Open Market Operations (in US Treasuries), your cumulative return is over 11%. in addition, 6 of the 7 times when S&P rallied 1% or more, OMO was conducted that day. this compares to a YTD return of 5.8%. the point: you would have outperformed the market 2x by being long on just the 16 days when – this is the important part – you knew in advance that OMO was to be conducted.” (Zero Hedge)

And where does that leave us now that the Fed is discharging treasuries, rather than accumulating more?

Fast forward to the present … or anti-POMO [where] it may be just a matter of time before the Fed’s liquidity absorption becomes the dominant force in the market.

Nomura notes, as I did long ago, that the worst drop in the stock market this year came immediately after the Fed first increased the rate of its Great Unwind to $20 billion a month. Tomorrow, the last day of the first half of summer, is when the Fed finally reconciles its books for July and completes it first month of $40 billion unwinding. And that is when I, too, have said the proverbial end-depositories hit the fan.

The most glaring episode was in late January/early February, which saw both the Fed’s MBS (mortgage-backed securities] and UST [Us treasuries] shrink over the last weekly period…. When there is a MBS or MBS/UST QT-unwind week, those periods on average see larger moves, in particular to the downside for broader risk assets…. The inference that the market is extra jittery on days when the Fed yanks tens of billions in liquidity is intuitive and a logical extension of the “POMO effect….” The first observation is that the majority of the weekly changes, or anti-POMOs, are sized between positive $5bn to negative $10bn. The second key finding is that there has only been one week of greater than $20bn reduction thus far – just days before the February VIXtermination event that sent the S&P on the verge of a 10% correction.

Well, guess what?

The next large QT-weekly reduction ironically enough is happening smack in the middle of this action-packed week, when on 1 Aug the Fed’s UST holdings will decline by $24bn.

That will be the largest Fed roll-off yet. And that is why I’ve said, “This is where it gets interesting.” Tomorrow the Fed closes its books on July, and the market gets to react. That is also the day by which I’ve bet my blog on the stock market’s crash. So far, we are in a market downswing that is notable to everyone because it is happening among the market’s long-time champions of the “Great Recovery,” and because it is happening for fundamental reasons of horrible reports by a couple of them, which have tarnished even those with good reports. How the market does on August 1 may depend a lot on Apple’s report after today’s market close. If a third out of five FAANG stock shows itself to been trouble, the market could become unhinged. If not, it may breathe a big sigh or relief.

Today, we have relief in the market as investors await the big Apple news. Let’s see tomorrow whether the downturn resumes in ernest or goes back up. In the meantime, enjoy today’s respite while you can, and have a mai tai for my sake. (Those still invested heavily in the stock market might want to hit up Laughable Larry for a little ether supply in case tomorrow moves in the direction I think it will.) In the meantime, enjoy what is left of the first half of summer.

*********

David Haggith started writing about the economy after he predicted The Great Recession half a year before it hit and was puzzled as to why no economists or stocks analysts saw it coming. In the months after the crisis broke out, he started to write humorous editorials in a series titled “Downtime,“ which chided the U.S. government and bankers who should have seen the economic collapse coming but whose cronyism, greed and ineptitude caused them to run the world into a ditch. Those articles were published in The Hudson Valley Business Journal, The Valley City Times-Record (North Dakota), and The Daily Herald in Tennessee. Haggith is dedicated to regularly criticizing the daily news — not just the content but the uncritical, unthinking nature of almost all of the reporting. He now writes his own blog, The Great Recession Blog, to break down the news as an equal-opportunity critic toward both Republicans and Democrats / Conservatives and Liberals … since neither kind of politician has done anything worthwhile to plot a better economic course. His articles are regularly carried by several economic websites.

More from Silver Phoenix 500