Powell Painted Into A Corner…Still

Though we just wrote about this last week, Tuesday's "emergency" fed funds rate cut demands that we write this update. Why? Because the bond market action in the hours since foreshadows even more cuts later this month, and this will have direct implications for gold, silver, and the U.S. dollar.

So let's begin with last week's link.

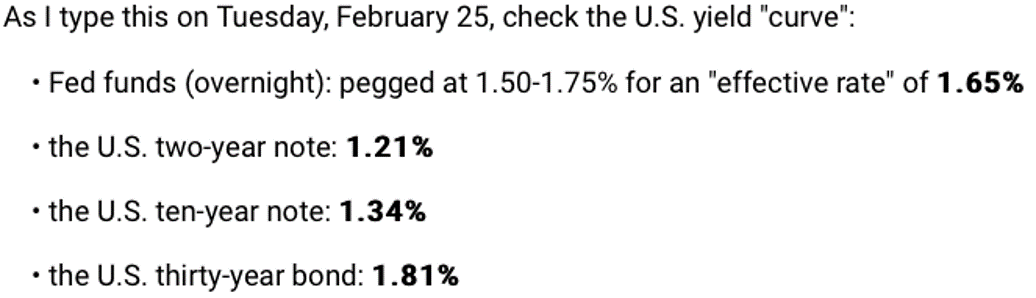

It was just eight (long) days ago that we explained for you WHY a fed funds rate cut was imminent. When that previous post was written, the yield curve in the U.S. looked like this:

As you're likely aware, yesterday (Tuesday, March 3) The Fed suddenly cut the fed funds rate in an attempt to bring it in line with changes in the bond market and provide added liquidity against an expected economic slowdown due to the worsening global coronavirus pandemic. In response, COMEX digital gold prices rallied over $50 and the U.S. dollar continued an eight-day plunge of nearly 3%.

But it was the action in the bond market that was the most noteworthy, and you must understand what this implies for Fed policy ahead of the next FOMC meeting in two weeks.

Below is the post-cut chart of the yield on the U.S. two-year Treasury note:

And check the post-cut reaction in the yield on the U.S. 10-year note:

So now the bond market has again painted Chairman Powell into an even deeper corner. Check the latest rates in the same format as posted last week and copied above:

• Fed funds (overnight): pegged at 1.00-1.25% for an "effective rate" of 1.15%

• the U.S. two-year note: 0.64%

• the U.S. ten-year note: 0.98%

• the U.S. thirty-year bond: 1.62%

As you can see, while The Fed sought to flatten and/or "un-invert" the yield curve through yesterday's emergency action, the movement in the bond market since has muted the impact, and today The Fed finds itself in nearly the same position it was in last week...namely, fully "behind the curve" and needing to cut rates again.

Absent any major selloff in bonds over the next two weeks (leading to higher rates), you can be certain that the FOMC will trim the fed funds rate by at least ANOTHER 25 basis points (0.25%) at their meeting on March 17-18. And this is very likely to have significant implications for precious metal prices in the weeks ahead.

Since the current pricing scheme still allows price to be determined by the heavily-margined trading of unbacked derivative contracts, the stated price of gold and silver will continue to be subject to sudden and sharp downdrafts, similar to what we witnessed last week. However, as long as Fed policy remains accommodative and the global trend continues toward zero (and perhaps negative) interest rates, even these digital derivative contracts will find a consistent bid on any dip.

We discussed our price projections for 2020 in this post from early January: https://www.sprottmoney.com/Blog/gold-and-silver-2...

Given the current state of the global markets—and the unexpected and unprecedented developments in the eight weeks since—we may have to update and post that 2020 forecast in the weeks ahead, too.

In the end, it is always prudent to accumulate physical gold and silver as a hedge against the madness of the global central bankers and politicians. Given the expected series of higher highs and higher lows in the months ahead, you should not delay any metal acquisition plans you have made for 2020 and beyond.

Craig Hemke, TF Metals

*********

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.

More from Silver Phoenix 500