Silver’s doubly-squeezed industrial and investment supply could drive prices above $100/oz this cycle

NEW YORK (September 11) In a strong bull market for precious metals, and at a time when gold is setting new all-time highs on a near-daily basis, silver still leads the yellow metal in 2025.

According to SilverStockInvestor’s Peter Krauth, while silver is definitely benefiting from the same rate cut optimism and inflation concerns that are propelling gold higher, it also enjoys a number of price drivers that gold lacks.

“I think that a lot of it is the same drivers as gold, and then I think the other half of what's driving it is something totally different from gold,” he told Kitco News in a recent interview. “And that is the scarcity aspect. You can argue gold is pretty scarce as well, but you don't have the same supply pressures as you have with silver.”

On the first point, Krauth said both gold and silver prices got a boost when the market started meaningfully pricing in the resumption of the Federal Reserve’s rate-cutting cycle.

“If you look at a chart, probably since at least August or even prior to that, we had that runup that went from $36 to let's say $38.40,” he said. “That was the market saying, ‘Okay, we really expect now that the Fed's going to cut rates in September.’”

Krauth said the Fed’s hand has been forced, and they are now in the position where they need to sacrifice inflation to preserve employment. “If you're going to cave in a situation where inflation is high and you're going to actually lower rates, then all bets are off,” he said. “On the macroeconomic side, I think that's really what's driving both silver and gold.”

But to the second point, silver also benefits from a supply deficit that can drive prices to outperform gold – even in an environment of burgeoning demand and unprecedented price levels for the yellow metal.

“It's accelerating and feeding on itself, this realization that this is an undersupplied market, already very tight,” he said. “We’ve seen supplies like identifiable secondary inventories fall significantly over the last four, four and a half years. I started saying early last year, probably February or March, ‘Look, the price hasn't moved significantly.’ Where are we at?”

“February of last year [silver] was $22. That has almost doubled since then.”

And while industry accounts for only a small fraction of gold demand, over half of the world’s silver supply is consumed by industrial applications. Krauth also believes that the market may have actually overestimated the pullback in industrial demand for silver as the solar buildout plateaus in China and subsidies end in the United States.

“The level of weakness that's expected in industrial has been overstated, and I think that we're going to be surprised by that once again,” he said. “One of the biggest drivers remains solar, and if we drill down a little bit, one of the aspects of solar that I think people are not considering enough is how the whole battery storage side of solar has really changed significantly.”

Krauth said AI data centers are increasingly including solar power generation in their plans now that battery storage prices are falling.

“They are [going with] solar because they can get it online very quickly, it's approved very quickly, it's contributing to their supply very quickly,” he said. “If you layer on top of that the whole battery aspect of it, the downside of solar without battery is that it would not be considered baseload because it's too variable.”

Affordable high-capacity battery technology eliminates this drawback from solar energy production. “You can store what you've produced during the day, and you can release that from batteries at night,” Krauth said.

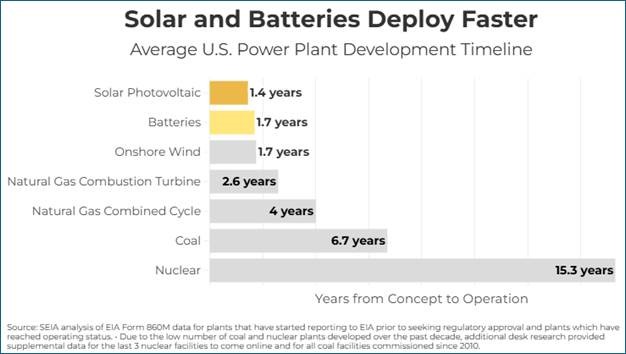

He pointed out that in the rapidly expanding AI and big data sector, photovoltaics make the most sense. “Solar and batteries deploy faster,” Krauth said. “The timeline [for nuclear] is 15.3 years from conception to operation. Solar is 1.4 years.”

And while the constraints on industrial supply have been well-documented, this year’s trade wars and tariff threats have introduced new constraints on silver's investment supply.

“The physical supplies remain tight,” he said. “We know that in the London market in particular, the liquidity's been dropping and lease rates have stayed above what they've been in recent years. We also know that a lot of the metal that left London when we had these tariff threats went to New York, and a lot of it has not gone back.”

“London, interestingly enough, is also where most of the silver for silver ETFs is stored,” he added. “80% of London stocks now are allocated to ETFs. That leaves only 20% available for either lending or for delivery.”

But the biggest catalyst for the gray metal’s recent breakout – and the most important medium-term driver for precious metals prices – is the Fed’s renewed dovish interest rate policy.

“The last three Fed rate-cutting cycles were early 2000s, and then 2008, and then 2020, and there was a pause in all three of them right around the middle,” he said. “When that pause ended, once they started cutting again to finish their cutting cycle, was when silver took off.”

“It's fair to assume that we are perhaps in the middle of the Fed rate-cutting cycle,” he said. “The forecast is for another 100 basis points to 125 or 150 basis points by September or October of next year. So that would point to potentially the U.S. being about halfway through.”

Krauth shared a chart that shows that in the last three cutting cycles, silver bottomed out halfway through the cycle, and when the cuts resumed, that’s when silver prices skyrocketed.

“[Silver] averaged 332% gains over the next 12 to 18 months,” he said. “Which is dramatic. If that were to happen from where we are now, let's say we started at $35 silver, then that's triple. We'd be over $100.”

“What's similar is that there has been a pause,” he added. “What's not similar is that silver did not bottom around the middle of that pause; it looks like it actually bottomed prior, close to when gold did, say late spring of last year.”

Krauth finished on a cautionary note for the near term, saying that silver prices may pull back in the near term once the September rate cut is delivered.

“A lot of this rate cut is being priced in right now,” he said. “Who knows, maybe silver will go to $42, $43. We may get some sort of a correction when the rate cut actually comes. That would not surprise me, a very classic ‘buy the rumor, sell the news.’”

That said, Krauth said that given all of the drivers supporting silver right now, this would constitute a buying opportunity.

“I think we could still see something like $45 for the end of this year,” he said. “And I think that $50 next year is probably quite likely.”

Silver continues to hold comfortably above $41 per ounce on Wednesday afternoon, with spot silver last trading at $41.128 for a gain of 0.62% on the daily chart.

KitcoNews