Can BTC Ever Be Money?

An examination of the Bitcoin phenomenon is timely, given that last Monday there was a widespread cryptocurrency $1.5bn crash, with Bitcoin losing nearly 3% in one day. Tellingly, this shake-out occurred at the same time as gold and silver rose strongly, tarnishing its monetary credentials.

Bitcoin is said to be a sound money alternative to debasing fiat currencies. But enthusiasts fail to understand the role of law, credit, and why stability of value is a prerequisite for a medium of exchange. This article ignores many Bitcoin issues, concentrating on monetary and legal practicalities.

The key issue is whether Bitcoin can be a future form of money. If so, then it could become the future anchor value for currencies and lower forms of credit. If not, then it is merely an ephemera, a latter-day tulipomania without even the backing of physical bulbs, a speculative mania liable to be punctured as the credit bubble deflates.

There are some important aspects of the Bitcoin phenomenon. There is the genius of a self-auditing blockchain coupled with an electronic mining system, which minimises counterparty risk. Once a Bitcoin is mined, in theory, it exists forever as an identified unit, capable of being transferred as a medium of exchange. But without the status of legal tender, can it ever truly be money? And will the blockchain allow the authorities to identify and confiscate Bitcoin on the basis that a previous owner bought and sold it to launder the proceeds of crime?

For most people, whether Bitcoin will become legal money or otherwise is immaterial. Fortunes have been made, the arithmetic of supply relative to fiat currencies is compelling, and investors believe they are onto a sure thing.

The logic behind Bitcoin is compelling: a fixed maximum supply of 21 million compares with government money printing at an accelerating rate towards infinity. It leads to comparing Bitcoin’s market capitalisation of $2.3 trillion with global credit outstanding of over $300 trillion and expanding. No wonder there are hopes that Bitcoin will go considerably higher.

For Bitcoin to be valued in this way assumes that it is actually money or will be when fiat currencies become worthless — a second assumption. Otherwise, it is no more than a paper derivative based on an intangible concept.

For Bitcoin to be a believable substitute for fiat currencies, there are major hurdles to surmount. The first is that it has no legal status nor a tradition of being a medium of exchange. This cannot be dismissed lightly, despite the anarchical chaos of collapsing fiat currencies foreseen by devotees. It also assumes that the electrical energy necessary for both mining and use as a medium of exchange will be freely available at all times, despite the economic chaos predicted.

However, even in monetary anarchy, both governments and their law-making will continue, both likely to become more repressive as economic and credit conditions deteriorate.

Alternatively, it is a huge leap of faith to argue that in the face of currency collapses, governments will admit their monetary failures and embrace a private sector alternative, particularly when it enriches its early promoters. More likely, they will try to shut it down and possibly even restrict gold in defiance of their own common laws in desperate attempts to maintain control over credit markets.

Furthermore, crypto promoters misunderstand the role of money. While every form of exchange media is credit, they come in two basic forms: metallic money without counterparty risk, accepted as such in the common laws of nearly all jurisdictions, with their roots in Roman law as final settlement. And then there is credit circulating nationally with counterparty risk, which is always settlement deferred. The former rarely circulates as a medium of exchange in modern economies, and the latter, in the form of currencies and bank credit, make up almost the entire circulating media.

For the value of currencies and bank credit to be stable requires them to be exchangeable for gold, and the final abandonment of the link between the two in 1971 is the source of circulating credit’s debasement, together with the inevitable demise of the fiat currency system.

The reason gold standards work is that, over time, gold’s value is stable relative to commodities and wholesale prices, and any currency readily exchangeable for gold acts as a gold substitute. In other words, so long as credible gold standards exist, currencies’ values vary little over time. The long-term value of savings is guaranteed, and businesses calculate their potential returns confident of their anticipated profits at the end of an investment project, as well as the true cost of any finance required, including its eventual repayment.

The ability of businessmen to calculate their prospective returns is fundamental to economic progress.

Therefore, the key to circulating media is a stability of value, which Bitcoin does not provide. Instead, Bitcoin would eliminate the expansion of credit linked to it because of the uncertainty of its value over time. A lack of understanding of the relationship between a monetary anchor without counterparty risk and credit is behind assumptions that Bitcoin can replace fiat currencies as a common exchange medium.

An economy based on Bitcoin without derivative credit would simply regress to medieval times, when the only acceptable payment was physical coin. The mistake Bitcoin promoters make is to believe that any expansion of credit is bad. That is not so. Bank credit conjured out of thin air and deployed productively does not undermine a currency. It is governments which are the problem. They require the discipline gold gives to always ensure that they hold sufficient gold reserves to meet currency redemptions.

If BTC cannot be money, what is it?

Clearly, if Bitcoin is not and never can be money in the accepted sense, then it is nothing. It is not even overpriced tulip bulbs, though there may be some uses for the blockchain concept. And even that, after the initial excitement, turns out to be a disappointment.

Regulations forced on crypto brokers have done much to sanitise the industry. But there are still many quacks using promotional methods which are downright dishonest. However, responding to public demand and potential profitability, Bitcoin trading has begun to go mainstream, with ETFs and other derivatives being marketed by establishment banks.

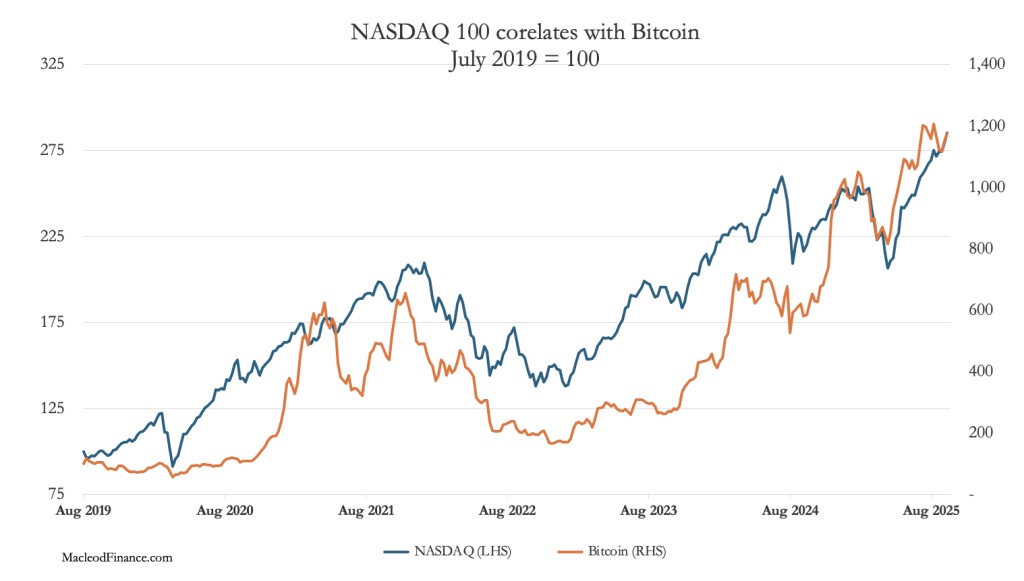

Undoubtedly, there is a heavy tech influence behind the industry. And just as soaring technology stocks have reflected easy credit conditions, there is little doubt that there is a correlation between the tech sector and Bitcoin, reflected in the chart below:

While correlation isn’t everything, the evidence is that instead of a future money Bitcoin is behaving like a tech stock. Compared with the Magnificent Seven, the correlation is even clearer. The next chart compares the performance of Bitcoin (the faint line) with CNBC’s Magnificent 7 Index over the last 3 months.

Allowing for volatility, the majority of rises and falls all occur together. Clearly, if tech stocks fall, Bitcoin will fall with them. Bitcoin appears to be a tech stock without business risks, but no assets and no earnings either. Furthermore, in light of its recent loss of momentum, it is beginning to underperform its tech peers.

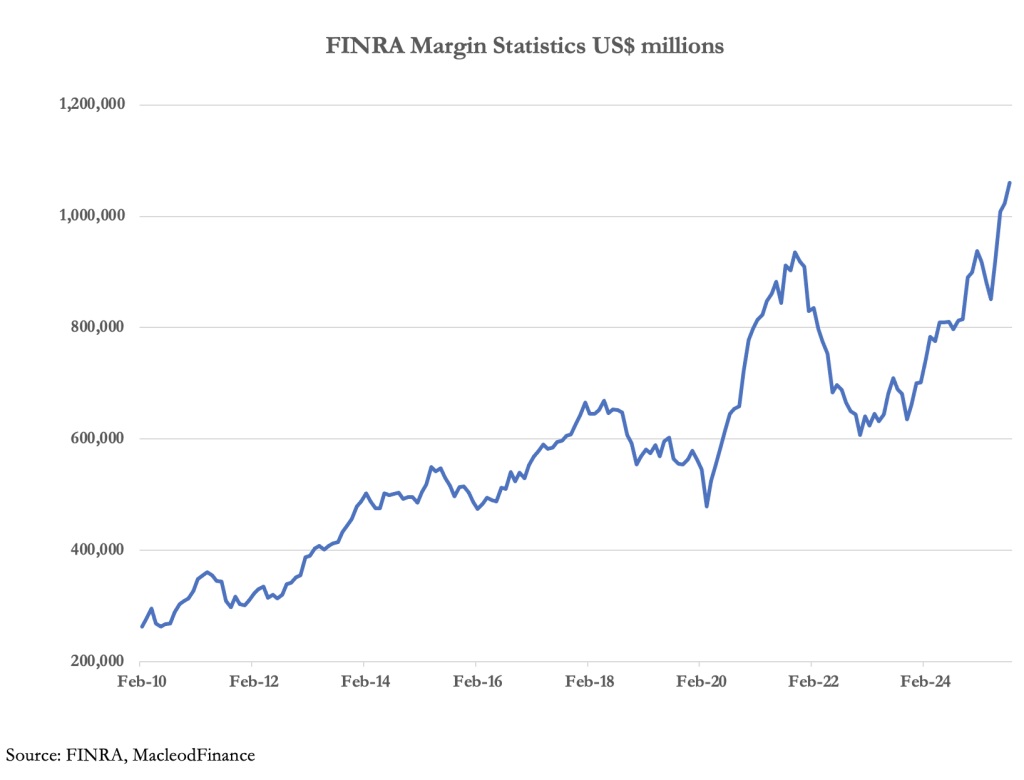

This is the polar opposite of what Bitcoin investors expect. They look for the credit bubble to drive the relationship between fiat currencies and Bitcoin, with Bitcoin rising priced in fiat. But an expansion of government credit from here will almost certainly drive interest rates higher as debt becomes increasingly unsustainable, undermining stock values. In this context, the persistence of bullish leverage in the market, particularly in tech stocks, is also concerning:

Higher bond yields and weakening currencies threaten the eventual collapse of the debt-cum-credit bubble, which has happened often enough in the past following credit expansions to be undeniable. Margin levels are at record levels, which suggest that NASDAQ and the Magnificent 7 have significant downside as margins are called in. How Bitcoin performs in these circumstances will be its true test.

********