Key factors for investors seeking relative value in precious metals in 2026 – CME Group’s Norland

NEW YORK (January 15) While there are a number of ongoing drivers supporting further price gains for gold, silver, platinum and palladium this year, each have key factors that could strengthen or weaken their prospects against the rest – even as the interest rate and inflation picture will impact the entire precious metals complex, according to Erik Norland, Managing Director and Chief Economist at CME Group.

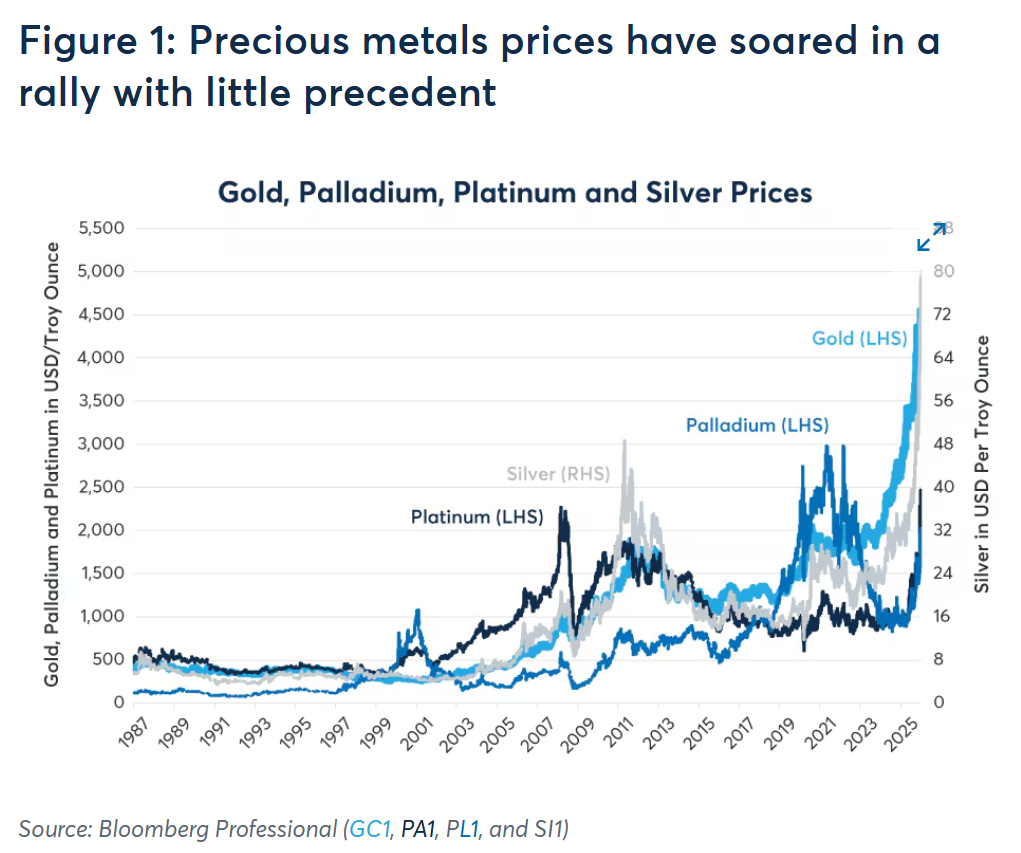

“The surge in the prices of precious metals in late 2025 has continued into the early days of 2026, with gold surpassing $4,500 an ounce, silver rising past $80 per ounce and platinum hitting its first record highs since 2007,” Norland wrote. “Palladium prices have also rallied sharply, although they remain far from record highs.”

“In terms of price returns, metals have far outshined any other asset class since the end of 2024 with gains of 65% for gold, 95% for palladium, 150% for platinum and 170% for silver as of January 6,” he noted. “Gold’s relative underperformance probably has a lot to do with the yellow metal’s gains outpacing those of the other metals to such a great extent between 2000 and the end of 2024. During those first five years of the 2020s, gold gained 73%, silver rose by 63% while platinum and palladium prices fell by 8% and 52%, respectively.”

“To some extent, the recent outperformance of silver, platinum and palladium may reflect their playing catch up after a long period of relative underperformance,” he added.

Norland sets out to analyze the relative values of these precious metals, with an eye toward identifying which are most likely to outperform in 2026 and beyond.

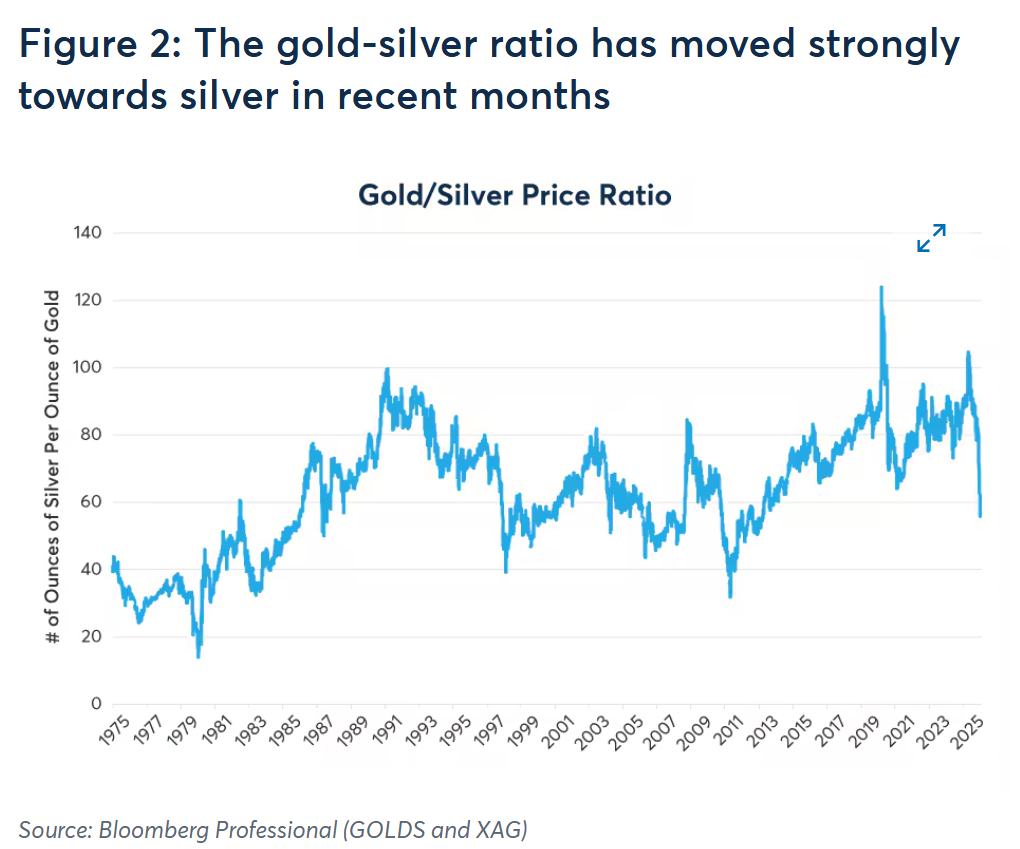

He begins with the two most often benchmarked against one another: silver and gold. “It’s getting harder to argue that silver is still cheap relative to gold,” he wrote. “The gold-silver price ratio (the number of ounces of silver one could buy for one ounce of gold), has fallen to its lowest level since 2013.”

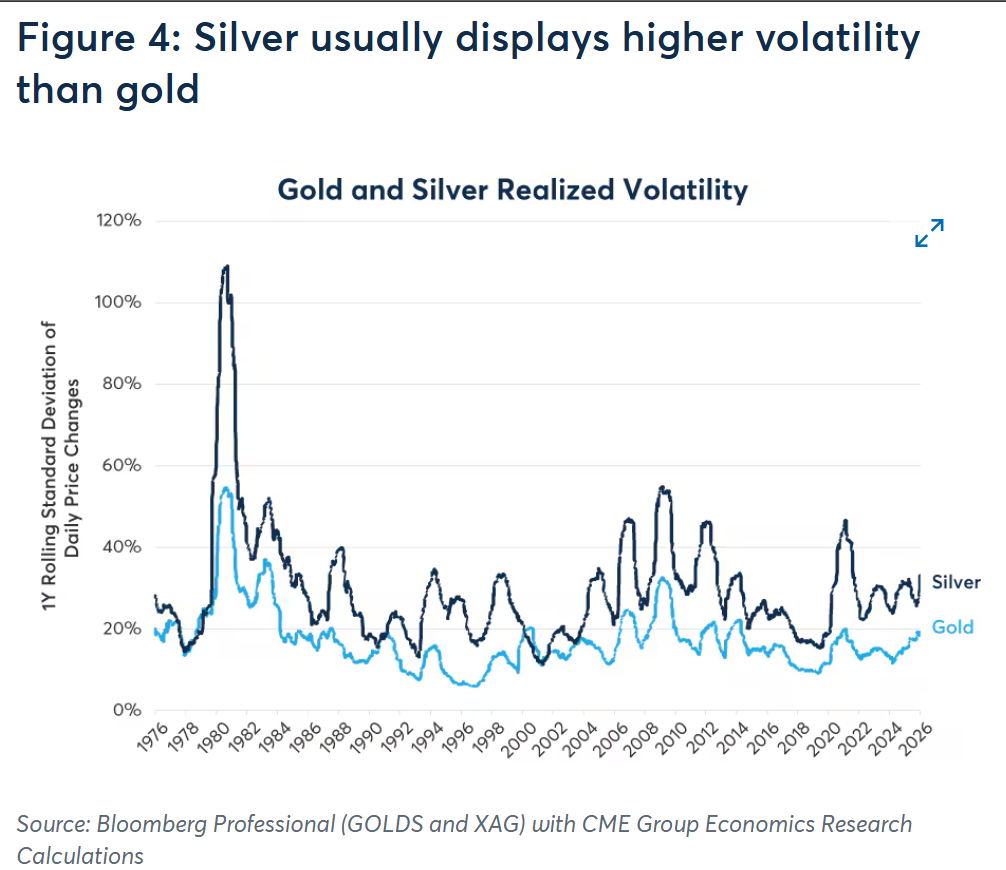

Norland noted that some of silver’s gains likely reflect its ‘high beta’ versus gold. “Silver and gold are deeply connected via the jewelry and investment markets and silver’s high beta results from it being a much smaller market which often amplifies its moves,” he said. “ Silver is both highly correlated with gold and typically more volatile (Figures 3 and 4). As such, up and down moves in gold tend to be reflected in silver to an even greater extent.”

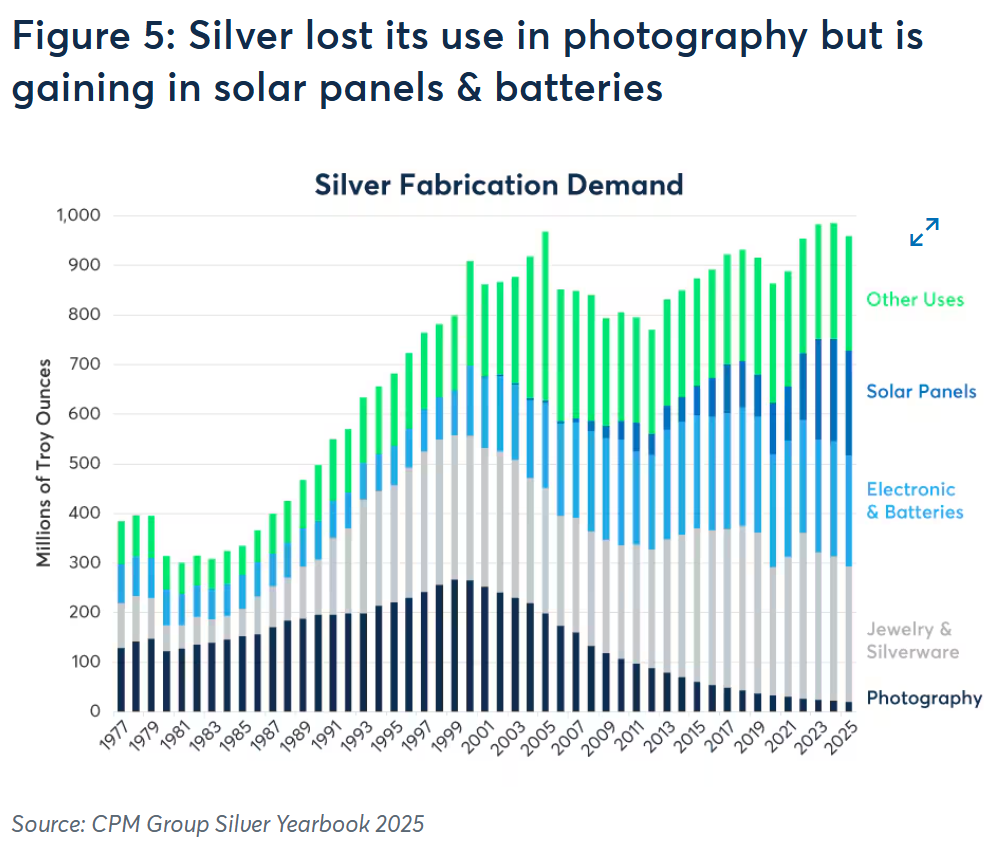

He warned, however, that there’s more to the gold-silver story than correlation and relative volatility. “Silver underperformed for much of the century because of the shift to digital photography which largely eliminated the need to develop photographs on silver plates, an activity that consumed one quarter of the world’s silver output in 2000,” he wrote. “In recent years, however, silver has found new sources of demand, including in batteries and solar panels, which appear to be driving the gold-silver ratio back in silver’s favor.”

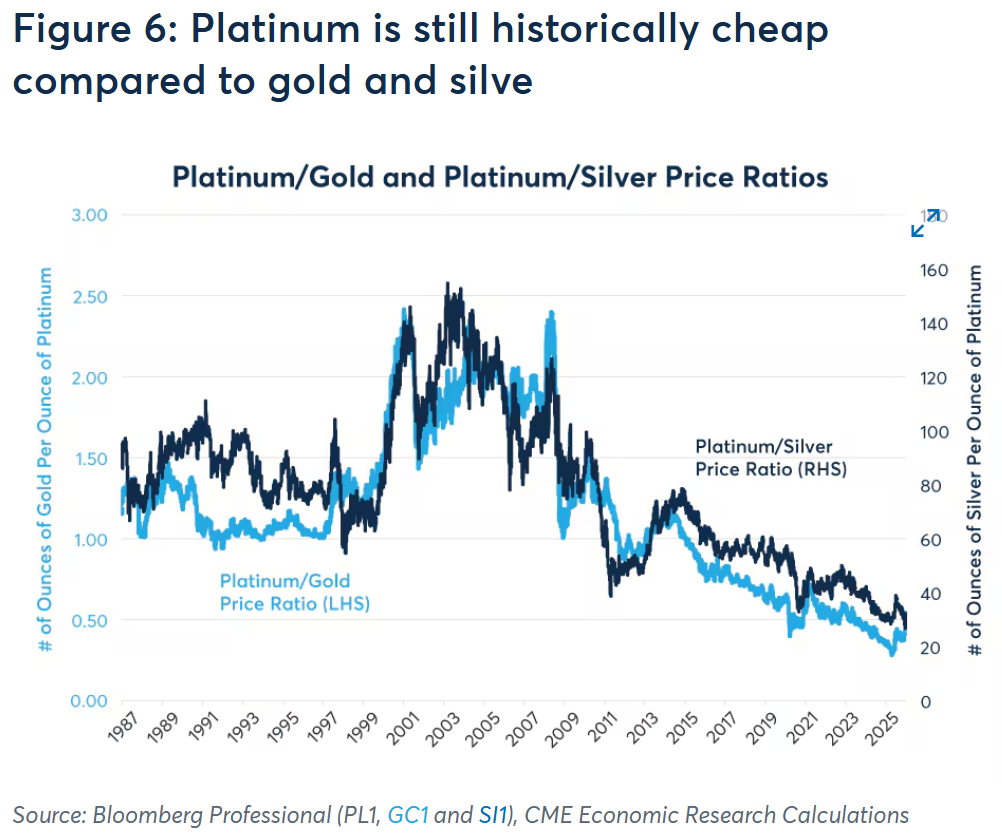

Next, Norland looks at gold and silver in relation to platinum and palladium, noting that “despite its recent rally, platinum remains historically inexpensive relative to gold and silver.”

“Back in 2007, when platinum hit a record high, it was nearly 2.5x as expensive as gold,” he said. “That has changed. As of early January, gold is close to 2x as expensive as platinum.”

Norland said a large proportion of platinum’s underperformance is due to decreased demand for diesel vehicles, resulting in less need for platinum catalytic converters.

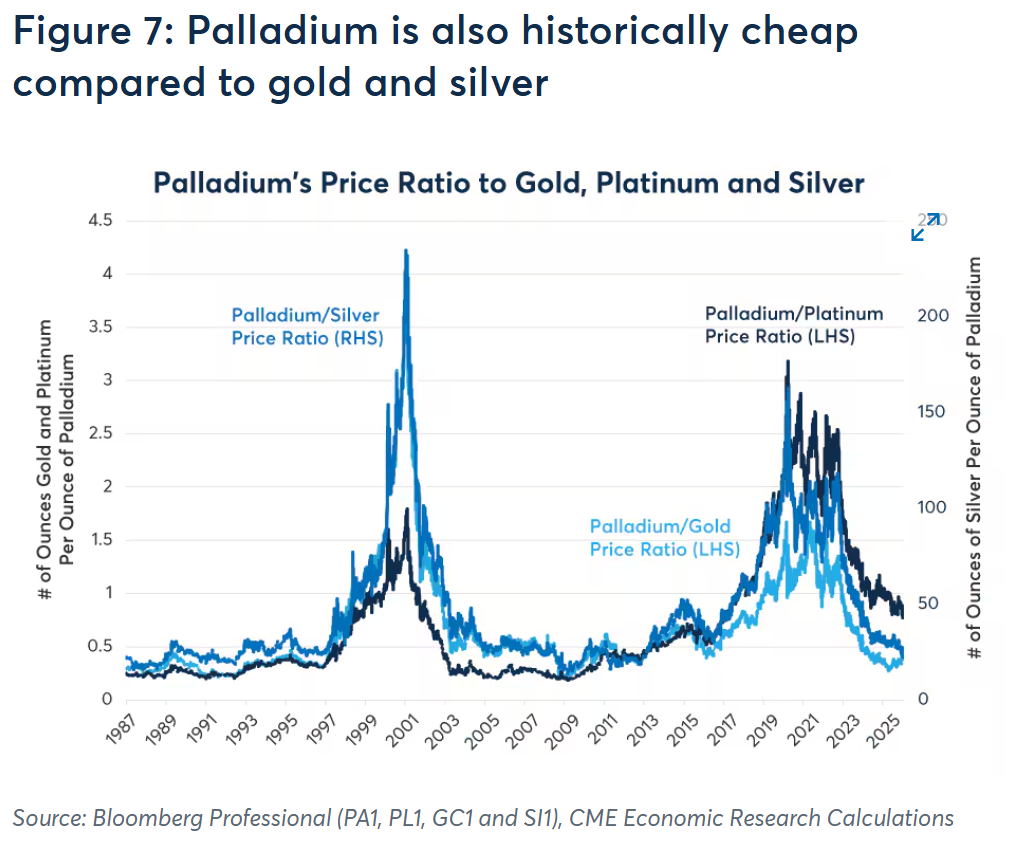

“Palladium’s two historic price spikes relative to the other metals came after periods of supply constraints, but prices have returned close to historic lows versus gold and silver,” he noted. “Palladium demand, too, has begun to erode as EVs have gained market share across the world in recent years. That said, EV sales could slide in 2026 as many countries, including China and the U.S., have curtailed subsidies.”

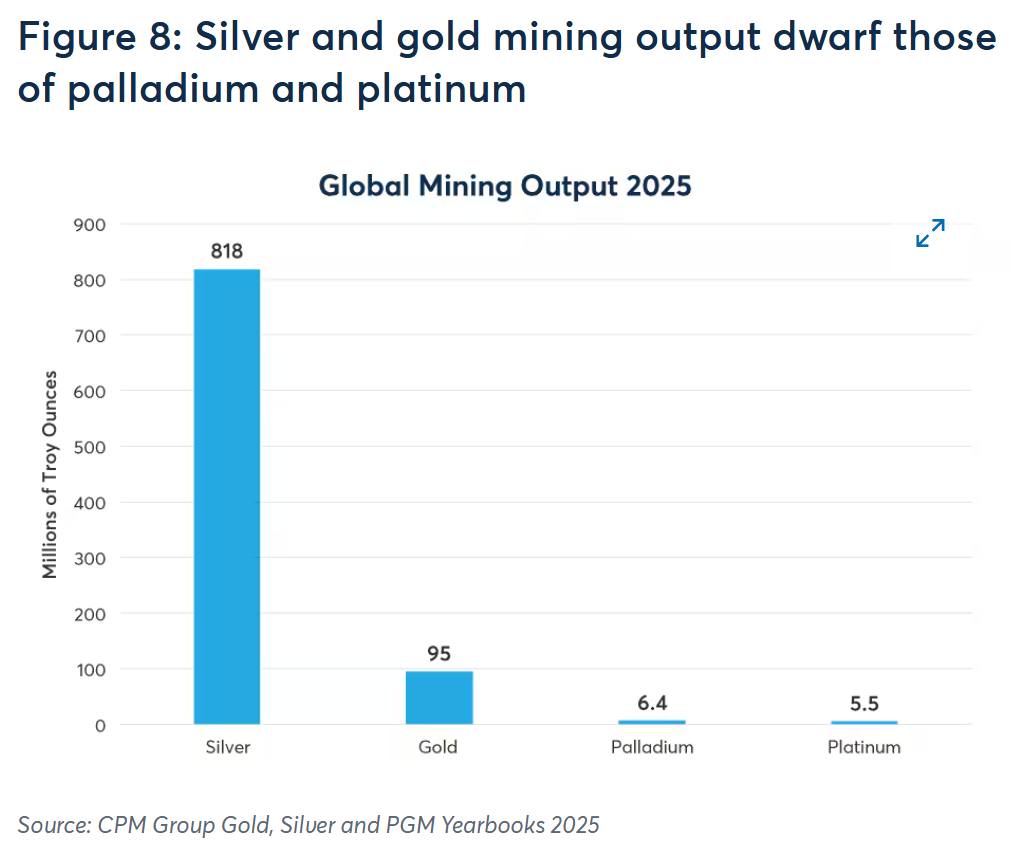

Norland said investors looking to diversify beyond gold could easily gravitate toward silver, platinum and palladium. “However, there is one last point to consider, which is the relative size of the markets,” he cautioned. “In 2025, the world’s miners extracted 818 million troy ounces of silver, 95 million of gold, 6.4 million of palladium and 5.5 million of platinum (Figure 8). But mining supply doesn’t by itself tell us about the relative size of the markets.”

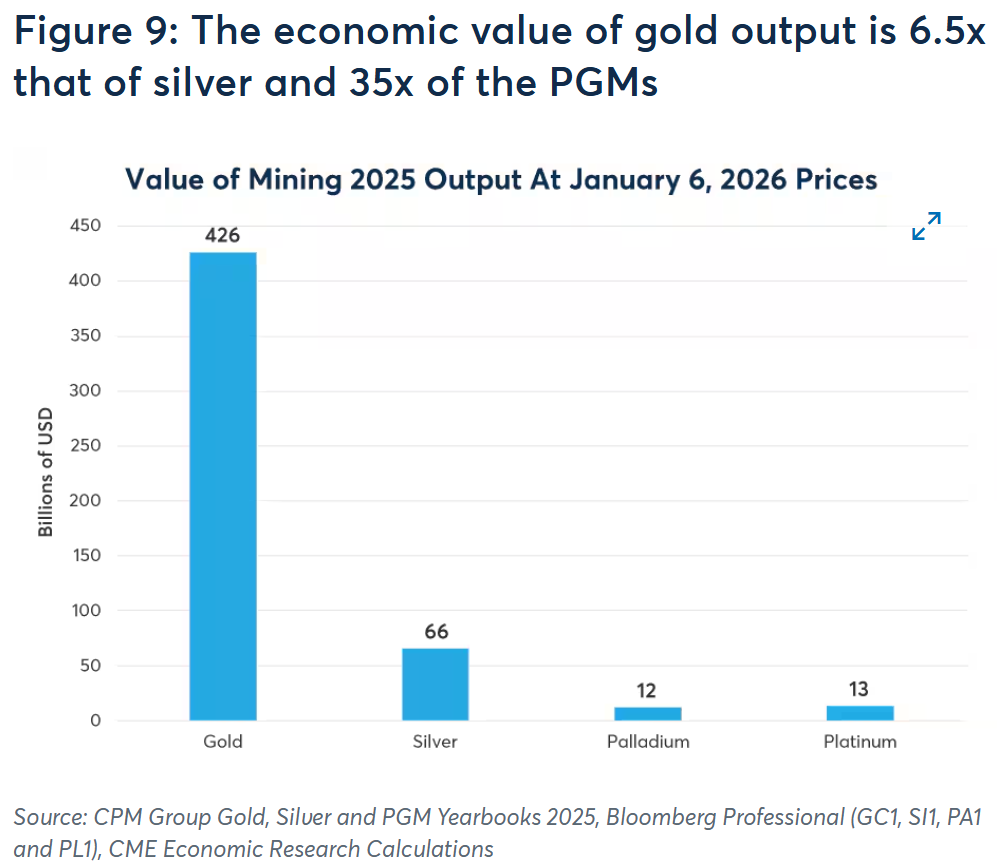

“Valuing the metals at early January 2026 prices, the value of gold mining output exceeds that of silver by roughly 6.5x and that of platinum and palladium by around 35x,” he noted. “As such, even if a small portion of gold investors choose to diversify into silver, platinum and palladium, their investment decisions could drive their prices in U.S. dollars (USD), and their price ratios relative to gold higher. This makes the macro picture driving the precious metals rally especially important even for relative value investors.”

Norland then looks at various ways the macro picture might evolve in 2026. “There appear to have been several macro factors driving gold prices higher in recent years, which subsequently spilled over into other precious metals markets,” he said.

These include core inflation remaining above central bank targets nearly everywhere, most central banks (excluding Brazil and Japan) continuing to cut rates anyway, large budget deficits in major economies, and changes in the geopolitical environment.

“As such, investors should watch core inflation rates closely,” he warned. “If they remain above target or rise further and central banks don’t respond with policy tightening, investors could construe this as an argument to continue increasing their portfolio allocations to these metals. By contrast, if core inflation eases, investor concern about inflation could abate, weakening demand for precious metals.

“The same could be true if central banks reverse course and raise rates,” he added. “No central bank is of greater importance than the U.S. Federal Reserve (Fed), and with the Fed undergoing a leadership change in May 2026, investors will likely scrutinize its actions closely.”

And while monetary policy and core inflation are very uncertain, Norland said the direction of global fiscal policy is much clearer. “Brazil, China, France, Russia, Saudi Arabia, the U.K. and U.S. are running large budget deficits, and none of them are taking meaningful actions to rein in the size of their deficits,” he said. “Moreover, other countries including Germany and Japan are loosening their fiscal stance to boost military spending, and in Germany’s case, investment in public infrastructure. As such, it seems that fiscal postures will likely remain supportive for precious metals in 2026.”

The final key piece of the puzzle is geopolitics. “If geopolitical concerns intensify, they could further boost gold prices, and by extension the prices of other metals,” he said. “By contrast, if investors see the geopolitical situation as stabilizing, this could lead to some money flowing out of precious metals and into fiat currencies.”

KitcoNews