Silver could outgain gold again in 2026, but may face some early headwinds

NEW YORK (December 26) Silver benefited from strong industrial and investment demand in 2025 – along with tariff fears which dislocated physical supplies like never before – driving prices over 120% higher this year. Looking ahead, investment banks, institutions and leading analysts believe the gray metal can move much higher next year, though it will likely face some early setbacks in 2025.

Analysts at Heraeus warned in their 2026 Precious Metals Outlook that silver and other precious metal prices will likely trend lower for at least the first part of 2026.

“The rally that has seen gold and silver at record highs and PGM prices at their highest level in years, took prices too high too quickly,” they said. “While prices could push higher in the near-term, once the momentum wanes a period of consolidation is likely.”

“The high price is denting silver demand in a number of sectors,” they added, “but if gold moves higher, silver is likely to follow.”

Heraeus believes a number of silver demand sectors will struggle in 2026. They project photovoltaic silver demand will decline in 2026 as thrifting outweighs installation growth.

“After several years of significant growth, photovoltaic (PV) installation growth is predicted to slow to about 1% in 2026 following policy changes in China, the largest market,” they said. “At the same time, the high silver price has reinvigorated efforts to thrift silver in PV systems. This is occurring on a number of fronts, including printing finer contacts, changes in the cell design and by attempting to use cheaper metals. Other industrial demand tends to grow broadly in line with the growth in the global economy, which is muddling through with modest growth despite the US tariffs that have complicated the trade outlook.”

Like gold, high silver prices have dampened jewelry and silverware demand, and Heraeus expects this will continue in 2026. “India accounts for about 40% of global silver jewellery demand and around two-thirds of the silverware market, and consumers have been unable to afford as much silver as the price has climbed,” they said. “The country imported 14% less silver in the year to October year-on-year.”

The analysts also expect higher silver prices to drive recycling rates up. “Even if the silver price slides from its current level, the average price in 2026 is likely to be higher than in 2025 and higher prices tend to encourage greater recycling,” they wrote. “Most silver is produced as a by-product at gold, copper and lead/zinc mines. Mine output for each of these metals is expected to expand modestly in 2026, suggesting that silver output is also likely to rise.”

“Demand growth in 2026 could be reliant on investment, with declines anticipated in silverware, jewellery, photographic and photovoltaic demand, and lackluster industrial demand,” they predicted. “That said, strong investment interest in silver is not a given as it has been variable in 2025. The rising price has a dampening effect on coin sales, which are priced at a premium to bars and are bought as much for collectability as investment. Bar demand has varied depending on the country, with retail investors in India, in particular, enthusiastically buying as the price rallied. ETF holdings rose by 17%, from 716 moz at the start of the year to 835 moz in October, before some profit-taking set in.”

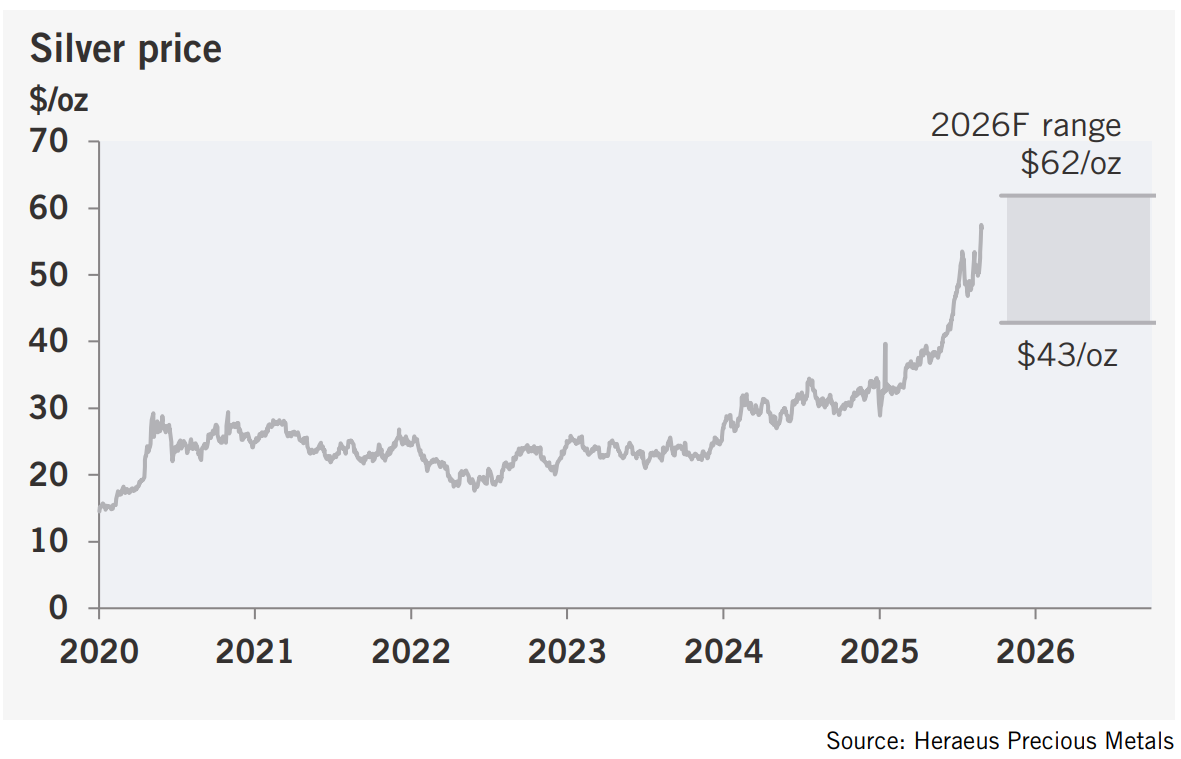

Heraeus forecasts the silver price to trade between $43 and $62 per ounce in 2026. “Ultimately, silver is a higher beta, i.e. more volatile, investment than gold,” the analysts said. “The drivers of the gold price, namely, economic and geopolitical concerns, US fiscal and monetary policy, central banks cutting interest rates, and their impact on the US dollar, will also influence the silver price. If gold’s rally resumes, then silver is likely to follow.”

Commodity analysts at TD Securities wrote in their 2026 outlook that they expect silver prices to moderate to the mid-$40s during the year to come.

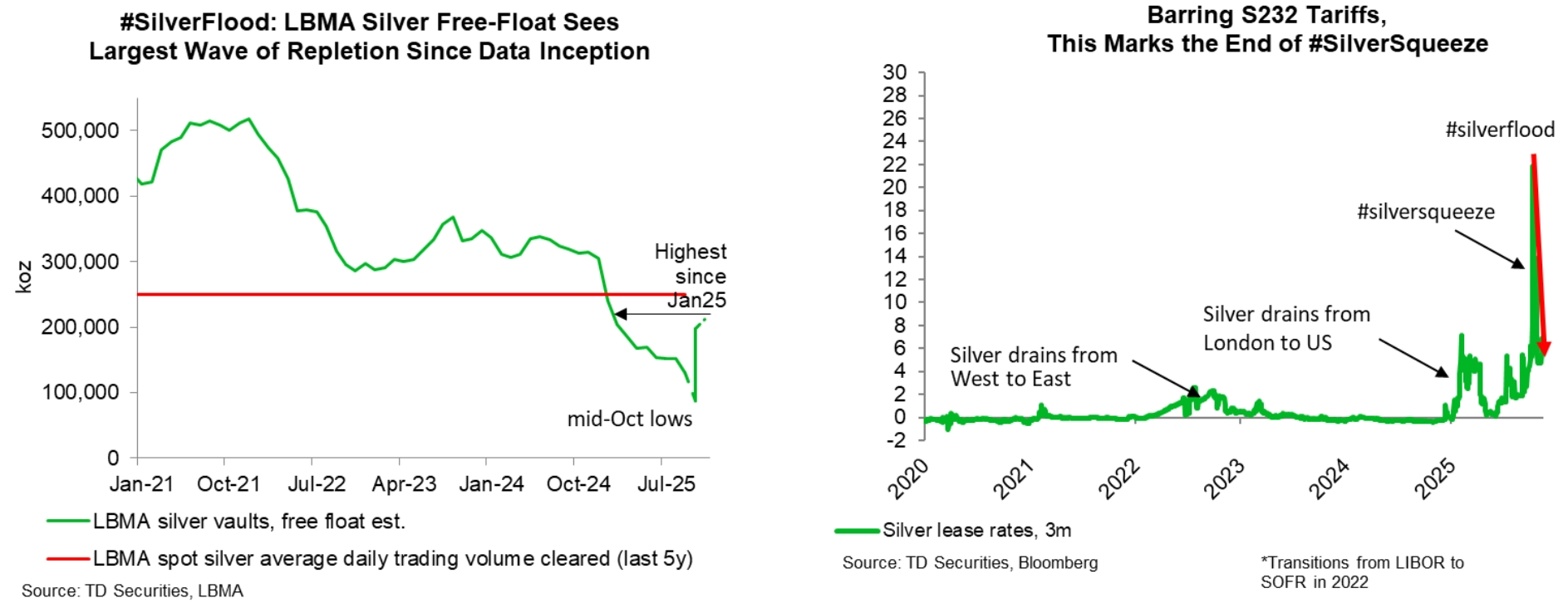

The analysts said that if you liked the #silversqueeze, you have to like the #silverflood.

“At the start of this year, the market was sleepwalking into a #silversqueeze, even as the set-up transitioned away from a demand boom towards a liquidity crisis in physical markets,” they wrote. “Heading into 2026, an epic-scaled #silverflood has resulted in the single largest wave of repletion in LBMA free-floating inventories on record. With more than 212mn oz of silver now likely freely-available in the LBMA's vaults, London silver markets have already unwound a year's worth of drain in London inventories.”

“This amount covers nearly two years' worth of global deficits, with evidence that we have reached the strike price necessary to open the taps from scrap and private vaults,” they added.

The analysts said this massive replenishment should have a big impact on the outlook for silver because the price no longer needs to rise to refill global inventory pools.

“Yet, prices haven't collapsed post #silverflood,” they noted. “Lease rates have collapsed from historic levels, but prices haven't. Prices have only traded violently near ATHs, clashing with a statistically significant relationship between commodity vol and inventories.”

They pointed out, however, that since the end of the silver squeeze, spot silver trading volumes have fallen dramatically by over 65% from their October highs, “potentially fueling a liquidity vacuum which has left precious metals markets vulnerable to gamma hedging flows.”

“This is corroborated by ETF vols now trading more expensive than Comex vols, reversing a post-Covid trend and potentially signaling that speculative demand has increased substantially beyond that of basis trades over the last months,” the analysts warned. “Further, 3m call skews on popular silver ETFs are now trading at their highest levels since the original retail #silversqueeze moment in 2022Q1, which preceded a severe drawdown in prices.”

The analysts also said that tight Shanghai exchange inventories “are a function, not a symptom, of the #silverflood, as Shanghai has emerged as a backstop to London over the last months.”

“Case in point: the Shanghai import arb window remains firmly closed,” they noted. “Considering invisible stocks within China are likely multiples larger than those on-exchange, tightness in Shanghai will be self-resolving amid incentives to return metal on-exchange.”

TD believes this will end the current chapter of the silver squeeze. “The next chapter in the #silversqueeze saga will necessitate (1) a more significant erosion of above-ground inventories in Shanghai and New York, or (2) forms of export controls that could inhibit rebalancing mechanisms, including section 232 tariffs, or more stringent export controls in China,” they said. “Liquidity has returned to London, which represents a correction risk from the late-November highs.”

However, the analysts do not expect any tariffs on silver as a repricing catalyst. “The stockpiling trend has already run its course, they wrote. “The President must now make a determination regarding the Section 232 critical minerals investigation by mid-January. Barring tariffs on silver, silver markets are facing rising global visible inventories, a significant deterioration in industrial demand (-2% y/y), including from solar cells (-5%) despite rising aggregate solar capacity, jewelry (-4%), silverware (-11%) and even global physical investment (-4%). At the same time, silver's debasement-hedging properties pale in comparison to gold's, suggesting that even an unlikely scenario of forced/quick-debasement, silver will underperform gold.”

TD Securities expects silver prices to start the year in decline, averaging $42 per ounce in the first quarter, and they say the gray metal will be hard pressed to get back to current levels in 2026. “Hence, our mid-$40s projection next year.”

Commodity analysts at BMO Capital Markets said in their official 2026 outlook that there is room for precious metals to run higher in 2026 – though silver may not be able to hold onto its current all-time highs.

The bank sees silver prices averaging around $60 an ounce in the fourth quarter of 2026, which they expect will represent the high for the year. BMO sees silver prices averaging $56.3 an ounce for the year as a whole. The updated outlook comes as silver prices are currently trading above $65 an ounce.

“One of the most significant upgrades we have made this quarter has been to our silver price, which we have raised by 14% to $56.3/oz for 2026,” the analysts said. “Investors have shown a greater affinity towards silver than we had expected, likely being swept up in the debasement trade as well U.S. stock building in light of its recent ‘critical mineral’ designation.”

BMO analysts said that while they believe gold’s multi-year rally can continue in 2026, “we have turned more cautious on other precious metals like silver and platinum in comparison, which are showing signs of being over-bought in recent weeks,” they wrote.

“These metals will happily trade like gold when in a market deficit (and can even offer significantly more torque during price rallies, as we have seen this year); however, our latest updated models suggest the deficits for these metals are narrowing.”

Maria Smirnova, Managing Partner at Sprott Inc. and Senior Portfolio Manager & Chief Investment Officer at Sprott Asset Management, told Kitco News in December that the supply problems which have plagued the silver market in 2025 remain unresolved, and surging investment demand has only exacerbated physical shortages where they’re most needed – setting the stage for further gains in 2026.

Smirnova said the shift in the physical shortages from London to Shanghai is significant, because while the investment demand may be centered in the UK and U.S., the metal is actually being consumed in China.

“In my mind, it's more important to look at solar, because that's where the panels are made,” she said. “Solar consumes over 200 million [ounces], or about 20% of supply. So, if we're saying in China that the inventories are out, that's very significant, because that's where the metal needs to go.”

And Smirnova said the ramping up of investment demand is happening while the physical supplies are as thin and as dislocated as they’ve been in many years.

“On the ETF side, from January until now we've had over a hundred million ounces go into the Western ETFs, at least what's tracked on Bloomberg,” she said. “Again, that's a big amount of silver.”

“I'll give you how I think about it: a big silver mine is between 10 and 20 million ounces of silver,” she added. “There's not that many mines like that, and we've not had new mines like that at all, really. And in the last 10 years, we've lost 80 million [ounces] of supply from mining. That's a handful of big mines that we need to replace.”

Meanwhile, other industry changes that occurred while silver prices languished are also negatively impacting present and future supply. Smirnova said that many silver companies focused on buying gold assets when the silver price was low. Now, the major players are being forced to scramble to acquire silver mines.

“In this calendar year, we've had three or four M&A transactions where now the companies are trying to buy silver deposits and silver mines, but there's a shortage of them,” she said. “There's not many good assets in the space.”

“It will take time to permit these things, to finance them and build them,” she added. “In my mind, it's a five-to-10-year process; it's not an immediate fix.”

“After five to seven years of deficits, we're finally seeing the effects of that translate into price movement.”

Going forward, Smirnova said silver’s supply dynamics – and its future price action – depend in large part on whether China is able to import silver to fulfill their industrial needs.

“Who’s the marginal seller at this point?” she asked. “Is it still London, or is it going to start moving from the COMEX now? And how much is available? Or are the investors going to empty the Swiss vaults all of a sudden? And do people sell their silver at $60?”

For all these reasons – and even at these all-time-high prices – Smirnova said Sprott remains bullish on silver in the medium term.

Michele Schneider, Chief Market Strategist at MarketGauge, told Kitco News that she remains significantly bullish on silver as the metal remains undervalued and the market continues to be driven by strong fundamental demand.

“It’s amazing that silver prices are not trading a lot higher right now,” she said. “Supply deficits have become a significant concern. Demand is only going to grow, but supply remains extremely limited.”

Schneider noted that tech companies are projected to spend $700 billion in capex as they build out the growing AI infrastructure, but that can’t happen if there isn’t enough silver.

She also views silver as a value play in the precious metals market. Although silver prices have pushed well above $60 an ounce, Schneider said it is still undervalued compared to gold.

The historical average of the gold/silver ratio is between 50 and 60 points, but she noted that back in the 1970s, the ratio was trading around 20 points. In the current environment, Schneider said she could see the ratio bottoming out at 40 points.

“Looking at the price of silver relative to the price of everything else, it is still pretty cheap,” she said. “The ratio can go a lot lower than it is right now and that means much higher silver prices.”

Ultimately, Schneider sees silver prices hitting $75 an ounce in 2026, and she sees any consolidation or drop in price as a buying opportunity.

Turning to industrial demand, the latest report from the Silver Institute noted that the gray metal will continue to play a critical role in the electrification of the global economy, which will support demand through 2026 and beyond.

“Sectors such as solar energy (PV), automotive electric vehicles (EVs) and their infrastructure, and data centers and artificial intelligence (AI) will drive industrial demand higher through 2030,” they said.

According to the report, silver demand in the solar sector remains the biggest driver within the industrial segment. In 2014, the solar sector represented about 11% of silver demand, but a decade later, it now accounts for 29%.

“Although the global trajectory of PV installations remains strong, technological developments have reduced the amount of silver required in some PV cells,” they wrote. “The loss of government subsidies and incentives in certain countries, however, is likely to be offset by ambitious targets in others. For example, the European Union aims to deliver at least 700 gigawatts of solar capacity by 2030, which will assist in silver consumption.”

The growing electric vehicle market is the second-largest source of industrial silver consumption. The report forecasts global automotive silver demand to increase at a compound annual growth rate of 3.4% between 2025 and 2031.

“EVs require significantly more silver than traditional internal combustion vehicles (ICEs), with silver used in various applications, including battery management systems, power electronics, charging infrastructure, and electrical contacts. The shift from internal combustion engine vehicles to EVs is expected to boost silver demand significantly; EVs, especially battery-electric vehicles, consume, on average, 67–79% more silver than ICE vehicles, with approximately 25–50 grams of silver per EV,” the report said.

The final source of industrial growth in silver is expected to come from the evolving AI economy, as more data centers are required to support increased computing power.

The report estimates that total global information technology (IT) power capacity increased by approximately 53 times, from 0.93 gigawatts in 2000 to nearly 50 gigawatts in 2025.

“Even in the absence of precise silver-loading data, the link is clear: a 5,252% increase in IT power demand translates into more computing hardware and, consequently, greater demand for silver,” the analysts said. “As AI applications diversify into media production, design, and simulation, demand for servers’ processing power and, by extension, data center infrastructure is expected to continue growing.”

The Silver Institute said they expect industrial demand to keep silver prices well supported in a long-term uptrend.

And on the supplier side, John Feneck, Founder and CEO of the Feneck Commodities Report, told Kitco Mining’s Digging Deep following the Federal Reserve’s December rate cut that silver’s breakout remains one of the defining moves of the year, and silver mining equities should see further gains in 2026.

When asked whether silver stocks are entering a stratospheric phase, Feneck responded, “They already have.” He pointed to developers and explorers that continue to trade below intrinsic value despite strong gains and said thin liquidity is amplifying upside moves as investors reposition ahead of 2026.

“There's going to be so many of these juniors that are going to make headlines in 2026 and 2027,” he said, adding that companies with scale, strong jurisdictions, or near-term production potential are positioned to benefit most.

Consolidation is accelerating across the sector, with Feneck noting the Dec. 8 merger between Contango ORE and Dolly Varden Silver, reflecting a broader move by developers to combine cash flow with district-scale exploration upside. He said producers are likely to pursue more M&A in 2026 as they look to secure future ounces and reduce permitting uncertainty.

Avi Gilburt, veteran technical analyst and founder of ElliottWaveTrader, believes the surge in gold and silver prices is entering its final stages. In a recent interview with Kitco News, he warned that investors should begin preparing for a multi-year correction that may begin in 2026.

“I believe we are heading into the end of the cycle,” he said. “2026 probably will provide us with the end of this long-term cycle in gold and silver, and potentially kick off another multi-year bear market.”

Gilburt said silver has already hit the minimum threshold of his long-term targets, but as long as support holds, the rally still has room to run.

“I don’t think we’re done yet,” he said. “My ideal target was about $75 to $80.”

Whether silver reaches that zone will depend heavily on how the market behaves into year-end, Gilburt said, as a controlled pullback toward the $43–$47 range could provide the technical structure needed for a final blow-off rally.

“If we get to $75 to $80, that could represent the final blow-off top.”

This parabolic move would mirror silver’s 2010–2011 fractal pattern — a comparison that prompted Gilburt to turn bullish earlier this year when the current rally began accelerating.

He said the coming months could offer one last opportunity to participate in the upside of the metals bull market – particularly in silver. Later in 2026, however, the risk-reward balance may look very different.

“This information gives people time to protect themselves,” Gilburt said. “Narratives can really hurt an investment account.”

And Kitco’s Jim Wyckoff wrote in his newly-released 2026 Technical Outlook for Silver that December Comex silver futures set yet another all-time record high of $67.38 on Friday, and the gray metal is set to end 2025 at more than double its 2024 closing price of $29.29.

“While the silver market in 2026 is forecast to remain strong, driven by soaring industrial demand and tightening supplies, it’s doubtful the new year will see the 130% price gain for silver that was seen in 2025,” he cautioned. “Still, more than a few metals analysts predicting silver prices could reach or exceed $75.00.to $100.00 an ounce in the new year. Specifically, silver demand should remain strong due to renewable energy growth, growing numbers of electric vehicles and the need for much more AI centers.”

On the supply side, Wyckoff noted that mining disruptions and depleted silver stocks are contributing to significant deficits, which are pushing prices up. “Potential U.S. interest rate cuts and a weaker U.S. dollar are expected to continue to drive speculator demand to silver—not to mention any geopolitical flareups that would drive keener safe-haven demand for silver,” he said.

Turning to the technical picture, Wyckoff noted that silver still looks overall bullish on both the longer-term and shorter-term charts. “However, silver is in a very mature bull market run and it's very likely the market will at least need to pause in the coming months,” he warned. “Raw commodities, including metals, are highly cyclical and go through well-defined periods of boom and bust. There’s no doubt silver is in a boom cycle at present. That means a bust cycle is next. The only uncertainty of that is the timing of the beginning of the bust.”

“Looking at the magnitude of the silver boom, as seen by the monthly continuation chart for nearby silver futures, it appears the magnitude of the bust will also be large.”

Wyckoff projects silver prices will bust toward the middle of 2026. “But after the bust, whenever it comes, will come another boom,” he added. “That’s the continually proven nature of raw commodity markets.”

KitcoNews