The Fiscal Grand Canyon

share

share

share

share

share

share

share

share

share

share

The cycle of hyperinflation is already upon us. It was set in motion long ago.

We are in the ultimate conundrum. Politically, the US Government, Treasury, and Central Banks must satisfy – pay for – unfunded liabilities and promises.

But the “money” is simply a desperate conjuring meant to keep the doors of government open.

The dollar as a concept is temporary and limited. Many outside the mainstream have observed ubiquitous evidence that the end is near.

We know it’s limited because history shows this to be true. All fiat currencies, all world reserve currencies eventually died.

There are modern case studies we can examine. They share characteristics that we project into real time and thereby serve as warning signs.

And despite the vast management of statistics and reporting that now shape perception, it is still relatively simply to peel away the layers to find reality.

For dollar collapse, the issues boil down to a simple set of variables that fit into an equation. A universal equation that ultimately describes a level of confidence across a given monetary region.

In “Monetary Regimes and Inflation: History, Economic and Political Relationships”, Peter Bernholz studied of 29 cases of hyperinflation and looked at the circumstances that led up to them.

Vicent Cate’s “How Fiat Dies”, (an equally invaluable and accessible resource) summarizes here http://howfiatdies.blogspot.com/2012/10/faq-for-hyperinflation-skeptics.html that:

He (Bernholz) found that the best predictor of hyperinflation is government debt over 80% of GNP and the deficit over 40% of government spending, in a country that prints its own money.

Note that 50% deficit spending would mean spending twice what was collected in taxes.

The US is over the debt number and not far from the deficit number, so the danger of hyperinflation is real.

However, the deficit number is not all that it appears to be. Even gross domestic product is a figment in terms of how measures real growth. But the gross national product is even worse. (GDP includes foreign land production abroad from multinational corporations).

We know we have a massive build-up of money supply (across all measures) and massive debt. This is combined with slowing growth and massive deficits that are hidden by a thin layer of belief.

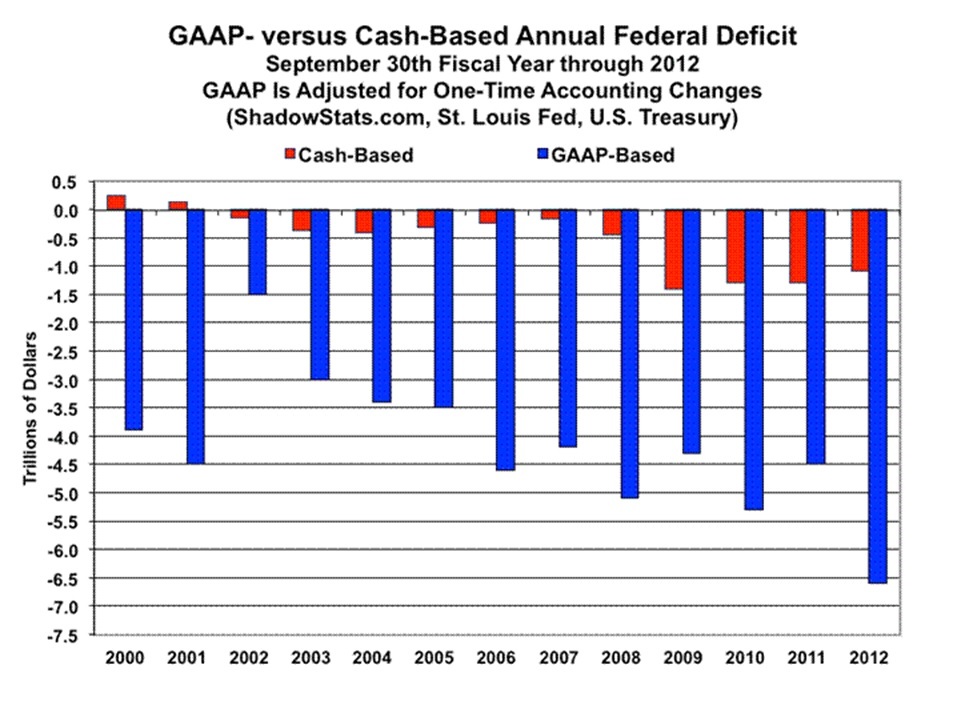

The belief is that the US has control over its budget. The combination of fiscal cliff and less spending gives rise to a cash-based (versus the generally accepted or GAAP-based) accrual headline number.

(GAAP makes it easy to accurately compare one company’s financial statements to another. Accrual accounting recognizes expenses when incurred and revenues when earned. It also applies the matching principle. This means that expenses related to generating revenues or delivering the services tied to the revenue are booked in the same period that the associated revenue is earned).

But in fact however, according to the pioneering work of John Williams of ShadowStats:

Using GAAP-based accrual accounting, though, as typically used by private corporations, the government’s day-to-day operations were shown to have suffered a shortfall of $1.3 trillion, with an additional $5.3 trillion shortfall in the year-to-year increase of unfunded liabilities in social programs, such as in Medicare and Social Security. Those unfunded liabilities are reported in terms of net present value (NPV), where future liability dollar estimates have been reduced to reflect the time-value of money. Effectively, the NPV indicates the amount of cash needed in hand today in order to meet those unfunded obligations.

Total Government Obligations. Based on the same official GAAP numbers, the federal government’s total obligations as of September 30, 2012, stood at $85.4 trillion, or 5.5 times the level of fiscal-2012 GDP. The GDP, though, is not that meaningful a measure here, other than it gives some perspective to the magnitude of the government’s annual deficit and total obligations.

….even with the government seizing all salaries and wages, taxes simply could not be raised enough to bring the system into balance for one year, let alone for future years. That also ignores the question—raised earlier—of whether raising taxes has reached a tipping point, where further tax increases would slow the economy and reduce—instead of increase—tax revenues. Separately, every penny of government spending—except for Social Security and Medicare—could be cut, but the system still would be in annual deficit.

This is just one more false precept in an array of statistical (data) massage – so called ‘normalizations’ giving way to false headlines that feed into perception and a false sense of security.

In order to keep the system going, the only way to satisfy the needs of today and tomorrow are with money printing (and Money Velocity) on an unimaginably grand scale.

We have a massive misperception of debt that makes us all the more at-risk for little earthquakes. Because when that mis-pricing comes to the collective awareness, the shock will lead to an irreversible panice.

When only the few are aware, confidence is easy to contain, either by conspiracy meme, or the sheer level of cognitive dissonance the issue tends to invoke.

But true shifts in confidence come with no warning. The awareness is always present. Perception changes overnight.

********

For more articles and commentary like this – to explore and find some piece of mind in the space between actual price discovery and the reality of the macro-financial state of things – visit us at http://www.Silver-Coin-Investor.com

share

share

share

share

share