Future US Oil Production Will Collapse Just As Quickly As It Increased

share

share

share

share

share

share

share

share

share

share

While U.S. oil production reached a new peak of 10.25 million barrels per day, the higher it goes, the more breathtaking will be the inevitable collapse. Thus, as the mainstream media touts the glorious new record in U.S. production that has both surpassed its previous peak in 1970 and Saudi Arabia’s current oil production, it’s a bittersweet victory.

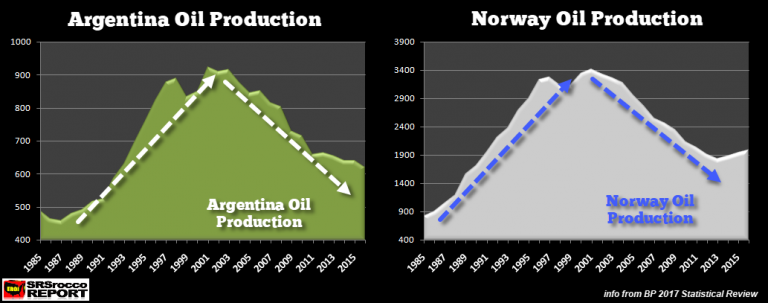

Why? There are two critical reasons the current record level of U.S. oil production won’t last and is also, a house of cards. First of all, oil production profiles tend to be somewhat symmetrical. They rise and fall in the same manner. While this doesn’t happen in every country or every oil field, we do see similar patterns. For example, this similar trend is taking place in both Argentina and Norway:

Here we can see that oil production increased, peaked and declined in a similar pattern in both Argentina and Norway. However, many countries had their domestic oil industries impacted by wars, geopolitical events, and or enhanced oil recovery techniques that have resulted in altered production profiles. Regardless, the United States experienced a symmetrical oil production profile from 1930 to 2007:

As we can see in the chart, U.S. oil production from 1930 to 2007 increased and then declined in the same fashion. On the other hand, the new Shale Oil Production trend is much different. What took 23 years for U.S. oil production to double from 5 million barrels per day (mbd) in 1947 to a peak of nearly 10 mbd in 1970, was accomplished in less than a decade with the new shale oil industry. Total U.S. oil production doubled from 5 mbd in 2009 to over 10 mbd currently.

For those Americans or delusional individuals who believe the U.S. oil industry will be able to continue producing a record amount of oil for the next several decades, you have no idea about the financial carnage taking place in the U.S. shale oil industry. This leads me to the second reason. The U.S. Shale Industry hasn’t made any money producing oil since the industry took off in 2008. And it’s even worse than that. Not only have they not made any money, but they have also spent a lot of investor money (most that will never be returned) and added a massive amount of debt to their balance sheets.

According to the Financial Times article, In Charts: Has The US Shale Drilling Revolution Peaked?, they provided the following chart on the negative free cash flow in the U.S. Exploration and Production Industry:

Because the U.S. Shale Oil Industry was a Ponzi Scheme from day one, the shale oil companies had to design clever investor relations presentations to bamboozle, hoodwink, swindle and hornswoggle investors from their money. And boy did it work. Even though two-thirds of the U.S. shale energy companies are still losing money, investors continue to flood the energy sector with gobs of Dollars and Pennies from Heaven. Without these much-needed funds, the U.S. Shale oil industry would go belly-up.

Now, there’s another downside to the U.S. Shale Oil Industry that I haven’t yet mentioned. Because shale energy industry is producing a grade of oil that has a very high API gravity (very light oil), we have to export more and more of it as our refiners can’t use it all. The notion that the U.S. decided to start export oil because we have become a leading oil producer is pure BOLLOCKS. The real reason the U.S. Government allowed the exporting of oil in 2015 was that our refining industry couldn’t use it all…LOL.

If you have your thinking cap on, why would we have to export oil if we could use it ourselves?? Well, again… the answer is that we cannot use all of our “light tight” shale oil. Here is a chart from one of the members of the PeakOilBarrel.com site:

According to the U.S. Energy Information Agency (EIA), the majority of growth in U.S. oil production is in the very light API gravity oils above 40. Unfortunately, there is a glut of high API Gravity oils (light oil) in the United States and the world. In the Petroleum Economist article, U.S. Tight Oil: Too Light, Too Sweet, stated the following:

While the US runs on light products, with gasoline making up nearly 48% of the de�mand barrel, the rest of the world has a stron�ger taste for middle distillates. The global de�mand barrel is 36% middle distillates and only 32% gasoline. European and Eurasian mid�dle-distillate demand is an enormous 49.3% of the barrel, according to the latest BP Statistical Review. Middle-distillate demand is widely ex�pected to grow as worldwide trucking volumes increase and maritime fuels begin a major shift to marine gasoil from heavy fuel oil so they comply with new sulphur-emissions limits. Product consumption patterns outside the US argue for processing middle-gravity crudes such as Arab Light, Iranian Light and Russian Urals, rather than extra-light barrels such as 48°API gravity Eagle Ford.

The weighted average API gravity of EU crude imports in 2016 was 35.2°, according to Eurostat. Refinery inputs look similar: the current average API gravity of the crude entering American refin�eries is approximately 32.3°, nearly unchanged for the past 30 years despite the recent rise in light oil output. Worldwide investments into more complex, higher conversion refineries have eroded very light sweet oils’ long-prized light-distillate yield advantage.

As the article states, the rest of the world demands more middle distillate fuels that come from medium grade oil stock. Furthermore, the weighted average API gravity of EU (European Union) crude oil imports in 2016 was 35.2°. However, the majority of U.S. Shale oil API gravity is 40-50°+.

Thus, as the U.S. shale oil industry continues to produce more light oil, exports will likely increase. And we already see this taking place. The U.S. net oil imports have risen from 2 mbd in Oct 2017 to 4.4 mbd currently. It is difficult to tell how much net oil imports will be over the next six months, but it is quite interesting to see the U.S. importing more oil even though we just hit a record of 10.25 mbd.

In conclusion, U.S. oil production in the future will collapse just as fast as it increased. It is hard to forecast when U.S. oil production will finally peak for good because there is so much fraud, leverage, and debt propping up the system. But, when the Greatest Financial Ponzi Scheme finally pops… I believe U.S. oil production will collapse much faster than we realize.

Courtesy of SRSrocco Report.

share

share

share

share

share

More from Silver Phoenix 500