Open The Door

share

share

share

share

share

share

share

share

share

share

Nickel is present in over 3,000 different alloys that are used in over 300,000 products for consumer, industrial, military, transport/aerospace, marine and architectural applications.

Nickel’s biggest use, about 65 percent, is in alloying - particularly with chromium and other metals to produce stainless and heat-resisting steels. Its primary function is to stabilize the austenitic (face-centered cubic crystal) structure of the steel. Normal carbon steel will, on cooling, transform from an austenite structure to a mixture of ferrite and cementite. When added to stainless steel nickel stops this transformation keeping the material fully austenite on cooling. Austenitic stainless steels have high ductility, low yield stress and high tensile strength when compared to carbon steel - aluminum and copper are examples of other metals with the austenitic structure.

Another 20 percent is used in other steels, non-ferrous alloys (mixed with metals other than steel) and super alloys (metal mixtures designed to withstand extremely high temperatures and/or pressures or have high electrical conductivity) often for highly specialized industrial, aerospace and military applications.

About nine percent is used in plating to slow down corrosion and six percent for other uses, including coins, electronics, in batteries for portable equipment and hybrid cars, as a catalyst for certain chemical reactions and as a colorant - nickel is added to glass to give it a green color. In many of these applications there is no substitute for nickel without reducing performance or increasing cost.

Opportunity is knocking

Many analysts are saying the nickel market is over supplied and London Metal Exchange warehouses are seemingly reaching record levels every day. The nickel story is dead and buried, move on and make your money elsewhere…right?

Wrong.

Here at aheadoftheherd.com we KNOW the nickel story is alive and well and just getting started. Nickel is presenting a huge profit opportunity in this author’s opinion.

Read on to find out why.

Action & Reaction

Indonesia’s President Yudhoyono prohibited ore exports from Southeast Asia’s largest economy in January. Yudhoyono is betting that investment and higher prices will more than offset job cuts and lost revenue from unprocessed ore shipments.

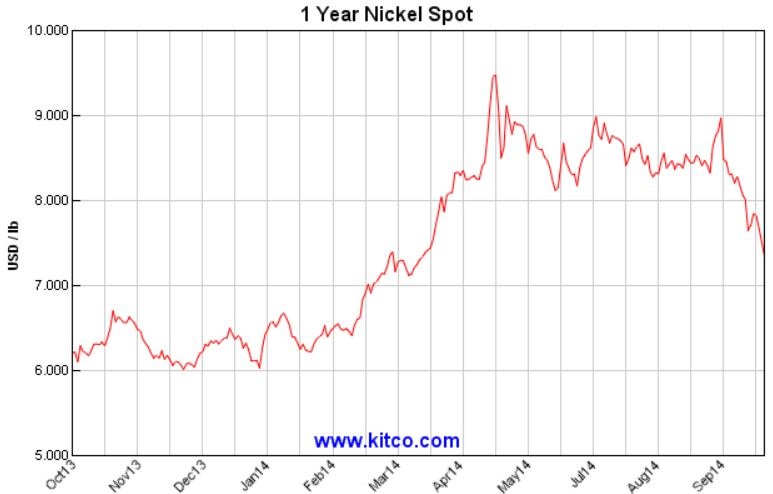

Nickel rallied as much as 56 percent on the ban, climbing to $21,625 a tonne in May.

Nickel rallied as much as 56 percent on the ban, climbing to $21,625 a tonne in May.

The reaction was swift, money poured into the country…mostly Chinese investors planning to build at least 30 nickel smelters that will process about 20 million tons of ore when they start production - supposedly in 2017.

Nickel prices have severely come off their high and are currently below $17,000.00 a ton. Why?

Four factors are driving the price decline:

- Concern that the Indonesian ban will be softened.

- Rising refined LME inventories.

- Philippines will not implement a ban on exports of nickel yet.

- Slowing Chinese usage

Investments in smelters, processing plants and accompanying infrastructure have reached a frantic US$4.9 billion so far this year. Indonesia’s Energy and Mineral Resources Ministry has categorically stated the ban on ore exports will remain in place as the curbs will spur as much as $13 billion more in investments by 2017. All political opposition parties are in full agreement.

“It’s important to maintain the policy. Investors have made it clear to the government that they don’t want any change in policy because it could damage all their investments and they would lose trust.” R. Sukhyar, director general of mineral and coal

The rise in high quality refined nickel LME stocks is important - it’s a widely followed metric that’s very misleading.

The rise in high quality refined nickel LME stocks is important - it’s a widely followed metric that’s very misleading.

London Metal Exchange grade material accounts for just a third of the overall nickel market when scrap and other grades are taken into account.

The wider nickel market is tightening significantly.

Scrap nickel in Europe fetches 83 to 86 percent of the LME price, that’s up from 75 per cent at the start of the year. In Asia, scrap discounts are thought to be even narrower at 90 percent of the LME price.

The Philippines was preparing to implement a ban on exports of unprocessed minerals similar to Indonesia’s Mining Law of 2009 – as with Indonesia’s new law it will take several years before the Philippines new mining and export policy is ready to implement. A yes/no decision is expected within months.

In 2013 China’s nickel usage climbed by about seven percent to 1.77 million tonnes. How much of this growth was because the metal is use for financial purposes as well as being stockpiled by NPI producers ahead of the export ban is hard to tell.

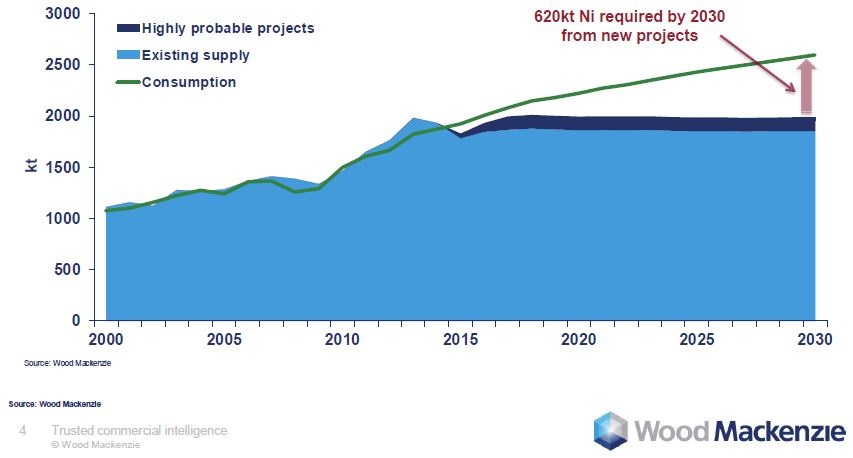

Global stainless steel demand is a better tell. Increased Asian demand, a potential recovery start in Europe and a continuing recovery in the U.S. all point to increased nickel demand. Fastmarkets.com, in their Nickel Analysis and Forecast Q2 2014 expects nickel demand to have grown around eight percent over 2014 to around 1.91 million tonnes.

Nickel Pig Iron

Indonesian smelters might, in three years, again fill all or part of China’s current need for nickel.

The Philippines might, or might not have the answer.

In the meantime expect scrap to fill a huge part of the supply/demand gap and supplies to tighten considerably with all grades going higher in price as China burns through its, and the world’s, low grade inventory in a desperate race just to keep even with its current nickel pig iron (NPI is a low-grade ferro-nickel) demand.

London Metal Exchange grade material, the class-one nickel in their storage warehouses - full-plate cathode, cut cathode, briquettes and pellets - is not used in China for NPI production.

NPI production has not spread to other stainless steel producers. The main reasons why the use of NPI has not spread are:

- Cost of shipping large volumes of low-grade nickel ores.

- Environmental issues related to processing.

Remember - Indonesian ore is the raw material for up to 30 per cent of global production of nickel, most of it heads to China to be processed into nickel pig iron.

China’s stainless steel industry uses NPI to produce the stainless steel the country uses and exports. Prior to implementation of the export ban Indonesian miners and traders ramped up nickel ore shipments.

Considerable nickel ore stockpiles have built up at Chinese ports so it will take time for the supply side to tighten.

But the net effect of an Indonesian nickel ore export ban will be twofold:

- A significant rise in the costs of Chinese NPI production, which will raise the floor price for all nickel grades in turn.

- A significant rise in the usage and cost of LME refined nickel as Chinese stockpiles are depleted.

Nickel Talk

According to Standard Chartered LME nickel inventories should start to fall by the middle of 2015 as stainless-steel producers in China are forced to switch from using nickel-pig iron to other forms of nickel and ultimately the refined metal.

According to Morgan Stanley the ban on ore exports will shift the global nickel market into a deficit in 2015 for the first time since 2010. Nickel demand will outstrip supply by 97,100 tons in 2015.

Nickel was listed by Societe Generale SA among its top picks for this half as the curb was seen moving the market to shortages.

Goldman Sachs Group sees a 200,000 ton Ni deficit in 2015.

Stephen Briggs, a metal strategist at BNP Paribas in London, says a jump to $25,000 a ton is plausible, Briggs outlook is conditional on the maintenance of the ore export ban.

Nickel Market Facts

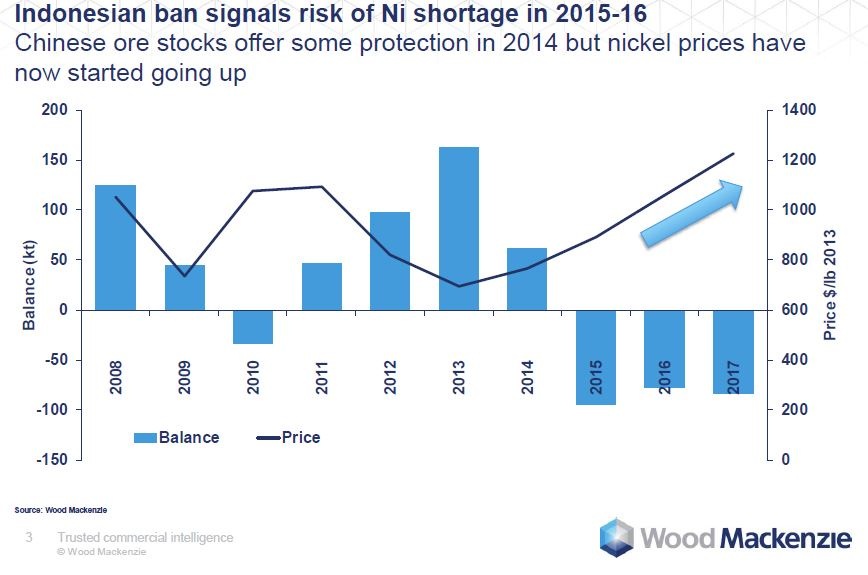

Fact - The nickel market has been hampered by oversupply in recent years. Jakarta’s ban on ore exports will drastically change that.

Fact - Annual Philippine ore output accounts for the equivalent of around a third of Chinese NPI production. Once NPI stocks have been depleted the NPI market in China faces a significant shortfall.

Fact - Once stocks run out, stainless steel mills in China will have to return to more expensive refined nickel.

Fact - 50 per cent of LME inventory nickel is concentrated in Jahor in the form of high quality briquettes. Historically when so much metal has been concentrated in just one location it’s most often because the metal is tied up in warehouse or financing deals and not available to the market.

Fact - Data shows nickel ore imports into China from the Philippines rising to records.

Roughly 60 percent of global available nickel is in laterite deposits – a deposit in which weathering of ultramafic rocks has taken place.

Roughly 60 percent of global available nickel is in laterite deposits – a deposit in which weathering of ultramafic rocks has taken place.

The initial nickel content is enriched in the course of lateritization - under tropical conditions fresh rock weathers very quickly. Some metals may be leached away by the weathering process but others, such as aluminum, iron and nickel can remain.

Indonesian lateritic nickel ore (saprolite - higher nickel, magnesium and silica but lower iron content) has higher nickel content, typically 1.8 percent to 2 percent, than the 1.5 percent lateritic ore (limonite - higher in iron and lower in nickel, magnesium and silica) from the Philippines.

Once the 1.8 percent Indonesian saprolite runs out China is going to have to produce from the Philippines 1.5 percent limonite ore. That shift is thought to raise the cost of making nickel pig iron to about $20,000 a ton.

Fact - The Philippines might be able to supply up to 20 percent of the ore amount Indonesia supplies. There is no other place for the Chinese to source ore for their NPI industry that doesn’t run into high shipping costs.

Fact - Globally the stainless steel industry has had no need to restock given the ample supply and good availability of nickel. When restocking starts it can lead to some fast rebounds in nickel prices.

Fact - Increased political risk, population and economic growth are causing the exploitation of lower grade larger deposits in geo-politically riskier countries. Mineral deposit distribution is log-normal – a few large deposits control supply.

Fact - In 2010 Chinese nickel consumption was .4 kilogram per capita, Germany was at 1.3 and Japan was the same. If the Chinese were to consume nickel at the same rate as Germans and Japanese Chinese nickel demand would increase by over one million tonnes

Mohr Berlin

“The world supply & demand balance will shift into a marked ‘deficit’ in 2015, as China depletes its inventory of Indonesian ore for ‘Nickel Pig Iron’ production (used in stainless steel).” Patricia Mohr, Scotiabank’s vice president of economics and commodity market specialist

Mohr sees nickel prices moving to US$10.75 in 2015 and then up to US$12 in 2016.

Anton Berlin, head of strategic marketing at Norilsk said the price of this year’s best-performing industrial metal is still too low as the market is set to slip into a deficit next year…

"The nickel price is still quite low fundamentally, as it is below production costs at a number of mines worldwide, including our facilities in Australia. Next year the market may turn into a deficit given that the Indonesian ban is still in place. The price should go up in order for the idled producers to restart working as there is demand for the metal. The metal should trade at $20,000 to $25,000 a ton in order for loss-making producers to break even."

Geo-political Concerns

Russia is the world’s leading country for nickel production and Russian mining giant Norilsk Nickel is the world’s largest producer. Most of the countries nickel production (an amazing one-fifth of global production) is from Norilsk - the largest nickel sulfide deposit in the world.

Russia might be facing export sanctions. Should the situation worsen and geopolitical tensions in Ukraine ratchet higher Norilsk might not be able to export nickel - the potential for escalation remains very high.

Conclusion

Three things are for sure:

- When the Chinese NPI supply has dried up we’ll definitely see it. LME nickel stocks will start to fall drastically.

- As the supply of NPI becomes depleted and Chinese producers switch to refined nickel, competition for refined nickel is bound to get fierce; the competition for limited supplies will show up in nickel premiums.

Refined nickel, held in LME warehouses is not the answer - all the metal held in LME warehouses is only 1.5 months of global supply.

Oh yeah, I said three things are for sure – 3. Nickel is going higher, much higher in price.

Ask yourself, “when is the best time to invest?”

While you mull over that question here’s five more facts for you:

- Nickel is currently unloved.

- There aren’t any nickel names left. Without Inco or Falconbridge, who do you invest in if you want nickel? The largest nickel producing companies, Norilsk, Vale and Xstrata don't actually provide a lot of leverage to nickel as they are diversified miners - meaning they also produce iron, manganese, bauxite, aluminum, copper, coal, cobalt, potash, platinum-group metals, gold and silver.

- Every country needs to secure supplies of needed commodities at competitive prices yet supply is increasingly constrained and demand is growing.

- All of a sudden juniors exploring for nickel will become much more interesting. Especially so if they are working in geopolitically stable countries.

- Pure junior nickel exploration plays aren't common.

“Someone's knockin' at the door

Somebody's ringin' the bell”

Let Em In, Paul McCartney

When opportunity knocks I open the door. Is nickel, and perhaps a nickel junior resource company, on your radar screen?

If not, one should be.

********

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

share

share

share

share

share

More from Silver Phoenix 500