Record Global Oil Demand: Even As The Price Of Oil Declined

share

share

share

share

share

share

share

share

share

share

There is this notion put forth by the media that a decline in global oil demand caused the huge drop in the price of oil. Ironically, global oil demand is higher than ever… that is, according to the IEA – International Energy Agency.

There is this notion put forth by the media that a decline in global oil demand caused the huge drop in the price of oil. Ironically, global oil demand is higher than ever… that is, according to the IEA – International Energy Agency.

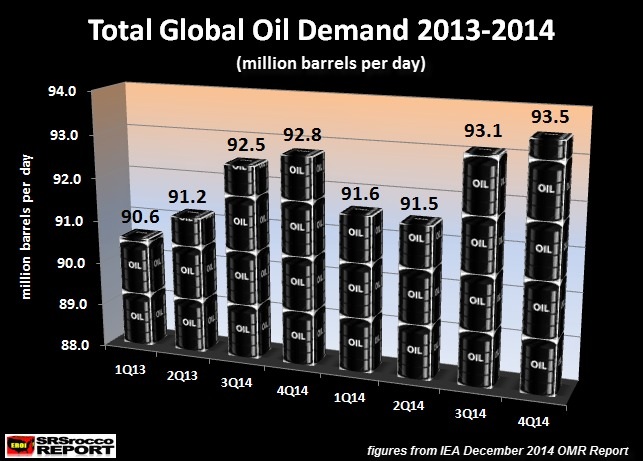

Not only did the world consume the most oil it had ever in the third quarter of 2014, it was 600,000 barrels per day more than it did in the same period last year. In Q3 2013, global oil demand was 92.5 million barrels per day (mbd), compared to 93.1 mbd in Q3 2014:

As we can see from the chart, global oil demand was only 90.6 mbd in the first quarter of 2013, increased 1 mbd in Q1 2014 to 91.6 mbd and then jumped up to 93.1 mbd in Q3 2014. I don’t see any falling demand here.

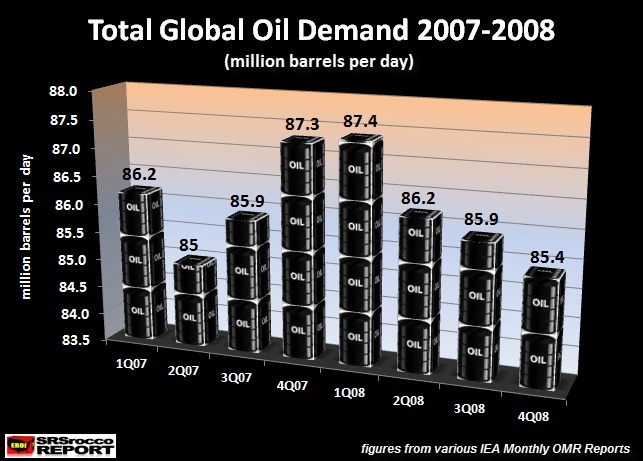

Now, if we go back to the 2008 collapse in the price of oil from $148 down to $30, it did occur on the back of falling world oil demand. In the first quarter of 2008, global oil demand was 87.4 mbd, but just three-quarters later, it declined 2 mbd to 85.4 mbd:

Furthermore, global oil demand was down 1.9 mbd in a year’s time from 87.2 mbd in Q4 2007, compared to 85.4 mbd in Q4 2008. Thus, the fall in the price of oil did take place as world oil demand declined significantly.

On the other hand, global oil demand is forecasted to increase from 92.8 mbd in Q4 2013 to 93.5 mbd in Q4 2014. So… what gives?? How can the price of oil fall as demand increases??

Well, that’s a good question. I believe the fall in the price of oil is due to a DECLINE OF EXPECTED DEMAND on top of INCREASED SUPPLY. In their May 2014 OMR Report, the IEA forecasted that global oil demand would be 93.5 mbd in Q3 and 94 mbd in Q4. Unfortunately, demand is 400,000-500,000 barrels per day less than what was forecasted.

You see, it doesn’t take much to disrupt the balance and price. However, as we can see, actual global oil demand is higher not lower than what took place during 2008 when overall demand fell 2 mbd.

Did the U.S. Purposely Destroy Global Oil Demand?

There are many opinions as to why the price of oil has fallen more than 50% in the past four months. Some believe it’s the Saudi’s and the U.S. working together to destroy Russia, while others believe it’s the Saudi’s trying to kill the U.S. Shale Oil Industry. And then we have the media who attributes the huge fall in the price of oil due to weakening demand as economic activity falls.

I actually believe the fall in EXPECTED OIL DEMAND is due to the U.S. instigating sanctions on Russia. Let me explain. Sanctions on Russia really began to have an impact in the beginning of the second quarter of 2014. According to the article, U.S. Sanctions On Russia Begin To Bite:

Russian markets took another knock Friday as sanctions imposed by the U.S. over the annexation of Crimea began to hit oligarchs and their businesses.

Moscow’s MICEX index fell more than 2% — taking its losses for the year to 14%. The ruble was steady, after dipping early in the day, but has still lost about 10% since the start of the year.

And President Obama warned Moscow the U.S. would target key sectors of the economy if Russia escalates the crisis in Ukraine.

Then in the third quarter, economic activity continued to soften… Russia’s Economic Growth Slows For A Third Quarter:

MOSCOW—Russia’s annual economic growth continued to slow in the third quarter, as gross domestic product added 0.7% compared to the same period of 2013, the Federal Statistics Service preliminary data showed Thursday.

Russia is on track to post its weakest economic growth since 2000, the first year Vladimir Putin was president, excluding the year 2009 when the economy contracted under the burden of the global financial crisis. Massive capital flight on the back of Western sanctions and a recent decline in oil prices pose additional headwinds for the commodity-dependent economy.

Not only has Russia’s economy suffered, so have countries in the European Union that were dependent on trade with Russia. According to the article, Eurozone Growth To Slow As Germany And France Falter:

The eurozone economy will grow more slowly than expected during the rest of this year as global conflicts continue to undermine business confidence, Europe’s largest central bank has warned.

…. It said conflicts in Ukraine and elsewhere – and European sanctions against Russia – were also affecting corporate sentiment, undermining the growth predicted for the rest of 2014.

If Russia and the European countries are experiencing a weakening of economic activity… how does that impact OIL DEMAND?? When you start to consider all the countries impacted by the Russian sanctions, then a decline of “Expected oil demand” starts to add up.

One more thing, the IEA forecasted that global oil demand would be 94 mbd in Q4 2014. However, it fell short by 0.5 mbd of the expected 94 mbd, which is only a decline of a half percent. Think about that for a minute. The price of oil declined 50% in the past four months on a decline of 0.5% of expected demand.

I dear say… it doesn’t take much to curtail economic activity to slow down global oil consumption by 0.5%.

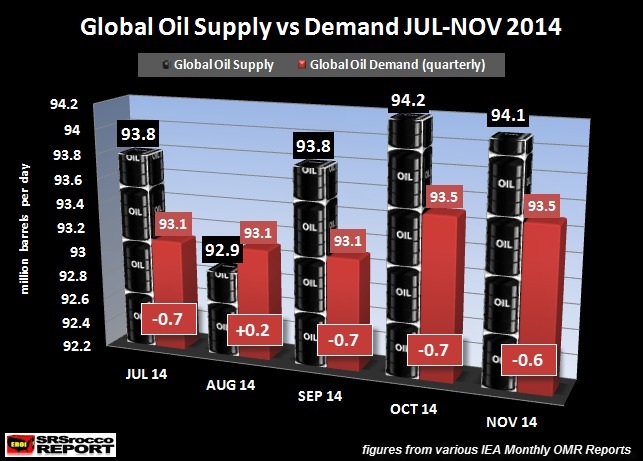

Let’s take a look at the current SUPPLY vs DEMAND situation in the global oil market:

According to the IEA’s May 2014 OMR Report, the world was expected to consume 93.5 mbd of oil in Q3 and 94 mbd in Q4. As we can see (shown by the RED BARS), overall oil demand was 400,000 barrels a day (bd) less than forecasted in Q3 and 500,000 bd less than Q4.

As economic activity weakened due to the Russian sanctions, the IEA’s expected global oil demand fell short. The RED BARS are quarterly oil demand figures released by the IEA and the OIL BARREL BARS are actual monthly supply. From Jul-Nov, global oil demand averaged about 600,000 bd less than supply.

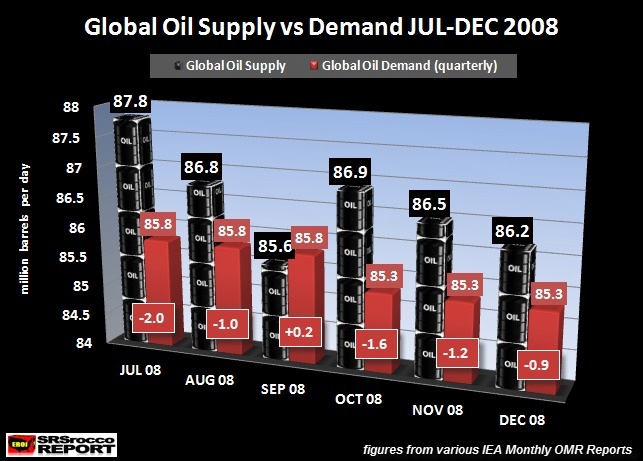

However, the oil supply vs demand equation was a much less than what took place in the second half of 2008:

In the chart above, global oil supply was 2 mbd higher than demand in July 2008. Demand continued to fall in the last quarter of 2008… and so did supply. The reason for the big decline in global oil supply in September was due to hurricane activity in the Gulf of Mexico.

The huge decline in the price of oil in 2008 was due to demand destruction stemming from a collapse of economic activity as the U.S. Housing and Investment Banking System imploded. However, I believe the present decline in the price of oil is a direct result from an U.S. orchestrated collapse of the Russian economy.

We must remember, a slight decline in economic activity across many countries will also impact oil consumption… a few ten’s of a thousand barrels a day lost here and there add up.

A Rising U.S. Dollar Also Negatively Impacts Oil Producing Countries Economic Growth

While the Main Stream media continues regurgitate the notion that falling oil prices act as an economic stimulus, they only do so for countries that act as a PARASITE on others… such as the United States.

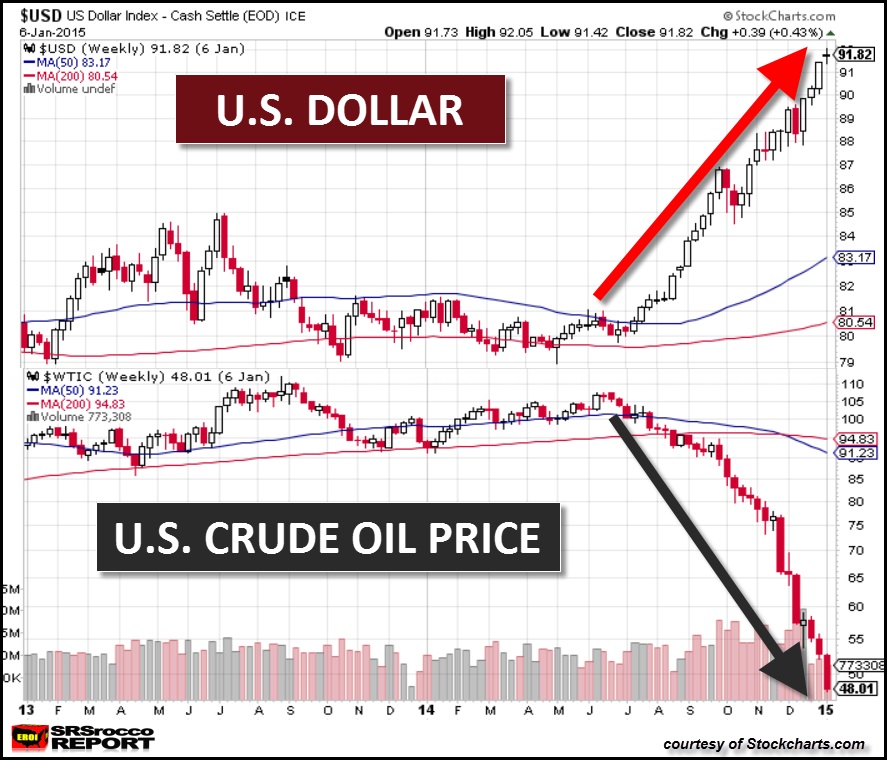

Before I get into that, let’s look at the U.S. Dollar vs Oil Price chart:

What a perfect MIRROR IMAGE… the price of oil declined in exact opposite fashion as the rise in U.S. Dollar index. This is one of the benefits of being the world’s reserve currency. Not have the U.S. sanctions on Russia impacted the Russian and European economies… it’s also wreaking havoc on Middle Eastern and other oil-producing nations.

According to the IEA’s December OMR Report:

- sharp declines in the value of many currencies, compared to the US dollar, have minimised, if not negated, the impact of lower crude prices on local-currency, retail product markets, even as they have raised the price of imported goods and services, thus putting a dampener on consumption.

- lower oil prices significantly dent potential export revenues in net oil-exporting countries, slashing their income streams and in turn denting demand. In particularly cash-strapped economies, such as Venezuela and Russia, this impact is likely to be magnified as the risk of default escalates.

So, what we have here is a typical DOMINO EFFECT set off by the U.S. sanctions on Russia. I believe if the United States didn’t meddle in Ukraine or apply sanctions on Russia, economic activity and oil demand would have remained strong… along with the price of oil.

How about China? Some believe the weakening Chinese economy is to blame for a fall in oil demand. Again, according to the IEA, China is forecasted to consume 10.3 mbd of total oil products in 2014, up from 10.1 mbd in 2013. This turns out to be 100,000 barrels a day less than the 10.4 mbd, the IEA forecasted at the beginning of the year.

So… while China is consuming less than expected, it’s only one-fifth of the 500,000 barrels a day of lost global demand forecasted by the IEA in May of 2014. Regardless, global oil demand continues to increase even though its less than previously forecasted. This is a much different situation than FALLING DEMAND as we experienced in the second half of 2008.

Furthermore, the IEA forecasts that global oil demand will continue to increase in 2015 at 900,000 barrels per day more than 2014… even with the downward reversions due to weakened economic activity and geopolitical factors.

The U.S. Shale Oil Industry Has The Most To Lose

The U.S. Government may have shot itself in the foot by instigating sanctions against Russia, which negatively impacted economic activity and global oil demand…. thus causing a 50%+ drop in the price of oil.

While Russia and Saudi Arabia would much rather receive $100 for their oil rather than $50, the high-cost U.S. Shale Oil Industry is about to receive an enema.

Already CLR – Continental Resources, the largest company drilling in the Bakken, spent $1.1 billion more on capital expenditures Q1-Q3 2014 than they received from operating cash flow. And this was when the price of oil was $93 a barrel. How bad will it be for Continental at $45-$50 oil??

Sure, maybe some of these companies have hedged production at higher prices, but I doubt they hedged 100% and for what time period? I believe we may soon see a peak and decline of oil production at the Bakken and then at the Eagle Ford.. the two largest shale oil fields in the United States.

The lower oil price is already impacting the U.S. shale oil industry as drilling rigs at the Bakken and Eagle Ford are declining . I would imagine the situation will get much worse in the second quarter of 2015, when the majority of backlogged wells already drilled (awaiting fracking) have been brought into production.

If the price of oil does not recover in the first half of 2015, we will likely start to see a decline in production at the Bakken, followed by the Eagle Ford.

As I have stated several times before, the peak and decline of U.S. Shale Oil Production is the DEATH KNELL to the U.S. and global economy. This will have grave implications for most paper assets going forward.

Gold and Silver will turn out to be some of the best investments to own in a peak oil environment.

Please check back for new articles and updates at the SRSrocco Report. You can also follow us at Twitter below:

share

share

share

share

share

More from Silver Phoenix 500