Discussing COMEX Silver

With the open interest in Comex silver blowing out to a new alltime high yesterday, we thought it best to discuss again what this indicates and what it doesn't.

As of yesterday's Comex close, the total open interest in Comex silver is at an all-time high of 241,135 contracts. This blows away the previous alltime high seen on April 20 of last year at 234,787 contracts. Let's first hit the basics...

At 241,135 contracts, total Comex open interest represents 1,205,675,000 ounces of digital silver. The entire world will produce about 825,000,000 ounces of silver this year so this open interest is now at a record 146% of global mine supply. To understand how ridiculously over-leveraged this derivative market has become, compare Comex silver to Comex gold and Comex copper:

-

Comex gold OI 500,627 contracts = 50MM digital ounces vs mine supply of 90MM ounces = 55% of global mine supply

-

Comex copper OI 289,814 contracts = 7B pounds vs 40B pounds of mine supply = 18% of total mine supply

OK, now that you have some sense of the scale of this madness, let's move on. How about some history?

April 20, 2017 was a Thursday. This means that two days earlier, with Comex silver OI at 227,984 and price at $18.40, there was a CoT survey. And what did this CoT show last year?

Large Spec Long = 128,378 Large Spec Short = 24,491 NET LONG 103,887 contracts

Commercial Long = 46,878 Commercial Short = 163710 (an all-time high) NET SHORT 116,832 contracts (also an all-time high)

So, with Large Specs NET LONG nearly 104,000 contracts and the Banks et al NET SHORT at an alltime high, what do you suppose happened next???

Of course you already know. The Specs began to dump longs into the May17 contract expiration and price fell for next 13 consecutive days. The total decline was $2.03! Total open interest fell back to a low of 188,527 on Day 10 of this selloff and The Banks had fleeced The Specs once again.

Now let's compare this to present day by making some reasonable projections for tomorrow's updated CoT.

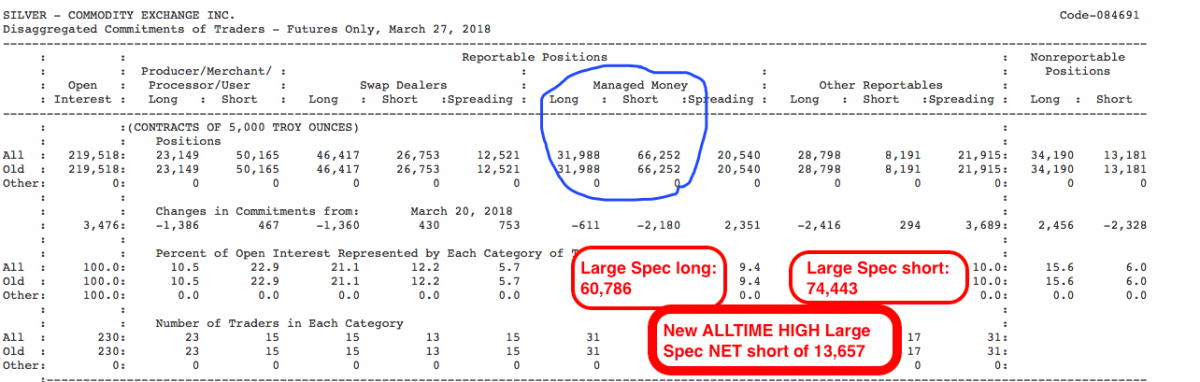

Last week's survey taken March 27 showed:

Large Spec Long = 60,786 Large Spec Short = 74,443 NET SHORT 13,657 contracts

Commercial Long = 82,087 Commercial Short 89,439 NET SHORT 7,352 contracts

You can already see the radical difference one year and $2 in price has made. And if last April's CoT virtually assured that the next move would be a washout of the Spec longs, why wouldn't the current CoT virtually assure that the next move would be a washout and squeeze of the Spec shorts?

But let's not stop there. Last week's CoT was a snapshot from five market days ago. Here's how things have changed since:

March 28: Price down 29¢ and OI up 8,800

March 29: Price up 2¢ and OI up 900

April 2: Price up 40¢ and OI down 900

April 3: Price down 28¢ and OI up 4,400

April 4: Price down 14¢ and OI up 8,400

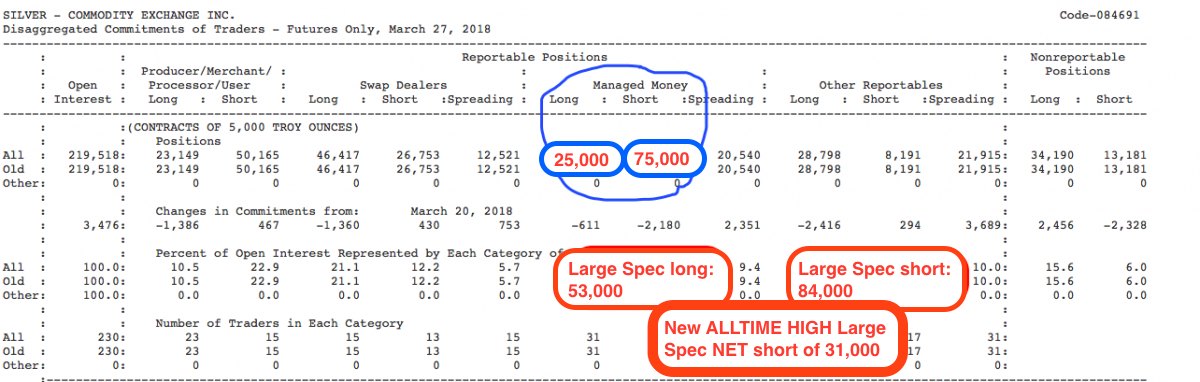

Since total open interest rose on every sharp down day for price, it's very safe to conclude that the Large Specs have continued to pile into the short side of Comex silver at every opportunity. So, while last week's disaggregated CoT looked like this...

An updated CoT, based upon projected changes through yesterday (Wednesday), would look like this:

Now consider these points:

-

The situation compared to last April is the same...but it's the opposite. Just like last April, the Specs will eventually have to unwind positions ahead of the May contract going off the board. But this year, instead of dumping longs, they'll have to cover shorts!

-

If, at present, The Large Specs are NET SHORT something like 30,000 contracts, this likely places the Commercials into a NET LONG position for the first time in the recorded history of mankind.

-

So, for once, The Commercials would actually benefit from a price rally.

-

However, where sharp selloffs ALWAYS benefit the Bank desire to cap price, maybe The Banks won't allow a sharp rally for fear of igniting upside momentum. This must be considered, too.

-

But again, if outsized Spec long positions always lead to selloffs, why wouldn't this incredibly outsized Spec short position lead to a squeeze and rally?

So, we'll see what happens next. Maybe we'll need to move closer to the May18 expirations before the squeeze begins. If anything, we've been warning you for weeks that NOTHING IS GOING TO HAPPEN until The Specs begin to feel pressured by a price that rises through the 50-day, the 200-day and the key resistance level of $17. Until then, we're stuck range bound and moving sideways.

But don't let the current malaise and price range distract you from this truly remarkable situation. Total Comex open interest is at an alltime high. The Large Specs are are building an unprecedented NET SHORT position. And The Commercials (the Banks) are now NET LONG for the first time ever.

A price rally is coming. This rally could be spectacular. The only question is whether or not The Banks will allow it to be.

IF The Banks play the usual game of swapping positions with The Specs, the mass of Spec shorts will be covered but then transferred back to The Banks. Price will rise but perhaps not more than the $2 it fell last year.

IF, however, The Banks stand down and simply hold their positions, this would force The Specs to buy and cover only amongst themselves. This limited amount of liquidity would have the potential to spike price in a rally the size and scope of which we haven't seen since the spring of 2011.

So, sit back and watch. These events will soon unfold and the record level of Large Spec shorts will begin to get squeezed. Once this begins, we'll all get to see the results in real time.

Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.

More from Silver Phoenix 500