The Fed Is A “Pickle”

Breaking news: The Wall Street casino created another all-time high for the Dow during the week ending February 14. Then it fell 35% in March.

The “pickle” description is explained below. Stay tuned.

The Federal Reserve is monetizing bonds—directly funding the federal deficit because congress and the administration spend more than their revenues. The coming recession will increase the shortfall, expand debt and force more monetization. Stagflation anyone?

Corporations, individuals and governments can ill afford higher interest rates. Expect the Fed to monetize at low interest rates to fund government expenditures. QE4ever is happening because it must.

What other gambles exist in the Wall Street casino?

- The Fed bets it can monetize via QE4ever and create minimal consumer price inflation. If not, the BLS will massage statistics.

- The Fed bets it can increase its balance sheet, aid hedge funds, feed Wall Street banks, please President Trump, buy off congress, and keep its position of power and influence. Based on a century of evidence, they can, for a while longer.

- The Fed bets it can levitate the stock market and boost the economy long enough to reelect President Trump in November 2020.

- The Fed “prints” currency units, and those currency units buy congresspersons, presidents, media corporations, the military-industrial-security complex and everyone important. The Fed is betting it will last nearly forever.

- The Fed bets they can continue their “take from the poor and give to the rich” program of controlled dollar devaluation for many more years.

- The Fed bets that “Federal Reserve Notes” are better than gold because they are “the only game in town,” even though gold retains its value and dollars buy less every year, as planned.

- The Fed bets the existence of Fort Knox gold is irrelevant. Total value, at current prices, is less than $300 billion, and the Fed created more than $300 billion from thin air in the past several months.

- The Fed bets it can plan to normalize their balance sheet, even though normalization would create a depression. Plans are not facts.

- The Fed bets it can avoid deflation and manufacture enough, but not too much, consumer price inflation. Doubtful.

IN SHORT, THE FED IS A GAMBLER.

The politicians and economists at the Fed are gambling with the health of the economy, purchasing power of the dollar, individual savings, Fed credibility, pension funding, and retirements. The gamble will work poorly for most people, but the Fed will protect the political and financial elite.

WHAT DO WE KNOW ABOUT GAMBLERS?

A few thrive. Most lose money. Some lose jobs, savings, health, marriages, and their lives. Businesses built Las Vegas casinos from profits generated by customer losses. Many people dumped a huge number of dollars to create and maintain that monument to wishful thinking and hopium.

Las Vegas sounds like the Federal Reserve—a monument to wishful thinking, hopium, greed, and lobbying power.

GAMBLERS ANONYMOUS or GA helps compulsive gamblers. A few clichés from GA:

- If nothing changes, nothing changes. [If the Fed continues “printing,” the devaluation consequences of printing will persist.]

- Once a cucumber becomes a pickle, it can never be a cucumber again. [The Fed has passed the point of no return; it is a pickle.]

- If a gambler holds a shovel, he will dig himself a deeper hole. If he puts the shovel down, it’s possible to climb out. [The Fed will not drop their shovel. Their “hole” will get bigger.]

There are two kinds of gamblers. A “cucumber” gambles and quits. A “pickle” gambles, loses too much, and moves to Las Vegas to dig a deeper hole and gamble more. A pickle’s life usually ends badly.

The Fed is a pickle. It has transformed from an occasional gambler, a cucumber, into a pickle, an incorrigible gambler making bigger bets and blowing larger bubbles every decade. Cucumbers can become pickles, but once a pickle, always a pickle.

SO WHAT? WHO CARES ABOUT VEGETABLES AND FED GAMBLING?

- The Fed gambled that lower interest rates (near zero) would “stimulate” the economy and bail out Wall Street’s bad bets. The cost for “Main Street” was large. We should care.

- But low interest rates made government debt less costly to refinance. This encouraged the government to spend even more and create massive debts. Ugly consequences must occur.

- And low interest rates allowed corporations to borrow inexpensively, buyback stock and levitate stock prices to unsustainable heights. The stock market downdraft will hurt many people.

- Low interest rates minimized income from savings. To get income, low interest rates forced people to invest in risky vehicles, such as overvalued stocks. Total risk increased. The stock market soared, thanks to Fed intrusions, but most profits went to the upper 10%.

- Governments, individuals and corporations borrowed and created excessive debt. That excessive debt is leverage, which makes the economy more fragile. A credit crunch, higher interest rates, a pandemic, war or other shock will devastate the economy, cash flow, profits, savings, investments, available credit, and the purchasing power of the currency.

- The Fed’s market manipulations and interest rate controls encouraged malinvestments and bad decisions. The next recession will be worse than if the Fed had intervened less.

- The Fed claims they saved the global economy in 2008 with at least $16 trillion in below-market loans, swaps, QE and more. The next crisis will encourage the Fed to double down. It worked once, so expect a repeat performance.

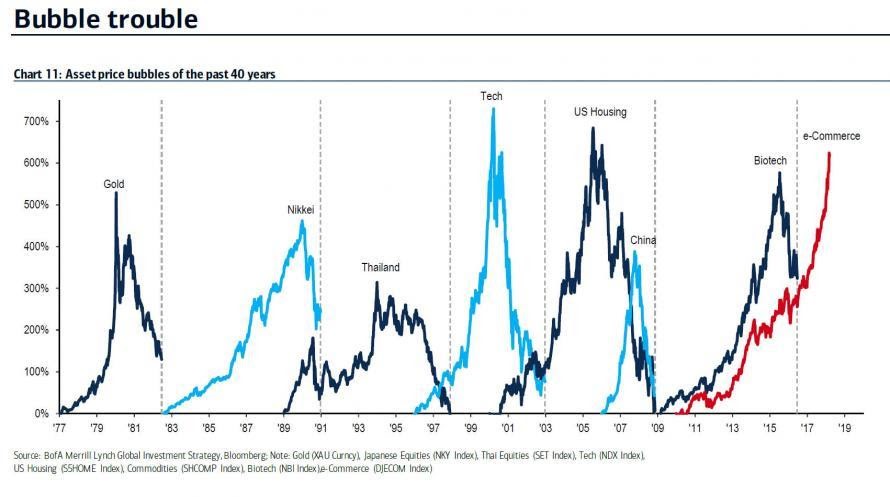

- The Fed created easy credit and expanded bubbles in sovereign debt, stock markets, and real estate. The next correction or crash will remove $trillions in equity from the stock and bond markets. Real estate may crash again. Bet on the Fed to implement QE4ever. Inflate or die!

- How do we know a recession, correction or crash is coming? Because bubbles always burst, and recessions follow booms, regardless of what politicians and Fed Chairmen want. This is a bursting bubble.

QUESTIONS:

- Why do $13 trillion (or so) of sovereign bonds “pay” negative interest? Does this sound like a debt bubble in search of a pin?

- Why were four tech companies (Amazon, Microsoft, Alphabet, and Apple) worth more than $1 trillion each in stock market capitalization? Bubble valuations?

- Why is real estate so expensive in some locations that most people can’t afford it? Prices will come down.

What reset is necessary to restore balance, integrity, and healthy investments to our markets?

- Honest money that can’t be created by the banking cartel.

- Balanced budgets for governments.

- Focus on manufacturing, not financialization.

- Focus on real money, not debt and fake fiat currency units.

- Will any of the above happen? Probably not.

From Alasdair Macleod: “Coronavirus and credit – a perfect storm.”

“This article posits that the spread of the coronavirus coincides with the downturn in the global credit cycle, with potentially catastrophic results.”

From Ron Paul:

“The Fed’s counterfeiting has created the biggest economic bubble in history. A severe economic crisis will be the inevitable result. Indications from Fed Chairman Powell are that more QE will be on the way. Can an increase in the disease succeed in being the cure?”

From David Rosenberg:

This turbocharged debt cycle will end miserably – it’s just a matter of when.

From Sherrod Brown at Senate Banking Committee

“Chairman Powell, you and your highly capable staff at the Fed have been proactive and creative in protecting Wall Street and the money markets from this President’s erratic behavior. And I’m glad you have. We’re all appreciative of that. But what I hope to hear from you today is how you’re going to be proactive and use that same level of creativity to make the economy work for everybody else.”

From Sven Henrich:

“11 years after the financial crisis there is no path to balance sheet normalization, there is no path for rate hikes, there is only the path of more intervention to disproportionally benefit the same people that have benefited for the past 11 years.

“Permanent intervention. That’s their answer. That’s intellectual bankruptcy and exposes central bank policy to be an empty suit.”

Other ideas about what will fix our fiscal, monetary and political mess are available, although unlikely. A summary of Doug Casey’s ideas is listed “for entertainment purposes only.” [his words]

- Allow the collapse of all zombie corporations – banks, brokers, insurers and government contractors.

- Abolish all regulatory agencies.

- Abolish the Fed.

- Cut the military by 90%.

- Sell most government assets.

- Eliminate the income tax.

- Default on the national debt.

Mr. Casey knows his suggestions will not be implemented. “If nothing changes, nothing changes.” No material change is likely, unless a devastating economic collapse forces change upon the world.

GOT GOLD? WHAT ABOUT GOD, GRUB AND GUNS? All may be needed to protect savings and assets.

Miles Franklin can’t help with God, grub or guns, but they sell gold and silver. Buy both to protect your assets from the consequences of Fed gambling with our future and the value of paper dollars. Call 1-800-822-8080.

Gary Christenson

The Deviant Investor

*********

Gary Christenson is the owner and writer for the popular and contrarian investment site Deviant Investor and the author of the book, “Gold Value and Gold Prices 1971 – 2021.” He is a retired accountant and business manager with 30 years of experience studying markets, investing, and trading. He writes about investing, gold, silver, the economy and central banking.

Gary Christenson is the owner and writer for the popular and contrarian investment site Deviant Investor and the author of the book, “Gold Value and Gold Prices 1971 – 2021.” He is a retired accountant and business manager with 30 years of experience studying markets, investing, and trading. He writes about investing, gold, silver, the economy and central banking.

More from Silver Phoenix 500