I Believe In The Stupidity Of The Stock Market

I believe in it in the sense that I believe it will stupidly become even stupider for a short time. So, I’m putting money back into stocks in order to bet on stupid, not because I believe in a phantom V-shaped recovery, but because I constantly hear plenty of people do believe in the “V.”

Right now the farce is with them — reopening has arrived! And these stupid people will believe that means they were right about the “V,” virtually assuring they continue to bet the market up for a little while.

The market ended its short plateau and pushed through all of its major barriers last week, with the Dow finally breaking above its 200-day moving average (typically a very bullish signal of a trend change). All indices have also made it above that 60% retracement I said could be expected in bear-market rallies.

This times out perfectly with the reopening of businesses in the United States. The reopening means economic statistics will improve rapidly. That will give a lot of stupid people many reasons to believe they were right to think the obliterated economy would experience a V-shaped recovery. What they won’t see because they don’t want to see it is that the steep recovery is not going to take the economy back to where it was.

It may take stocks back to their last highs (and beyond!) but not the economy. Many people continue to think the stock market is a gauge of the economy, even though the stock market has never been more completely disconnected from economic reality than it is now. They will agree with Donald Trump when he says the economy has recovered because stocks have recovered. They’ll buy the narrative they want to believe without even questioning it.

Here’s the full truth: Reopening means businesses will start to show rapid improvement, and millions of jobs will certainly come back almost overnight. That’s half the truth. The other half, which investors and Trump supporters won’t see because they don’t want to, is that many businesses will not reopen, and many jobs will not come back.

But guess which half of the truth you get to see first? We’ll be deep into July before we start to see where the rapid recovery stalls out, and then it may take a little longer before investors start to see it because they don’t want to.

At some point this summer, it will be clear that jobs are topping out well below where they were at the start of the year. The economic recovery will look less V-shaped and more square-root (which starts out just like a “V’). Narratives will be concocted to explain that away as a brief lull, but reality will keep pushing in, just as I’ve said will happen.

Unemployment will remain high enough to still be considered typical of a recession because marginal businesses did not reopen (including particularly retail stores that were barely holding on). Government stimulus programs will start to wind down unless congress extends them, which will be less likely if the virus stays at bay. People who did not return to full employment will start to default on their mortgages when forbearance ends in July. Defaulting businesses will start to pile up, etc.

That’s a long slog, and where along that path the stock market finally gives up its delusions, I don’t know. Maybe it never does.

However, between now and then, reopening is almost guaranteed to shoot economic statistics up quickly. That’s because the one thing that is different between this huge crash and all previous ones like 1929 is that no previous big crashes had the possibility of the government just flipping the circuit breakers back on to restart the economy.

Because this was an instantaneous chosen economic shutdown, it can be a relatively quick turn-on, too. Yet, the breakers are being turned back on in phases, just as often is done when major factories restart. So, it may not be quite as immediate as it went down; but it will be quick … to a point! An then it will fail … along all the economic fault lines that the big jolt also reopened.

The reopening of businesses timed out perfectly for that moment when the Dow was pressed against its normal bear-market rally eight and was pushing against its 200-day moving average as a ceiling. The reopening came just in the nick of time to thrust the Dow (the market’s last holdout of the three most influential indices) through those stiff resistance barriers. So, we’ve broken through!

Had Trump chosen to keep the economy closed another month, I doubt all of the Fed’s pushing would have broken through those barriers because reopening gave a huge boost by giving investors hope that the worst is behind us now.

There should be a lot of major good news during the month of reopening, and the market has shown it will ignore all bad news anyway. Records will be broken in the good news ahead, which will symbiotically support the Fed’s stimulus efforts and the government stimulus efforts that are set to continue, at least, until mid-July.

The phantom “V”

So, the market may swell to its pervious highs and even beyond, but look out when the “V” in the economy stops rising because the “V” is a phantom.

What we have is a not a V-shape but a reverse tick shape: down huge and up a little (and even less than shown). Yes, at least it’s not still down. Yes, some more jobs will come back as reopening begins. But many sectors won’t, and once government payroll support schemes end we will see just how ugly things really are…. Nonetheless … equities up big: because bad news is good news for stocks and good news is also good news, apparently.

Even GDP growth will look great after the second quarter because it is measured quarter-on-quarter and annualized, so the third quarter may yield the best GDP growth we’ve ever seen. Trump will boast about it to salvage his election chances; but he’s the one who decided to shut the economy down. His supporters will believe it actually means something simply because they want to. Stock investors will focus on it as if the growth rate does mean something.

But look beneath the hood. Sudden growth in GDP, when it happens (and I’m telling you in advance it will in the third quarter), doesn’t mean a thing. It is nothing but a rapid retracement from an near instant restart of a near total shutdown. It’s really just math. If you turn off a massive number of things, then suddenly turn them back on, you get a huge jolt. The real issue is what broke in the jolt.

To see that, you’ll have to pay attention to total GDP, not GDP growth, because the total GDP line will remain well below where it was at the start of the year even though growth soars (just as we’ll see it plummeted deeply negative in the second quarter).

That means the overall size of the economy will remain well below what it was. Total GDP rarely sinks because population growth alone makes it greater every year, yet it already made a downtick in the first month of the year because the economy was already shrinking into recession before COVID-19 hit, just as I said it would:

Total GDP is different from the following GDP growth rate graph, which shows how much GDP changes from one quarter to the next:

Even on that graph, which the Fed has not updated since the beginning of the year (perhaps because it doesn’t want to show how much GDP declined, rather than grew, until it can also show how much it bounced back), you can see that the entire Trump presidency, with all its massive tax cuts and deficits, delivered paltry growth.

How long it will take the market to accept that the economic “V,” which would be shown in the total GDP graph if it happened (not the market “V”) was a mirage, I don’t know because the market is, after all, stupid. However, the economy’s long depression — a sustained dip below the level total GDP hit in the first graph at the start of year — will give the market many months after July in which it will have to maintain the fantasy without the benefit of the fantasy narrative that the initial reopening will deliver.

Will that eventually pound the point through the thick heads of investors? I think it will because reality has always won over market delusions in the past and because the Fed is now having to pump money at phenomenal rates just to avoid another repo crisis, let alone a stock-market collapse. However, investors will be able to fool themselves for awhile into thinking the “V” in the market proves a “V” in the economy, even though market and economy have totally decoupled.

Plenty of other statistics will be available, such as continued unemployment, to prove the economy did not put in a V-shaped recovery; but the market has proved adept at ignoring all statistics it doesn’t want to believe in.

The Fed is being supported by delusional belief in an ephemeral economic rebound that will disappoint and by government support; but even the Fed is tapering, and the stock market already showed at the start of the recent plunge that it was less willing to believe in the Fed and needed a lot more juice than it did in previous hard times.

So, trouble ultimately lies ahead for the market, too. The ones to really feel the trouble before investors will be the people who didn’t get their jobs back, business owners who didn’t weather through the lockdown, people walking mainstream who see more closed businesses.

The repo market is also, again, showing no forgiveness toward the Fed’s tapering, which I’ll come to.

Phantom facts are all we need now

The market soared last week because unemployment dropped as jobs rose. Of course jobs rose! No one (and I do mean “NO ONE”) thought all the jobs that went away would stay away when the lockdown was lifted.

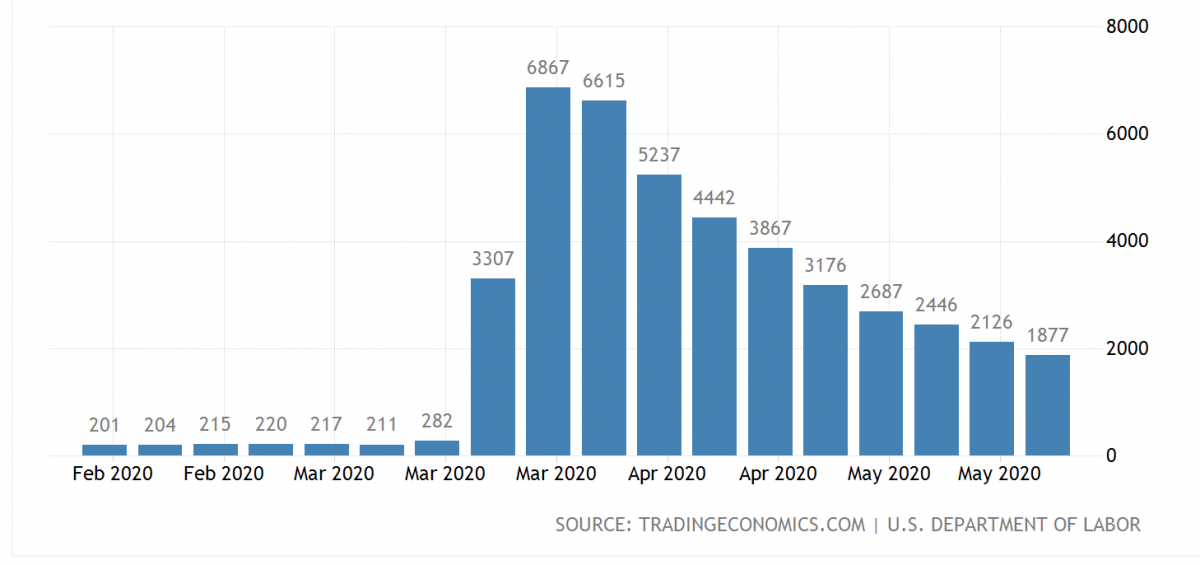

No one thought most of them would stay away or that they would be slow to start recovering. Obviously, after the biggest and most rapid job loss in history, as shown in the graph at the top of this article, the spike back up due to a return to work will also be the biggest job gain in history! So, expect a lot more job improvement to come.

However, the unbalanced stock market ignored the entire job-loss period, as if it didn’t matter, yet roared euphorically over the job-returning news as if it meant everything.

People who are not stupid, on the other hand, realized that enough of those jobs will ultimately stay away to leave the economy badly crippled for a long time to come:

Unemployment data this week is anything but promising, suggesting a V- shaped economic recovery is a pipe dream. Continuing jobless claims show people aren’t being rehired. Salary cuts across the board mean even those who have a job have less to spend.

Think about the following graph of NEW unemployment claims presented in the article just referenced:

As the article notes,

Unemployment data showed a decline in new claims, but the number of people filing is still outrageous.

Euphoric bulls aren’t thinking about that. They’re not thinking at all. They are driven by pure testosterone. The fact is, however, that 1.88 million NEW unemployment claims is massive for the start of reopening. In a normal world, that number would have been devastating news; but, because it looks so much better than the extraordinary bad news of the recent past that the market ignored, bulls took it as great news, which they didn’t want to ignore.

Wall Street bulls celebrated when this week’s unemployment data showed that new claims had fallen to 1.877 million. That’s the lowest they’ve been since lockdowns began….

There’s still an extraordinarily high number of people filing for unemployment benefits. Recall that before the pandemic rocked the U.S. economy, that figure ranged between 200,000 and 220,000….

It gets worse. That’s just the number of initial jobless claims— meaning people filing for the first time.

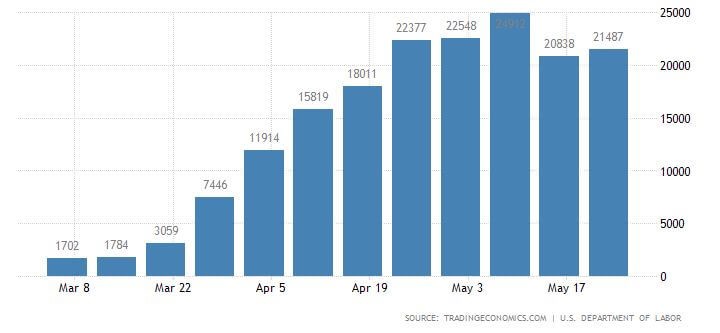

In fact, the number of continuing jobless claims actually rose, in spite of the decline in new claims:

The number of continuing claims suggests people aren’t being rehired. | Source: Trading Economics

A whopping 21.5 million Americans have yet to be rehired despite the fact that the U.S. economy is reopening….

The University of Chicago estimated that approximately 42% – or 9 million of those people – will remain unemployed. Other estimates suggest upwards of 16 million, or roughly 10% of the entire labor force, will continue to claim unemployment benefits for the foreseeable future.

Continued 10% unemployment sounds like a big, bad recession to me, but the stock market isn’t going to see the obvious until it happens. That means they won’t see it until unemployment stops going back down. Blind bulls may not even see it then; but, if they do, it will be quite a wake-up call.

Finally, the May jobs shocker was due to the CARES Act, which provided Payroll Protection money to employers to keep people on or put people back on their payrolls during the shutdown. That money runs out in July, and we don’t know how many of those people will stay employed when the money runs out. It’s not a normal kind of return to employment.

For the month ahead and into part of July, however, unemployment is nearly certain to go down, feeding delusional investors exactly the fantasy they want to believe in. Many other positive economic indicators will rise quickly as money starts to flow through businesses again.

The speed will feed the recovery narrative, but it’s not the speed that matters. A rapid bounce back up is quite likely. It’s where things level off that matters — how much many measures of the economy fall short of where they were at the start of year.

Total jobs will be an important number to watch (as well as the corollary of total unemployment). Adding to the pain of those real-world numbers, many of those jobs that are reopening are doing so with wage cuts.

It’s also a fairly reasonable bet, as Jim Bianco claims, that those losing their jobs now — just as the economy is going from shutdown back to reopening — represent permanent job losses:

Claims in 20 minutes. Consensus is 1.8 million

We are now 11 weeks into the shutdown and everything is restarting. If 1.8 million lose their jobs now, it’s a good bet these are permanent and not temporary furloughs.

Ditto the 2+ million that filed claims last week.

— Jim Bianco (@biancoresearch) June 4, 2020

This late in the game with employers fully knowing that reopening is happening, it is unlikely employers are laying people off due to the national shutdown and much more likely they are laying the off because they are shutting down their businesses in failure due to the national shutdown.

These are likely the zombie companies and other marginal companies that I said would not weather through the shutdown, already throwing in the towel. Otherwise, why lay people off just as shut-down orders are being lifted? These are either job losses from company closings or from corporate resizing to the new economy.

The pandemic isn’t finished with the U.S. labor market, threatening a second wave of job cuts—this time among white-collar workers.

Close to 6 million jobs are potentially on the line, according to Bloomberg Economics. That includes higher-paid supervisors in sectors where frontline workers were hit first, such as restaurants and hotels. It also includes the knock on-effects to connected industries such as professional services, finance and real estate.

“It will get worse before it gets better—white-collar workers will now bear the brunt,” said Yelena Shulyatyeva, senior U.S. economist at Bloomberg Economics. “Even if states and businesses reopen, we’re likely to see this second wave of losses,” since the labor market tends to lag economic activity, she said….

“Businesses are still operating in such an uncertain environment and they’re still adjusting to the new reality, and the new reality may be that you don’t need as many workers.”

This is what I’ve forecast from the start of the Great Shutdown.

In short, it ain’t over till it’s over.

Every company right now is busy figuring out how to do more with less.

And once they figure who the less is those jobs are not coming back.

— Sven Henrich (@NorthmanTrader) May 11, 2020

Prediction fulfilled: shell corporations trade as prized chips

The market has actually already entered the ultimate bizarre phase I said we would see if the Fed kept pumping and market bulls kept following their delusions about a V-shaped recovery.

Remember how I wrote several times that, if the Fed’s game continued, we would move to the point where bankrupt shell corporations would trade as trillion-dollar chips in the casino because the only thing left that mattered was the continued existence of their name as a place holder for bets?

Reality? Who needs it! We have a stock market, for cryin’ out loud! And if you have a stock market, you don’t even need an economy! Give me one good reason why stocks can’t exist and be traded like casino chips without a real business behind them when the market hasn’t paid a dime’s worth of attention to GAAP-based business numbers for years anyway. Just make it a stock market full of shell corporations that used to be real businesses, and keep betting their values up using free Fed money.

“If Bulls Had Wings They Could Fly; Without Them They’ll Die!” April 9, 2020

Even in the extraordinary event the market does keep going up, in spite of the endless outpouring of historically atrocious economic news … all that means (as I said before) is the S&P 500 is going to become a list of revenue-stripped shell corporations… and what does that matter … because they’ll just be meaningless chips in a casino — nothing left but space holders for a bet? It will become the most meaningless market in history.

“Wall Street Bulls Battle the Bears in Mother of All Recessions” April 15, 2020

As company values crash in terms of price-to-sales ratios or revenue or earnings or forward guidance or any business metric you want to apply, the Fed wants to make sure that stock prices are never true valuations again. That means we could soon have the scenario where mere shell corporations trade as trillion-dollar chips in the Wall-Street casinos.

Ask yourself one common-sense question: if it doesn’t matter for stock-trading purposes whether or not corporations have any actual business income under the coronavirus shutdown, does it even matter if they actually exist? So long as their name exits, why not keep betting them up?

“Fiercest Economic Collapse in History is Best Month for Stock Market” May, 1, 2020

Well, we’re there! Not at the trillion-dollar level yet, but we live in the center of a diseased brain where bankrupt corporations — mere shells of their former selves — are skyrocketing as prized chips in the Wall Street Casino:

This market is so bullish even bankrupt companies are rallying.$HTZ pic.twitter.com/TPMh0wyay1

— Sven Henrich (@NorthmanTrader) June 5, 2020

The move in stock of bankrupt Hertz has gone absolutely parabolic, with the stock rising as high as $6.25, nearly triple its Friday close…. As a reminder, the stock was trading at 80 cents just last Thursday, returning approximately 800% in the past three trading days … sending the company stock soaring even though it is patently worthless….

As for Hertz, we hope the company’s sells a few hundred million worth of stock – after all there is apparently endless demand for its shares…. Joking aside, we hope that at some point the regulators (remember them) will step in and put an end to this insanity before too many gamblers lose their life savings….

Nothing screams “buy” in this Wonderland rabbit hole of a world like bankruptcy! Just give me a good shell corporation I can trade on the market boards. In this whirling dervish of a casino, you can buy bankrupt Hertz and see nearly ten times your money over the weekend! The stock is up 1,450% since the company declared bankruptcy.

The Fed supplies the money needed to keep the casino open, while the reopening supplies the fantasy fiction needed to keep the bets coming.

It’s the mother of all “money illusion” rallies. In 3 months, the Fed juiced up M2 by a cool $2.5T, and the S&P 500 mkt cap surged dollar for dollar. Who needs earnings? Who needs productivity? Who even needs buybacks anymore? MMT arrived early and with a Republican in office!!

David Rosenberg | Source: Zero Hedge

So, why would I risk betting on stupid?

Because stupid is a pretty safe bet right now. The only caveats to all of this for the next month or two will be if the flow of superficial good news from reopening causes the Fed and government to rapidly back down on the support the market is fully dependent on (unlikely) or if the coronavirus returns this summer with a vengeance due to reopening, instead of waiting until normal flu season (unpredictable but not too unlikely).

To keep all of this in perspective, realize that the economy’s steep climb from record job losses is just the completion of the first “V” in a “W” or in square-root symbol. If a square-root symbol, even that will ultimately fail, turning into nothing but a short plateau, when we fall back off the other end.

Don’t mistake the shape of the stock market, which may well be a full “V,” for the shape of the economy; but do know that the market has always corrected back to the economy in the past, and the economy is in deep trouble. That is where the Fed is particularly dead. Even if it pumps up stocks, it can’t save the economy because its earlier recovery plans, which it is now replaying, created a lot of the economy’s trouble in the first place, and those plans have about run out of gas.

So, the market is stupid because it is actually betting on the “V.” It believes in the “V.” I don’t, and I’m not betting on the “V.” I’m betting on stupid, and that seems like a pretty safe bet right now. I’m betting that the reopening yields enough record good news to feed the delusion until the stimulus funding starts to dry up and the knock-on effects of the shutdown start to show up and the virus eventually returns or the repo crisis returns in full force.

The return of the coronavirus in full force could be extremely soon with so much social narrowing and mixing during the George Floyd protests that are taking us back into the Civil War, which have made it OK for Democrats to doff their masks and gather together in the thousands. Give that a two-week gestation period.

While I try to surf the wave of peak stupidity in the belief that this month and, at least, part of next will provide plenty of surge to keep the wave going, I will be looking for the end of the reopening surge as the point to jump back off or the return of the COVID surge.

As for that repo crisis, now that the Fed is turning down the quantitative-easing tap to a mere 50% higher flow than under QE3, the Repocalypse has already returned. The latest Fed overnight repo trade saw over a $100 billion in takers. Apparently 1.5x QE3 isn’t enough to keep markets liquid in Bozoland. It may be the bond market’s turn to go down before the stock market makes it next dive.

That’s why I’ve claimed since September, “It’s QE4ever now, Baby!”

And that’s the way it is!

*********

David Haggith started writing about the economy after he predicted The Great Recession half a year before it hit and was puzzled as to why no economists or stocks analysts saw it coming. In the months after the crisis broke out, he started to write humorous editorials in a series titled “Downtime,“ which chided the U.S. government and bankers who should have seen the economic collapse coming but whose cronyism, greed and ineptitude caused them to run the world into a ditch. Those articles were published in The Hudson Valley Business Journal, The Valley City Times-Record (North Dakota), and The Daily Herald in Tennessee. Haggith is dedicated to regularly criticizing the daily news — not just the content but the uncritical, unthinking nature of almost all of the reporting. He now writes his own blog, The Great Recession Blog, to break down the news as an equal-opportunity critic toward both Republicans and Democrats / Conservatives and Liberals … since neither kind of politician has done anything worthwhile to plot a better economic course. His articles are regularly carried by several economic websites.

More from Silver Phoenix 500