No More Copper Surpluses

Every year the experts predict a copper surplus; instead, what happens? Deficit after supply deficit.

That’s because the copper market is subject to so many variables external to regular mining operations. That includes strikes and community unrest that sometimes leads to blockades, then you can add; droughts, flooding, earthquakes and production snafus such as lower-than-expected ore grades.

There are a lot of things that can cause global copper production to take a hit.

In 2023, the government of Panama ordered First Quantum Minerals to shut down its Cobre Panama operation, removing nearly 350,000 tonnes from global supply.

A strike at another large copper mine, Las Bambas in Peru, temporarily halted shipments.

Yet the International Copper Study Group said at the end of April 2025 that:

“The global copper market is expected to see a significant surplus over the next two years as the negative impacts of US tariffs on demand outweigh supply growth, the International Copper Study Group (ICSG) said in its latest forecast.

The Group, which recently concluded its biannual meeting with key industry players in Lisbon, forecasts global copper surplus to reach 289,000 tonnes in 2025, more than double the 138,000 tonnes from last year. This forecast also represents a larger surplus than its earlier projection of 194,000 tonnes.”

So, we already know that the ICSG’s forecasted surplus will be off. Let’s face it, it’s an insignificant number to begin with – 289,000 tonnes are approximately 1.33% of global copper supply in a year. The slightest problem occurring out of all those problems listed above, and suddenly, the world has a copper deficit.

Earlier this month, the giant Kamoa-Kakula copper mine in the Democratic Republic of Congo had to stop underground operations due to flooding resulting from a large earthquake in the region.

On May 29 it was reported that seismic activity caused widespread flooding deep below ground, with water levels rising after pumping and electrical infrastructure was damaged.

Bloomberg said the impacted mine accounts for at least 70% of the complex’s current production, and that the flooding could shut the Kakula underground operation until at least the fourth quarter.

The complex was on track to become the third-largest supplier of copper in the world, having begun commercial production on July 1, 2021.

It was at first difficult to get accurate information regarding the incident, which happened on May 18. Part-owner Ivanhoe Mines reported on May 20 that two days earlier it had temporarily suspended operations at Kakula underground following seismic activity.

Bloomberg said a lot of water had entered the mine and that workers were prohibited from going underground. Kakula’s Chinese owners Zijin Mining, which controls 39.8% — the same as Ivanhoe — said there was a roof collapse, and that full-year production would likely be impacted.

Ivanhoe disputed this, saying via Bloomberg there was no evidence of collapsing stopes or structural pillars. But within days, Ivanhoe withdrew its 2025 output guidance of 520,000-580,000 tons at Kamoa-Kakula. In April, Ivanhoe produced a record 50,176 tons from the mine.

With only sparse information to go on, analysts have estimated that 84,000 to 275,000 tons of copper output could be lost this year. That would potentially wipe out a sizable chunk of the 289,000-ton global surplus forecast for this year by the International Copper Study Group.

Note that surface operations have been unaffected; Kakula’s concentrator facilities can reportedly process sizeable surface stockpiles.

Ivanhoe put out a press release on Monday, June 2nd saying that Kamoa Copper plans to resume operations on both the western and eastern sides of the Kakula Mine. Subject to dewatering progress, underground mining is expected to restart later this month on the western side of the mine, which remains dry and supported by over 1,000 litres per second of operational pumping capacity.

Stage One involves the installation of temporary underground pumping infrastructure to stabilize and maintain current water levels…

Stage Two involves the installation of high-capacity, surface-mounted pumps and new permanent infrastructure to fully dewater the entire Kakula Mine…

Meanwhile, the Phase 1 and 2 concentrators continue to operate at approximately 50% of their combined capacity, processing ore from surface stockpiles.

Huge copper supply deficit looming

S&P Global produced a report in 2022 projecting that copper demand will double from about 25 million tonnes in 2022 to 50Mt by 2035. The doubling of the global demand for copper in just 10 years is expected to result in large shortfalls — something we at AOTH have been warning about for years.

The US ranks second-last globally in terms of required lead times for new mines — 29 years, just ahead of Zambia’s 34 years. Potential new copper mines face permitting challenges. For example, development of Rio Tinto and BHP’s massive Resolution copper mine in Arizona is on hold, facing opposition from native Americans. (Although the Supreme Court recently declined to hear an appeal from the Apache tribe seeking to block development of the mine.)

US copper production dropped 3% last year from 2023, following an 11% decline that year.

Demand

Global copper consumption has increased steadily in recent years and currently sits at around 26 million tonnes. 2023’s 26.5 million tonnes broke a record going back to 2010, according to Statista. From 2010 to 2023, refined copper usage increased by 7 million tonnes.

Wall Street commodities investment firm Goehring & Rozencwajg quoted data from the World Bureau of Metal Statistics confirming that global copper demand remains robust, outpacing supply.

The shift to renewable energy and electric transportation, accelerated by AI and decarbonization policies, is fueling a massive surge in global copper demand, states a 2024 report by Sprott.

Increasing investments in clean technologies like electric vehicles, renewable energy and battery storage should cause copper demand to climb steadily, and challenge global supply chains to meet this demand. Artificial Intelligence, data centers, 5g, global infrastructure build out and a global effort to rearm the world’s militaries all contribute to increased copper usage. And than there’s an expected copper demand push to achieve ‘use parity per capita’ by the vast majority of the world’s population, which I explore later in the article.

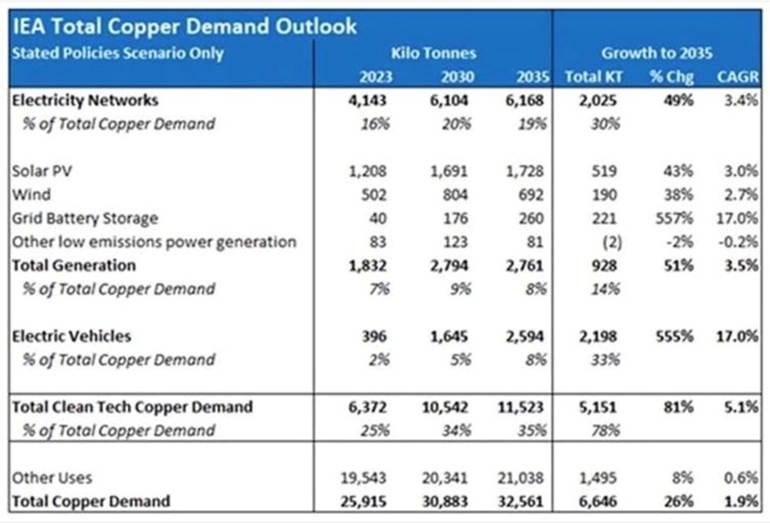

The report cites figures from the International Energy Agency (IEA), such as global copper consumption growing from 25.9 million tonnes in 2023 to 32.6Mt by 2035, a 26% increase. Clean tech copper usage is expected to rise by 81%, from 6.4Mt in 2023 to 11.5Mt in 2035.

Source: International Energy Agency (IEA)

The IEA expects the copper needs from electricity networks to grow from 4.1Mt in 2023 to 6.2Mt by 2035, an increase of 49%. Copper demand for solar panels is expected to rise by 43% and for wind power by 38% over the same period.

The fastest-growing area, though, is grid battery storage, where copper demand is expected to surge by 557% to 2035 as the need for energy storage increases, Sprott writes.

Copper demand for EVs is a close second, with a projected rise of 555% from 396,000 tonnes in 2023 to 2.6Mt by 2035, with EVs accounting for 8% of global copper consumption by that year.

BHP foresees global copper demand increasing by 70% to reach 50 million tonnes annually by 2050.

Supply

On the supply side, BHP points to the average copper mine grade decreasing by around 40% since 1991. The next decade should see between one-third and one-half of the global copper supply facing grade decline and aging mine challenges. Existing mines will produce around 15% less copper in 2035 than in 2024, states the company.

“Most of the high-grade stuff’s already been mined,” says Mike McKibben, an associate professor emeritus of geology at University of California, Riverside, quoted recently by NPR. “So, we have to go after increasingly lower grade material” that costs more to mine and process, he says.

Shon Hiatt, a business professor at the University of Southern California, said, “It’s projected that in the next 20 years, we will need as much copper as all the copper that has ever been produced up to this date.”

Mining Technology reports that global copper production in 2024 was poised to reach a new high of 22.9Mt, a 3.2% increase from 2023. A confirmation is provided by the US Geological Survey, which showed mine production in 2024 of 23Mt, 600,000 tonnes more than 2023.

The supply increase is being driven by expansions at key mining operations in several countries including Chile — the top producer — the DRC, Russia, Zambia and China.

Mining Technology notes Chile was set to see a substantial bump in 2024 output thanks to the expansion of Teck Resources’ Quebrada Blanca mine — 252,200 tonnes compared to just 62,700t in 2023, a 303% increase.

GlobalData forecasts a CAGR of 4.2% for global copper production, reaching 29.3Mt by 2030. Note from above, however, the IEA predicts global copper consumption reaching 32.6Mt by 2035, creating a potential shortfall of 3.3Mt.

Source: World Copper Factbook 2024

Deficit

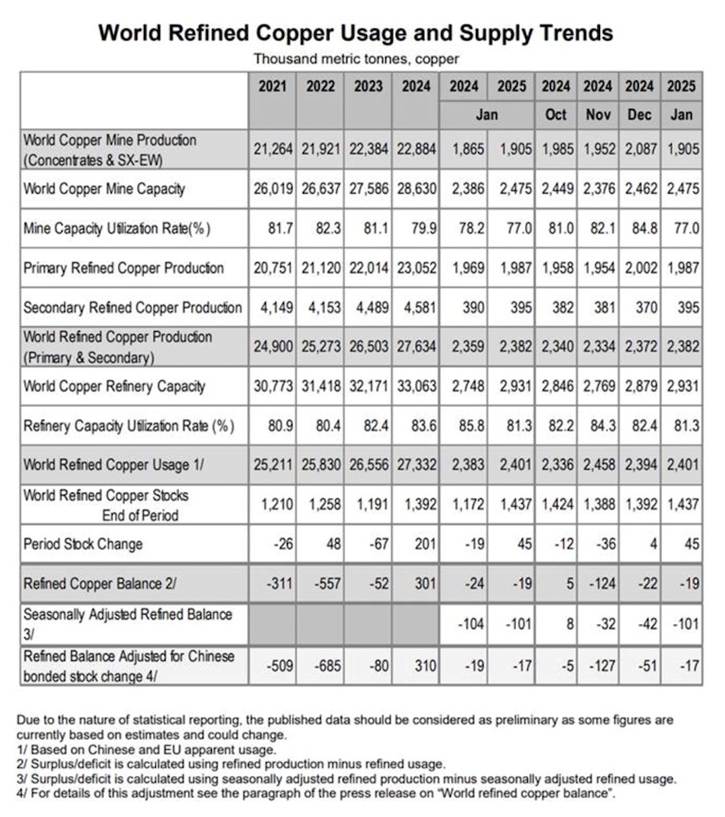

Full-year 2024 copper supply figures are available from the International Copper Study Group. In its January report, the ICSG shows a slight increase in world copper mine production, 22.884 million tonnes in 2024 versus 22.384Mt in 2023.

Last year saw a surplus of refined copper production, 301,000 tonnes, determined by subtracting world refined copper usage of 27.332Mt from world refined copper production of 27.634Mt.

Source: International Copper Study Group

However, that could change as early as this year.

According to Swiss bank UBS, via EV Magazine, the current copper surplus will swing to a deficit exceeding 200,000 tonnes in 2025.

What could cause the copper market to fall into a large deficit hole from which it would be very difficult to climb out of? There are several factors.

Last year S&P Global commissioned a report that blamed the shortfall on underinvestment in new exploration and mines due to the industry’s focus on short-term returns (NPR)

It noted the copper industry faces pressures from the need to decarbonize itself; political instability in many countries which mines are located; and reputational damage from its history of safety and environmental failures. The latter means the industry is now under greater scrutiny from regulators and community groups.

The firm predicts copper supply will be unable to keep up with demand from as early as 2025; demand could double to 50Mt by 2035.

In a piece by the International Energy Forum (IEF), Goldman Sachs found that regulatory approvals for new mines are on a downward trend, having fallen to the lowest level in 15 years, which is particularly disturbing since it can take 10 to 20 years to approve and develop a mine in North America.

Another factor behind depleting copper supply is a lack of new discoveries.

According to Crux Investor, citing S&P Global Commodity Insights, despite a 12% increase in exploration budgets in 2023, the industry has seen only four major discoveries in the past five years (2019-2023), totaling a mere 4.2 million metric tons (MMt) of copper. This marks a significant downturn in the frequency and size of major discoveries compared to previous decades.

What’s behind this trend? Crux says companies are increasingly focused on brownfield (past-producing) assets rather than engaging in greenfield exploration that could yield new, large-scale discoveries. Early-stage exploration budgets have dropped to a record low of 28%, compared to the 50-60% allocation that was typical in the 1990s and early 2000s.

Crux says the copper market is heading towards a significant supply-demand imbalance, making the following supporting points:

- A refined copper deficit is projected to begin in 2027

- The concentrate market is currently in deficit and expected to remain so for the next five years

- Mine supply is forecast to peak in 2029

A potential concentrate deficit of 2.2Mt is expected by 2032.

The International Energy Agency believes existing mines and projects under construction will only meet 80% of copper needs by 2030.

“There’s this growing consensus that demands fueled by the energy transition is going to outstrip supply and that’s why analysts are now saying we’re simply not going to have enough of it,” says Pippa Stevens, markets reporter, in a 2024 CNBC video on the coming copper shortage.

The video says it is very difficult for existing mines to even maintain current levels of production. To keep up with demand, the industry is faced with several obstacles including a shortage of mine workers, navigating regulatory hurdles and dealing with pushback from local stakeholders.

Moreover, most of the “low-hanging fruit” has already been mined.

“High-grade economic copper resources are not abundant, these things aren’t all over the place, you have to go find them,” said Chris LaFemina, global metals and mining analyst at Jefferies.

Inflation and the high costs associated with building a new mine are also deterrents.

“It’s so capital intensive, you need to invest billions upfront for a payout that might take 10 or 15 years to come in the future and by that time who knows what the economic landscape, the political landscape will look like and so it’s hard for investors to give the green light for that,” says Stevens.

The video concludes that demand may already be starting to outweigh supply: the amount of copper needed in the 28 years between 2022 and 2050 will exceed the amount consumed between 1900 and 2021.

While copper is abundant globally, only a fraction can be extracted cost effectively at today’s prices and with current technology.

Sprott said in a 2024 ‘Insights’ report that Chile and Peru, the top copper-producing countries, are grappling with labor strikes and protests, compounded by declining ore grades. Russia, ranked seventh in copper production, faces an expected decline due to the ongoing war in Ukraine.

Despite efforts by miners to ramp up production, many analysts anticipate a widening supply imbalance.

The degree to which the industry has failed to bring on new mines is evident in a study by the University of Michigan and Cornell University. The researchers found that copper can’t be mined fast enough to keep up with current US policy guidelines to make the transition from fossil-fueled power and transportation to electric vehicles and renewable energies.

How impossible? The researchers found between 2018 and 2050; the world will need to mine 115% more copper than has been mined in all human history to 2018. This would meet our current copper needs and support the developing world without considering the green energy transition.

To electrify the global vehicle fleet requires bringing into production 55% more new mines. Between 35 and 195 large new copper mines would have to be built over the next 32 years, at a rate of up to six mines per year. Spoiler alert – not going to happen, in other words an impossible task. In heavily regulated environments like the United States and Canada, it can take up to 20 years to build one mine from scratch.

Source: International Energy Forum

“We show in the paper that the amount of copper needed is essentially impossible for mining companies to produce,” said Adam Simon, a professor of earth and environmental studies at the University of Michigan.

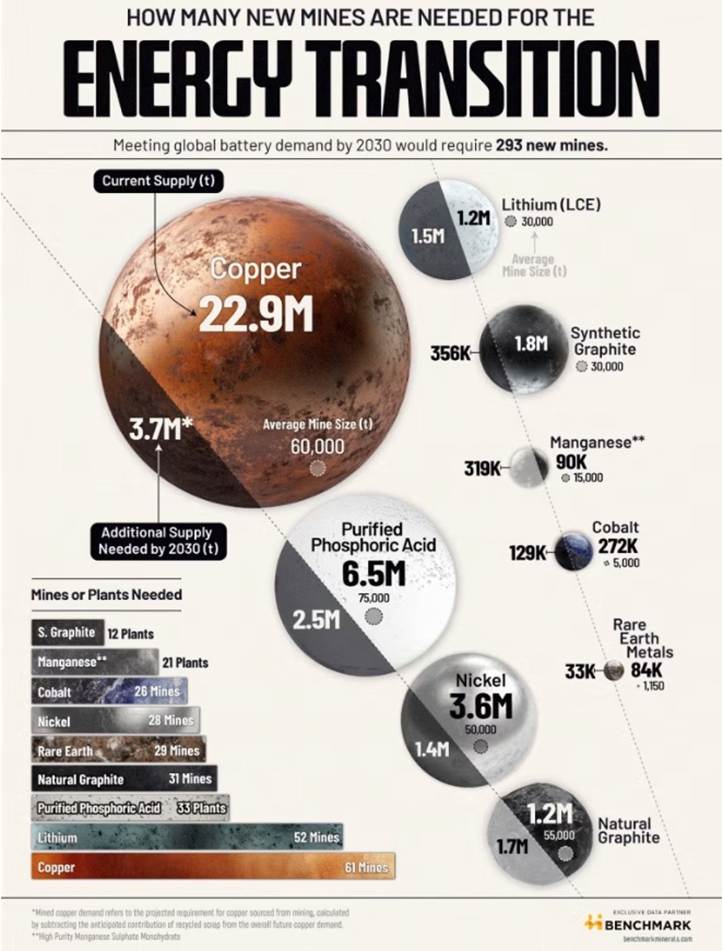

According to Benchmark Intelligence, meeting global battery demand by 2030 would require 293 new mines. Source: Benchmark Mineral Intelligence

The researchers recommend that instead of building electric vehicles, the car industry should concentrate on hybrids, which use less copper — about 88 pounds versus 200 lbs for a fully electric EV.

“Instead of producing 20 million electric vehicles in the United States and globally, 100 million battery electric vehicles each year, would it be more feasible to focus on building 20 million hybrid vehicles?” Simon said.

Even meeting baseline demand won’t be easy. The study calculated that 60-plus large mines each yielding 500,000 tonnes a year must come online before 2050 just to keep economic growth on track. For investors to green-light new pits, the copper price would have to trade about $20,000 per tonne — more than double 2024 levels.

Another alarming statistic from the University of Michigan study is that continuing “business as usual” population growth and rising standards of living would consume about 1,100 million tonnes of copper by 2050. Mines globally produced 23 million tonnes in 2024, barely 2% of what the world will burn through over the next 25 years. (Earth.com)

The excessive demand numbers are likely to force policymakers to make some difficult decisions: meet climate goals or meet the needs of developing nations — i.e., not both. Transitioning every passenger vehicle to electric power using copper-based components pushes demand to 1,248 million tonnes. You want wind and solar? Copper demand increases to 2,304 million tonnes. Building an electrical grid that stores energy in battery packs raises the tally to 3 billion tonnes.

Meanwhile, emerging economies require more of the red metal. India for example will need about 227Mt to expand power lines, hospital and sanitation system, Earth.com points out.

The forty-plus nations of Africa could require around 1 billion metric tons to build comparable infrastructure.

Copper parity

The current global population is 8.2 billion.

Another 0.9 billion people will be added to the world by 2050. Most will not be Americans, but they are going to want a lot of things that we in the Western, developed world take for granted — electricity, plumbing, appliances, AC etc.

“Infinite growth of material consumption in a finite world is an impossibility.” — E. F. Schumacher

“We’re living in a finite world, one in which resource constraints are becoming increasingly binding.” — Paul Krugman, ‘The Finite World’

What if all these new consumers were to start consuming, over the next 10 years, just like an American? What’s going to happen to the world’s mineral resources if one billion more “Americans” are added to the consuming class? Here’s what each of them would need to consume, per year, to live the American lifestyle:

In 2020, 40,633 pounds (20.3 tons) of minerals and fuels were needed per person to maintain the American lifestyle.

According to the National Mining Association every American consumed the following amounts of minerals in 2020.

2020 US per capita use of minerals – source: National Mining Association

Can everyone who wants to, live an American lifestyle? Can everyone everywhere else have everything we in North America have? The answer is a resounding no!

Even if we mined every last discovered, and undiscovered, pound of land-based copper, the expected 8.2 billion people in the developing world by 2050 (out of 9.1 billion total) would only get three quarters of the way towards copper use parity per capita with the US.

Of course, the rest of us, the other 0.9 billion people expected to be on this planet by 2050, aren’t going to be easing up, we’re still going to be using copper at prestigious rates while our developing world cousins play catch-up.

Adam Simon, from the University of Michigan study cited above, points out the disparity in copper use between wealthy and developing nations:

Over the course of the 20th century, the United States progressed from having no electricity or plumbing to becoming a copper-intensive society, with more than 400 pounds of copper per person embedded in homes and infrastructure.

In contrast, Simon estimates that in countries like India, the figure is closer to just 40 pounds per person.

Source: World Copper Factbook 2024

Copper use parity isn’t going to happen, it can’t.

Despite what mainstream analysts say, copper is already in a very real structural supply deficit. Most just don’t know it.

Let’s state the obvious:

- For over the last 16 years supply has struggled to keep pace with demand.

- Metal supply is finite and subject to compounding demand from developing nations.

- Metal production is highly cyclical, with intermittent peaks and troughs which are intricately linked to economic cycles. Declining production has historically been driven by falling demand and prices, not by scarcity.

- Rates of production and reserve amounts continually change in response to market movements and technological advances.

- If energy was cheap and unlimited, recoverable resources would be unlimited.

But

- Discovery and development is increasingly becoming more challenging and expensive.

- Average ore grades are in decline for most minerals, yet production has increased dramatically.

- Our most important metals are suffering from declining ore quality and rising extraction costs.

- Our prosperity has always been based on the fact that producing resources yielded more resources than costs. However, the cost of energy and the amount used are climbing but the returns from energy expended is declining. Eventually the quantity of resources used in the extraction process will be 100% of what is produced.

- Most older mines, the foundation of our supply, have increasing costs, with production rates stagnating or even declining.

- The rate of discovery is not keeping pace with the rate of depletion, let alone being higher.

Conclusion

The world’s exploding population, the massive shift from rural to urban, the growth of a consumption-minded middle class in developing countries, is all happening now.

Add in finite, increasingly hard-to-find resources.

The effects will be felt long before we start to run out of copper and there will be severe consequences:

- Rising energy and commodity prices

- A decline in the global economy

- Civil unrest

Perhaps the two biggest reasons to be bullish on copper are one, the massive costs and risks involved in finding and opening new mines in often geopolitically risky countries where a miner’s social license to operate is shaky at best.

And reason two concerns what has been going on regarding a loss of funding for junior exploration. A dearth of exploration capital in recent years is making it increasingly difficult for copper mining companies to replace their reserves. We are optimistic to see junior drill programs finally beginning to get funding, this year.

Not helping copper’s cause is the army of experts that trot out supply surplus predictions that nearly every year turn out to be wrong. Events out of the industry’s control frequently occur; the underground flooding at the Kakula mine is a case in point. Remember this statistic? 84,000 to 275,000 tons of copper output could be lost this year, potentially wiping out a sizeable chuck the 289,000-ton global forecast this year by the International Copper Study Group.

We can almost guarantee that Kakula won’t be the only copper mine to come up short on production. Strikes, bad weather, force majeure, poor grades are some of the reasons why a surplus will not materialize.

According to Swiss bank UBS, via EV Magazine, the current copper surplus will swing to a deficit exceeding 200,000 tonnes in 2025.

And let’s bring up another statistic never quoted by copper bears:

For investors to green-light new pits, the copper price would have to trade above $20,000 per tonne, or $9.07 per pound — more than double 2024 levels.

On Monday copper surged nearly 6%, following Trump’s announcement on Friday that he plans to double tariffs on steel and aluminum to 50% on Wednesday, along with a weaker dollar. Mining.com said the threats raised concerns over the fate of copper which may also be facing a tariff.

Copper per pound. Trading Economics

Years ago, the US Geological Survey put out a report stating that if the developing world were to catch up to the developed world, we wouldn’t even get to the starting point before we ran out of every pound of copper. That report disappeared off the internet but there is no doubt in my mind that the copper crunch is going to be one of the worst metal scarcities because of structural supply deficits.

Even the “business as usual” scenario — not increasing copper consumption for electrification, 5G, AI, or building more copper capacity in the developing world — would consume 1.1 billion tonnes by 2050. Last year, mines only managed to produce 23 million tonnes, barely 2% of what the world will need to burn through over the next 25 years – without forgoing many of the things we want.

We have clearly reached the point where we need to build new copper mines and to relax permitting rules that are unfriendly to mining in restriction-heavy jurisdictions like Canada and the US. In this respect, we are encouraged by President Trump’s executive order to boost American mineral production and streamline permitting.

The BC government just passed Bill 15, the Infrastructure Project Act, which is aimed at fast-tracking public sector projects like schools and hospitals, as well as private projects such as critical mineral mines, that are deemed provincially significant. (CBC News)

Prime Minister Mark Carney’s Liberal government is preparing to table legislation that would fast-track projects deemed to be in the national interest, having met with the premiers in Saskatoon on Monday to pitch their ideas for “nation-building projects.”

Cross-country oil pipelines and a proposed “energy corridor” have become part of the national conversation in the face of punishing tariffs on Canada by the Trump administration. The country is looking to diversify trade to markets beyond the United States, which up to now has been Canada’s largest trading partner by a long shot.

Carney wants Canada to be an “energy superpower” and building new copper mines would be a significant step in that direction.

I expect to see copper as the next must own metal for both investors and large miners. There will be a huge increase in the sector’s M&A. In my opinion the best way for me to invest is find a couple of undervalued junior resource companies. After all, the best leverage the best exposure historically, to increasing prices and M&A is to own the shares of juniors.

Richard (Rick) Mills

aheadoftheherd.com

*******

More from Silver Phoenix 500