Record High Markets, Despite Poor Jobs Report

The markets closed the week at record highs and booked weekly gains for the fourth time in five weeks. This comes despite a disappointing U.S. jobs report.

News Recap

- The Dow Jones gained 248 points, or 0.83, the S&P 500 gained 0.9%, and the Nasdaq advanced 0.7%. All three indices posted both intraday and closing record highs. Meanwhile, the small-cap Russell 2000 also closed at a record high and once again led the markets with gains of 2.2%.

- The November jobs report grossly disappointed and came well short of estimates. The report stated that the U.S. added 245,000 jobs compared to the consensus estimate of 440,000.

- November’s unemployment rate matched expectations and fell to 6.7% from 6.9%.

- The US trade deficit widened to $63.1 billion in October from a revised $62.1 billion. Market expectations placed this number at $64.8 billion.

- New data was encouraging for US factory orders. New orders for US manufactured goods beat expectations and jumped 1% from a month earlier. This marks the 6th consecutive month of rising factory orders.

- As COVID-19 numbers continue to reach record highs in new infections, single-day deaths, and hospitalizations, a report from Thursday that Pfizer may have issues rolling its vaccine out was quite concerning . Judging by the markets’ performance on Friday, however, investors are not overly concerned.

- Stimulus talks continued for another day as Republicans and Democrats attempted to break a stalemate and pass a relief package before the end of the year.

- Chevron and Caterpillar each rose 3.9% and 4.3%, respectively, and led the Dow higher.

- Energy was the best-performing S&P 500 sector, gaining 5.4%.

- Friday’s jump led to the major indices booking their fourth weekly gain in five weeks. The Dow rose 1%, the S&P 500 gained 1.7%, and the Nasdaq rallied 2.2%. The Russell 2000 also gained over 2% this week.

In the short-term, there will be optimistic days where investors rotate into cyclicals and value stocks, and pessimistic days where there will be a broad sell-off or rotation into “stay-at-home” names. On other days, like Friday, the markets will broadly rise without any one specific catalyst.

In the mid-term and long-term, there is certainly a light at the end of the tunnel. Once this pandemic is finally brought under control and vaccines are mass deployed, volatility will surely stabilize, and optimism and relief will permeate the markets. In fact, CNBC personality Jim Cramer said that beating COVID-19 would feel like “the end of prohibition.” Stocks especially dependent on a rapid recovery and reopening such as small-caps should thrive.

Markets will continue to wrestle with the negative reality on the ground and optimism for an economic rebound in 2021. While more positive vaccine news continues to trickle in day by day, there is still discouraging COVID-19 news, economic news, and geopolitical news to consider. Amidst the current fears of a double-dip recession with further COVID-19-related shutdowns and no stimulus, it is very possible that short-term downside persists. However, it’s encouraging that Democrats and Republicans are speaking again, and if a stimulus deal passes before the end of the year, it could mean more market gains.

Due to this tug of war between good news and bad, any subsequent move downwards will likely be modest in comparison to the gains since the bottom in March and since the start of November. It is truly hard to say with conviction that another crash or bear market will come. If anything, the constant wrestling match between sentiments will keep markets relatively sideways.

Therefore, to sum it up:

While there is long-term optimism, there is short-term pessimism. A short-term correction is very possible, but it is hard to say with conviction that a big correction will happen.

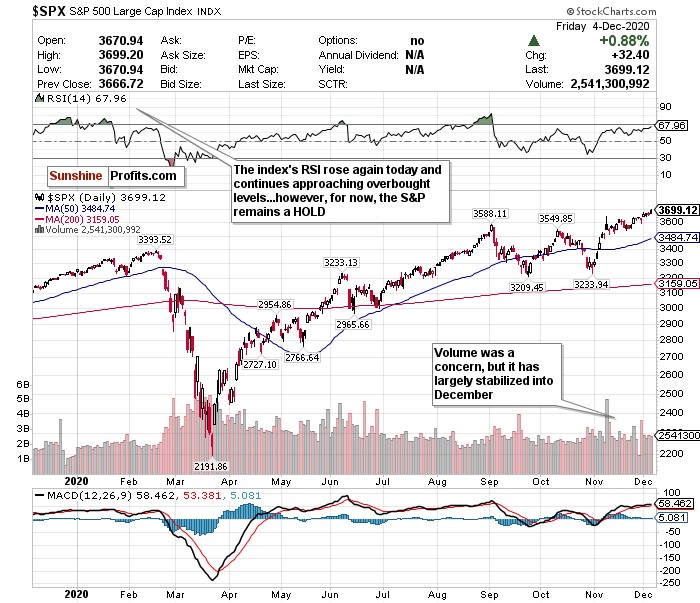

The S&P, which has seen three record closing highs this week, has skyrocketed to unprecedented levels at a breakneck pace. However, there are a few indicators that show that the S&P could face some near-term volatility after this run, but again, it is hard to say with conviction there will be a major downturn.

The RSI of 67.96 keeps the S&P in a HOLD category. However, it is certainly higher than it was to start the week and continues creeping towards an overbought 70 level.

The volume has stayed relatively stable since Thanksgiving though. While the sharp decline in volume after November 9th was concerning, especially relative to its record closes, the stabilization is encouraging.

Low volume, especially a sharp drop in volume, means that there are fewer shares trading. Lower volume also means less liquidity across the index, and an increase in stock price volatility. Therefore, this stabilization of volume adds some confidence in the volatility of the index.

Because of how far and fast the S&P 500 has risen, a further pullback from these elevated levels would not be a shock… but another surge based on good news would not be a shock either. Because of all of the uncertainty, a HOLD for the S&P is an appropriate call. For an ETF that attempts to directly correlate with the performance of the S&P, the SPDR S&P ETF (SPY) is a good option.

Thank you for reading today’s free analysis. I encourage you to sign up for our daily newsletter - it's absolutely free and if you don't like it, you can unsubscribe with just 2 clicks. If you sign up today, you'll also get 7 days of free access to the premium daily Stock Trading Alerts as well as our other Alerts. Sign up for the free newsletter today!

Matthew Levy, CFA

Stock Trading Strategist

Sunshine Profits: Effective Investment through Diligence & Care

* * * * *

All essays, research, and information found above represent analyses and opinions of Matthew Levy, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Matthew Levy, CFA, and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Levy is not a Registered Securities Advisor. By reading Matthew Levy, CFA’s reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading, and speculation in any financial markets may involve high risk of loss. Matthew Levy, CFA, Sunshine Profits' employees, and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

********

More from Silver Phoenix 500