The Recurring Money Retirees Need

When you retire, your investment goals change. It is one thing to build a portfolio of unrealized gains and reinvest all of your gains when you are still earning an income. However, it is a very different ball-game when you start withdrawing money from your investment accounts. Most retirees require a certain amount of income from their retirement accounts and that income needs to be predictable.

The Income Method is a great investment strategy for anyone. Building an income stream can be a very powerful tool in your portfolio. For retirees, it is essential. You need income today, you will need income tomorrow and you need to make sure you have enough indefinitely. Today we are covering the application of the immediate income approach over a large span of time in the view of retirement vs. other options available to retirees.

Buying and holding immediate income, high-yield stocks and securities can provide retirees a steady, reliable income stream in the face of increased market volatility. Choosing, sound income-producing securities, is essential to having peace of mind.

Non-Stock Options Yield Too Little

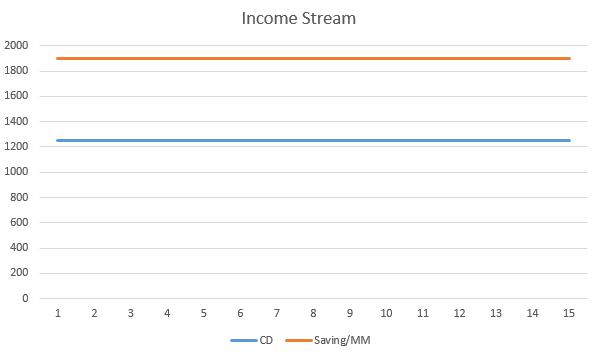

One option that many retirees consider when reaching retirement is leaving the stock market for quieter shores - non-equity options. Placing their hard-earned cash in certificates of deposit for example or money market accounts. Sadly these options yield next to nothing when it comes to trying to live on interest alone - although they're the lowest level of risk. According to Bankrate.com (with who we have no relationship) CDs on the high side average a yield of around 1.25%, but that requires locking away the principle where you cannot touch it. Savings and money markets come in around 0.65%. These are more liquid but still offer a lower yield.

Source: Author's Calculations

A retiree with $100,000 invested in these sources would receive only $1,250 annually or $650 annually. That's nowhere near enough to supplement other retirement sources like Social Security. However, these are very safe investments - their yields are either locked in with a CD or changing with the prime rate. We expect with a recession coming the prime rate will eventually be cut, reducing the yield of savings locked into a money market or savings account.

Outcome: Too little to live on, barely helping annually.

What About T-Notes?

The rate for 10-year Treasury notes is currently sitting at 1.37% and would allow you to more actively trade them, but again - the yield is too low to really assist a retiree needing a revenue stream.

A Flight to "Quality" or a Flight to Poverty?

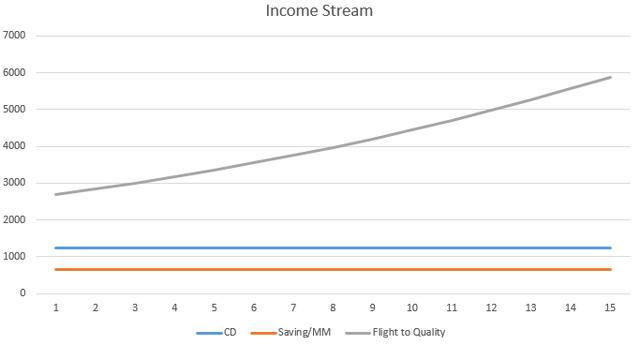

Typically investors engage in what is considered a "flight to quality" when the economy slows down. Well-known and well-loved dividend payers see their market price rise and their available yields drop as investors pile onto these bastions of hope and promise. But this often can have an inverse effect. Like selling out and placing everything into savings or CDs, many see a loss of income from trading into these names.

Some well-known quality names are General Dynamics (GD), Coca-Cola Company (KO), Colgate-Palmolive (CL), and Johnson & Johnson (JNJ). All serve as good examples of this.

|

Ticker |

Yield |

Dividend Growth (5 year Avg) |

|

JNJ |

2.48% |

6.13% |

|

GD |

2.63% |

9.78% |

|

KO |

3.35% |

4.25% |

|

CL |

227% |

2.98% |

All of these options are lower-yielding and enjoy a semi-cult following. There is nothing wrong with them as a supplement to an income portfolio, but should you depend on them alone?

Source: Author's Calculations

We've added our new option to the graph, and immediately we can see a notable difference. For this group, we invested equally $25,000 into each stock and tracked their dividend growth over the 15-year difference. We can see that the flight to quality stocks take time to have a meaningful impact.

If you had $100,000 and enjoyed 15 years of retirement - living from 65-80 years old in retirement. Your average drawdown would be $6,667. So the flight to quality stocks do not even break this threshold by the end of a retirees' average lifespan - not much to celebrate for "getting ahead" here either. These names are considered safer. But even for those "dividend growth" stocks that many considered "safer", recent memory brings back Kraft Heinz (KHC) who until recently was considered part of this quality group that suddenly took a turn and cut its dividend - catching many off-guard.

How Immediate Income Works For You

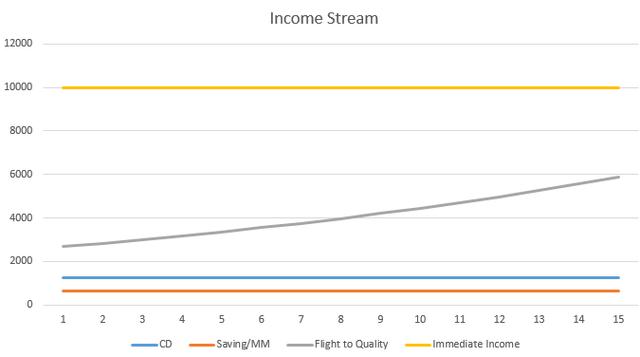

High Dividend Opportunities invests in high-quality names, along with high diversity to achieve our goal of a stable safe income stream. We have been mixing preferred stocks, CEFs, and common equity into a portfolio yielding between 9%-10%. I will provide four HDO picks that reveal how this combination works.

For this calculation we are going to use:

-

Global Partners LP (GLP) which yields 11%.

-

PIMCO Corporate & Income Opportunity Fund (PTY) which sports a 8.7% yield.

-

Sachem Capital (SACH) is a hard money lending REIT that sports a 10.6% yield currently.

-

Newtek Business Services (NEWT) offers a 9.6% yield.

|

Ticker |

Yield |

|

GLP |

11% |

|

PTY |

8.7% |

|

SACH |

10.6% |

|

NEWT |

9.6% |

With these stocks, we've done the same as before, invested $25,000 evenly, and did not reinvest the dividends.

Source: Author's Calculations

As you can see, the flight to quality securities after the average 15 years of retirement fall vastly short of HDO's picks. Now mind you, these are only a portion of our portfolio - furthermore, it doesn't reflect the dividend/distribution growth expected for GLP, SACH, and NEWT.

Limitations to Our Examples

We have to acknowledge some limitations to our examples:

-

We assumed the flight to quality stocks would keep raising their dividends - when they very well might not.

-

As with the vast majority of sectors, some of our picks may have different performance depending on the economic cycles. Our experts are constantly monitoring all of our picks on behalf of our members. Therefore, our holdings might not stay constant for 15 years.

-

The outlook of each stock, and its ability to generate dividends, need to be followed closely to have a successful income portfolio.

We also assumed no dividend reinvestment whatsoever, our retiree in this example - they need this money to live!

The Bottom Line

After 15 years, how did all of our strategies work out?

|

Method |

Total Income Received |

Percent of Original Investment Returned |

|

CD |

$18,750 |

18.7% |

|

Money Market |

$9,750 |

9.7% |

|

Flight to Quality |

$61,367.61 |

61.3% |

|

HDO Picks |

$149,625 |

149.6% |

Over 15 years the difference is outstanding, investing in "immediate income" stocks more than doubled the output of "dividend growth" stocks in choices that are stable, high-yielding, and have strong fundamentals. In the end, retirees don't need to wait 15 years to see the benefits of their investments, and your life shouldn't be put on hold for a hypothetical monetary windfall.

Investing in immediate income can unlock a massive amount of potential and income from a portfolio of any size. If you're sitting on a portfolio of $100,000 or even $1,000 you can see the benefits and impacts of switching your portfolio into high gear. COVID-19 may have pushed your retirement date sooner, but that doesn't have to be a bad thing if you fine-tune your portfolio now.

********

Rida Morwa recently joined the ElliottWaveTrader.net analyst team, bringing his hugely popular High Dividend Opportunities service, the largest-known service for income investors and retirees, with over 4000 members, and featuring a model portfolio with a 9-10% overall dividend yield. Free 15-day trial available here.

More from Silver Phoenix 500