Return Of The Euro Crisis: Italy Quakes As Rest Of The World Shakes And Merkel’s Empire Breaks

Europe’s many fault lines are spreading once again, bringing the endless euro crisis saga back in 3-D realism. Italy gained a new anti-establishment government last week, even as Spain elected a new Socialista government that could crack Catalonia off from the rest of Spain. All of Europe fell under Trumpian trade-war sanctions and threatened their own retaliation. And Germany’s most titanic bank got downgraded to the bottom of the junk-bond B-bin.

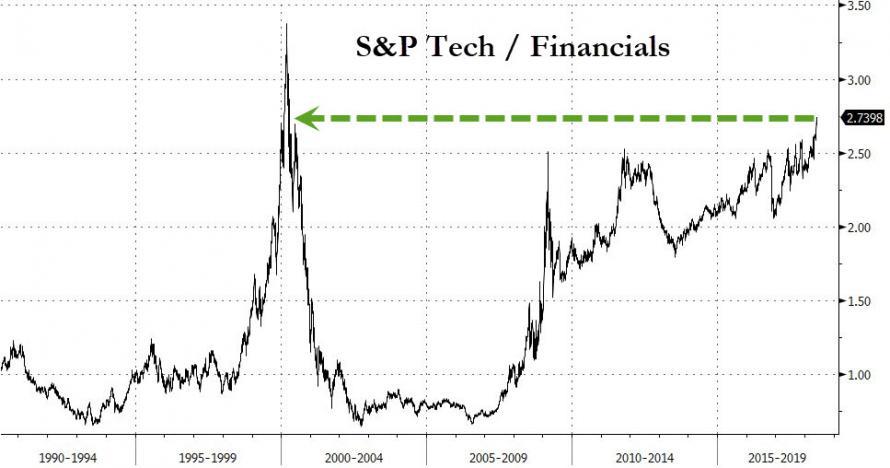

The Italian shakeup caused US bond prices to soar (yields to drop) in a flight of capital from European bonds, yet US stock investors took this invasion of troubles from foreign shores as good enough news to end the week on a positive note. The NASDAQ especially never looked happier, though financials feared contagion. As a result, the contrast between tech stocks and financials burst upward to its highest peak since the top of the dot-com frenzy:

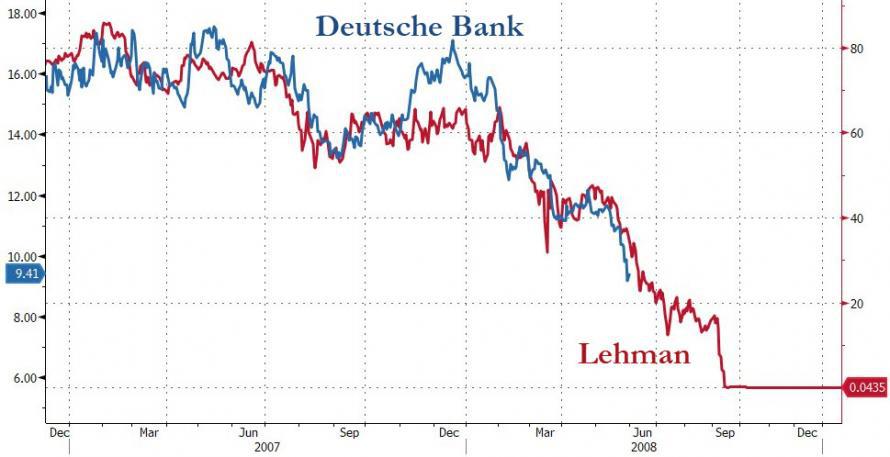

While Europe’s troubles apparently sounded like great news to US stock investors, the Italian crisis caused EU bank stocks in aggregate to take one of their largest avalanches in history, ending in a one-week cliffhanger at their lowest level in two-and-a-half years. Deutsche Bank, Germany’s titan of global finance, ended looking like the spawn twin of the Lehman Brothers:

Deutsche Bank appears to be leading the way into a full blown euro crisis like Lehman Bros did in the US financial crisis.

In one week, Europe with its impossible euromess moved back into position of being the world’s chief menace. The Eurozone is a house of cards with many exits, each with their own name, as I’ve written about frequently in the past, and it’s time to pay the never-ending euro crisis some attention once again.

Quitaly Looks Like Next Brexit In Everlasting Euro Crisis

But do Italy’s political-economic problems even matter? Well, Italy ruptured last week, and the rest of the earth trembled, clearly showing that Italy’s fault lines have the capacity to become the epicenter of another global financial crisis. While things ended well in the US, financial markets around the world fell off a cliff when Italy’s newly formed eurosceptic government’s choice of finance minister was negated by Italy’s figurative president. Who would think inner politics of a second-tier political appointee in a second-tier European economy would cause the entire globe to shake?

Even US stocks plunged that particular day with the Dow plummeting 400 points. Though they recovered later in the week, which was only after Italy’s government managed to compromise on choice of a finance minister. Asian markets saw big drops, too. Such a global reaction to a country where the average government only lasts fourteen months anyway proves contagion is still alive and well.

At the fault line of this earth rattling event, Italian bonds immediately busted open with the two-year yield leaping from 0.9% to 2.4% in less than a day! That hasn’t happened in more than thirty years. Some of that money fled to the US, shaking the yield on the US 10-year down from 2.93% to 2.77. That’s a sizable one-day thump for the US bond market, which moves slower than cooling lava. The only day in recent years that saw the US 10-year fall that much was the time Trump triumphed in the US elections.

Italy’s new premier, Giuseppe Conte, made clear in his inaugural speech this week that the new populist Italian government is setting a trajectory for radical policy changes that put another euro crisis directly in the cross hairs. Instead of European enforced austerity, Italy will jettison Europe’s 3% budget deficit rule while establishing guaranteed income for everyone, a minimum wage, and better health care. How the debt-buried nation is going to pay for that, no one knows, except that simultaneously ditching the deficit rule reveals a clear path. To wit, in the same way the US promises greater government spending with lowered taxes, Italy’s new premier promises a new flat tax. That was a big part of why Italy’s bond interest took off again this week.

I guess that is how you get to be populist … by promising voters things that cannot be done. Welcome to Euro Disney. The result is that Old Glue Factory, the US dark horse, is back in the race to the top of the heap, thanks to Italy. The gradual move in the US toward a bond bust got a quick reprieve when euro trash became US treasuries. So, Old Glue Factory bolts ahead in the backstretch.

Oh, but before you find relief in that thought (if you’re from the US), consider this oddity of Wonderland economics: Italian bond yields still remain lower than US yields. Yes, the country that is crashing has lower yields than the far more stable and sizable US because its debt is mostly purchased by the European Central Bank, which controls interest rates. That creditor relationship, however, is precisely what is now most at stake. So, how do you spell mispriced risk? E-C-B.

In a more stable global economy, the rejected confirmation of a finance minister in Italy wouldn’t have raised a single goose bump, much less chicken flesh all over China. Makes one wonder how small the trigger for collapse could eventually be. Perhaps people are a little jumpy because of how fragile the bond market is:

Fast forward to today when one of the icons of credit and distressed investing, Oaktree Capital, joined the bandwagon of fallen angel hunters, saying that the fund “expects to see a flood of troubled credits topping $1 trillion as rising interest rates overwhelm low-quality loans and bonds….” Oaktree Capital’s Chief Executive Jay Wintrob said that when the cycle turns it will be faster and larger than ever as “fallen angels” proliferate, and added ominously that “there will be a spark that lights that fire.” Picking up on last week’s warnings by Moody’s, in which the rating agency warned of a junk bond default avalanche as rates rise, Wintrob said that the supply of low-quality debt is significantly higher than prior periods, while the lack of covenant protections makes investing in shaky creditors riskier than ever. (Zero Hedge)

Italy is a spark in a global bond tinder box, but it is also a flame thrower in the European financial system’s house of paper cards because it is not as if the EU is going to accept any part of Italy’s new governmental agenda. The battle is on, especially if Italy’s election rhetoric carries through:

Slaves of the European Union? No, thanks! I can’t wait for Italy … to regain its sovereignty to defend the national interest in any way possible…. The immigration policies and economic sacrifices imposed by the European Union have been a disaster and will be rejected by the free vote of Italians…. League will always defend our fisheries and the agriculture of Italy. Enough with the European standards that slaughter our businesses and our territory! (Zero Hedge)

With Italy’s situation now the worst it has been since World War I, it looks like this will be the summer of Italy’s discontent. It’s per-capita GDP is now 8% lower than it was in 2007 when the Great Recession began, making Italy second only to Greece in terms of how deep and long the Great Recession’s impact has been. Because Greece’s and Italy’s debt burdens were the worst of the Eurozone (at 109% of GDP and 102% respectively) at the start of the Great Recession, they were positioned the worst of any of the Eurozone countries to weather the recession.

For those reasons, one of Prime Minister Conte’s prime objectives is to cancel 250 billion euros of Italy’s debt. As with the attempted resolution of Greece’s credit collapse, this is an epic battle that will be in the news for a long time as creditors rage against the EU government and the Italian government, wrestling to find a solution that fails to solve the problem. Conte is also pushing for EU treaty revisions that include a measure that would allow European nations to exit the euro in order to regain their own monetary sovereignty.

Bear in mind, Italy’s debt remains tenable only because it exists in an environment of extraordinarily low interest created by the ECB, given that Draghi has not yet begun the ECB’s unwind. But wait! The ECB has essentially been the only buyer of Italian bonds for the last couple of years. That makes the ECB the counterparty to any bankruptcy action by Italy’s government that would try to write down debt. The central banksters will have to scrape a little caviar back off their biscuits if they’re going to resolve this, and it is not at all clear why eurocentric kings would feel friendly toward such eurosceptic paupers. I can’t imagine them washing that dry gulp down with Dom Pérignon.

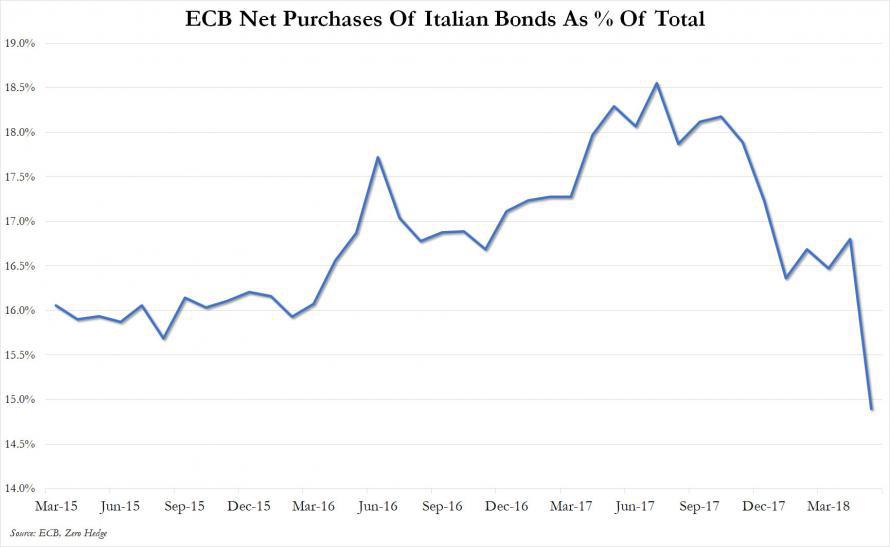

The European Central Bank Stepped Back From Saving Italy

It would appear that the ECB decided to punish Italy for electing a non-globalist, eurosceptic government because it backed sharply away from buying Italian bonds right at the moment of their greatest need:

Laura Castelli, another Five Star parliamentarian … said in an interview with Huffington Post that “the ECB and Italian banks have slowed up if not suspended their buying of [Italian government bonds] . . . which is adding to pressure on spreads”. She also argued that “quantitative easing is being weakened at exactly the moment when we need it strengthened to secure the stability of the EU.” As it turns out, skeptical Italians [were] proven right because as the ECB revealed when it disclosed its … bond purchases for the month of May … the central bank sharply scaled back the proportion of Italian purchases relative to all other bonds … in the month of May. (Zero Hedge)

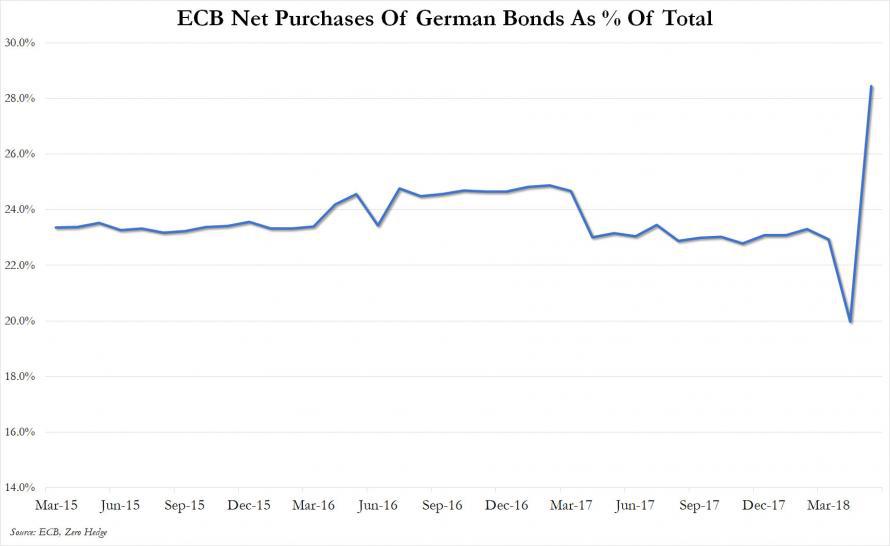

The ECB, however, had no problem helping save Germany:

No wonder some Italian leaders have become euroskeptics when it comes to wondering if their Italian-led European Central Bank will still follow Drag’s promise to “do whatever it takes” when it comes to saving Italy.

Whether the ECB’s lack of bond buying was intentional europunishment or not, the blow-out in Italian bond yields revealed how bad things can be when the central bank isn’t there to be the savior as buyer of last resort. How much worse will this re-opened rift in eurozone crisis become for Italy and the rest of Europe when the ECB backs away from buying everyone’s bonds as Bankster Draghi has promised … IF he follows through with his predicted course of quantitative tightening this year? This is what happens in an environment where the ECB has just begun to taper its bond purchases, but the ECB has indicated it will curtail them entirely by the start of 2019.

“All the Italian political headlines so far have occurred against a backdrop of incredibly easy monetary conditions, and should such events transpire in the future, their impact on markets will be even greater as the cushion against such shocks will be much thinner,” said Aaron Kohli, fixed-income strategist at BMO Capital Markets. (MarketWatch)

Clearly, Europe does not have the capability of coping with the removal of ECB life support.

(Incidentally, the ECB’s rescue of German bunds during this blowout was the major cause of Bill Gross’s biggest one-day loss ever for Janus’s unconstrained fund — another anecdotal example of contagion potential for the US and beyond. There are so many connections between Europe’s financial faults and the US that the possible paths for contagion are unlimited.)

In the centrally rigged world of banking, the ECB controls the price of all European bonds, so they can pick and choose winners; but if they back out entirely as promised, every nation in Europe becomes a looser. If you don’t believe me, hide and watch. A European financial crisis is going to happen. It is only a question of how soon. And this euro crisis will be much more than financial; it will be cultural and political as well. It has never been possible to end CB recovery efforts (in either the US or Europe) without ending their fake recovery results. Look at Japan: Every time they back away from their decades of quantitative easing, they have to move right back to even greater easing … and they have never dared try real tightening.

For now, the Teutonic European Central Bank appears to be picking and choosing winners and losers in order to chastise those that show signs of moving away from the euro. On the other side of this fight, Italian politicians are now calling on Germany to leave the euro in order to end its dominance over the rest of Europe. (Who would have thought during the formation of the European Community that Germany would try to control all of Europe?).

Watch Angela Merkel’s Endless Return of the Euro Crisis in 3D

Having noted in the past how the Merkel-driven European government’s insistence on rampant immigration was fueling a much larger euro crisis than we’ve seen so far, I should note here that a good share of the calories that are now lighting Italy on fire came from the fact that Merkel’s government force-fed Italy and Greece with most of that immigration. The governments of Europe’s centralized economy can force their fanciful ideas of harmonious global integration all they want, but blowback is assured, and it is happening now, just as I’ve said it would.

As the editor of Capitalist Exploits recently said:

“Italians are happy about it in the same way you’d be happy with genital mutilation.”

And, so, risk is rapidly rising again in Emperor Merkel’s Euro Crisis Zone … and just as “harmonious global recovery” was filling global media with hope of happy endings for all for years to come! Just when you thought it was safe to go back in the water, the tsunamic tide rolled out much further than usual, revealing that the emperor has been swimming in her new clothes.

(Photo of Angela Merkel in 3D glasses by Kuebi (Armin Kübelbeck)) (http://www.gnu.org/copyleft/fdl.html, CC-BY-SA-3.0 / http://creativecommons.org/licenses/by-sa/3.0/), via Wikimedia Commons)

David Haggith started writing about the economy after he predicted The Great Recession half a year before it hit and was puzzled as to why no economists or stocks analysts saw it coming. In the months after the crisis broke out, he started to write humorous editorials in a series titled “Downtime,“ which chided the U.S. government and bankers who should have seen the economic collapse coming but whose cronyism, greed and ineptitude caused them to run the world into a ditch. Those articles were published in The Hudson Valley Business Journal, The Valley City Times-Record (North Dakota), and The Daily Herald in Tennessee. Haggith is dedicated to regularly criticizing the daily news — not just the content but the uncritical, unthinking nature of almost all of the reporting. He now writes his own blog, The Great Recession Blog, to break down the news as an equal-opportunity critic toward both Republicans and Democrats / Conservatives and Liberals … since neither kind of politician has done anything worthwhile to plot a better economic course. His articles are regularly carried by several economic websites.

More from Silver Phoenix 500