Share Buybacks…Good Or Bad?

Buy Low and Sell High!

Though this is what investors aim for, many (most?) wind up doing just the opposite. Companies buying or selling their own shares are notorious for their awful timing. Rather than indicating merely lousy skill, many times it points to corporate leaders acting in their own, personal interests, even when that is opposite to their fiduciary responsibility of working for the benefit of all shareholders.

When you hear a CEO say that the company is buying back its own shares ‘To release shareholder value,” you may need to dig deeper. After that kind of “handshake,” you may want to count your fingers.

So, why would companies buy back their own shares? A good reason might be that the market is undervaluing the growth in company earnings expected by the company officers. There may have been a Research & Development breakthrough which “the Market” doesn’t fully appreciate. A new product may be about to be launched which could cause profits to take off, followed somewhat later by the stock price.

Or, general stock valuations may be unusually low due to a Recession which is ending. The S&P 500 and other market indicators go in long cycles – sometimes the Price to Earnings Multiple (PE Ratio) gets below 7 times earnings (YES, this happens roughly every 30 years or so!). A recovery, and money printing by the FED, tend to encourage a stock buying surge, and the PE Ratio goes up, without needing actual profits to go up.

Buying company shares when the officers believe the price will go up may make a lot of sense. Or, the company may not buy shares back if there is a very profitable use within the company. Allocating capital is an important function of company management.

But, sometimes (many times?) a company may buy its own shares even when the price is expensive. The PE Ratio, instead of being at a low 7, is above the 100 year average of 14 – today the PE Ratio on the S&P 500 is about 20.

Officers would need a very good reason to buy back shares at these levels. If the company’s total Dollar earnings were growing quickly (10-20% a year, for example), then a PE of 20 still might be a low price.

Two other reasons why shares are bought back are their effects on Earnings Per Share (EPS) and on Stock Options. Let’s look at what a buyback does.

After a share buyback, there are fewer shares held by investors than there would have been otherwise. Whatever the total Dollar amount of earnings the company reports, EPS will be higher than without the buyback. Total profits have not changed, but the EPS is higher – artificially.

To put some numbers to it, if the company has 1 Billion shares outstanding, and earns $1 Billion, then the EPS is $1.00 per share. If the company buys back 100 Million shares, then ($1 Billion / 900 Million shares) the EPS jumps to $1.11 per share. Management’s performance looks better, and maybe they keep their jobs or get a big bonus.

Since the stock price ultimately is tied to how much the company earns, the stock price likely will go up, maintaining the same PE Ratio. This higher stock price for remaining shareholders is why management can even claim to be releasing shareholder value.

Stock Options often are granted to management, in lieu of cash. The company may be short on cash, or the Options may be used as an incentive to help profits grow.

Those profits, on an EPS basis, can go up either because the total Dollar profit went up or because the number of shares went down. An officer has a real incentive to want a company share buyback because it raises the EPS – and by raising the share price, the Options become worth more.

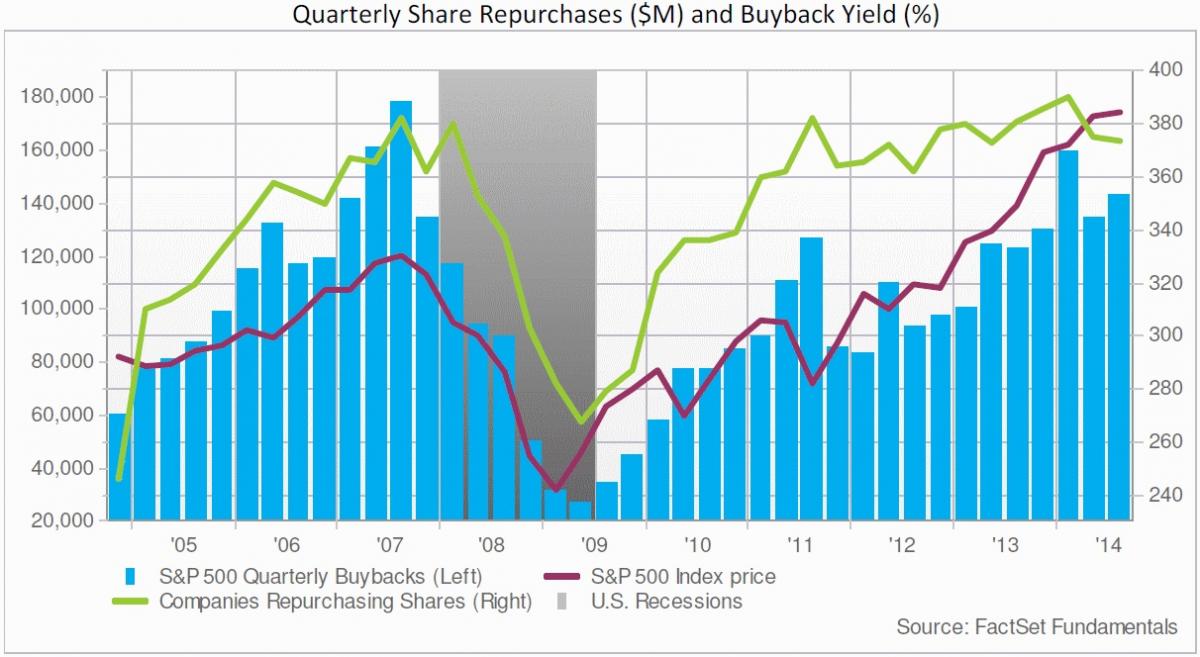

Looking at the S&P 500, the number of companies, and the amount they spend, buying back shares changes over time. As the US went into the last Recession, the number of S&P 500 companies doing buybacks fell from 380 to 270, and spending went from $140 Billion to $30 Billion.

When the S&P 500 was at its lowest – around 250 – buybacks were at their lowest levels. Now that the S&P 500 has gone up well over 50%, more buybacks are being done.

So, how can you tell if a buyback is good for investors? See if the stock is cheap – is the PE low compared to EPS without the buyback or compared to total Dollar profit growth for the company (and compared to other companies in that industry)?

If the stock is not cheap, see if there are a lot of Stock Options held by the officers, or if the EPS, without the buyback, would have been dismal. If the officers are succumbing to their own interests above the shareholders’ interests, then this may not be a stock you want to own.

If you’re “lucky” enough to have a large stake in the company, it may be worth your while to start a shareholder uprising to throw these rascals out. Having an new team – even if inexperienced – who will work for you, instead of against you, really might increase shareholder value.

Robert (Bob) Shapiro is self-taught in Austrian Economics and has consulted briefly for the governments of Mexico, Greece, Portugal and Spain. He has traded Gold & Silver and their stocks since 1970. Bob Shapiro’s blog is http://us-issues.com

Robert (Bob) Shapiro is self-taught in Austrian Economics and has consulted briefly for the governments of Mexico, Greece, Portugal and Spain. He has traded Gold & Silver and their stocks since 1970. Bob Shapiro’s blog is http://us-issues.com

More from Silver Phoenix 500