Silver Saddens the Permabulls

After a crash to the 200-day MA, is this the bottom, or could silver retest its March lows?

A Reality Check

While the permabulls proclaimed that interest rates were irrelevant and that silver had entered a new bull market, we warned on Apr. 28 that their confidence was extremely shortsighted. We wrote:

Resilient [earnings] prints driven by price increases highlight how demand and inflation support higher, not lower, interest rates. And with the crowd expecting the opposite, the fundamentals materially contrast the prevailing sentiment. As such, when reality sets in that inflation is a problem again, the PMs should come under immense pressure.

To that point, with short and long-term interest rates (to a lesser extent) ratcheting higher, silver ended the Jun. 22 session down by ~15% from its May high. Consequently, our technical and fundamental expectations continue to bear fruit.

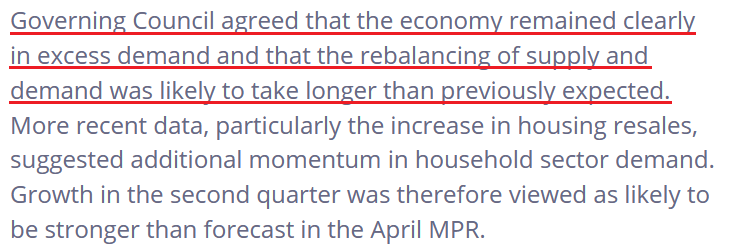

Furthermore, while the Bank of Canada (BoC) surprised the crowd with its latest rate hike, the committee released its summary of deliberations on Jun. 21. The report stated:

“Growth of gross domestic product (GDP) in the first quarter was 3.1%, above the Bank’s expectations of 2.3%. Consumption growth was surprisingly strong, coming in at 5.8%, with strength not only in services but also in goods sensitive to interest rates, such as automobiles, furnishings, and other household products.

“Even after accounting for significant population gains, Governing Council agreed that consumption in Canada was proving stronger and more broad-based than had been expected.”

The committee added:

“Members were of the view that with the resurgence in household spending growth, the pickup in consumer confidence, and the slowing in disinflationary momentum, monetary policy did not look to be sufficiently restrictive.”

So, while we warned that resilient demand would haunt the pivot predictors, the BoC highlighted how the process of normalizing inflation could be one of attrition.

Please see below:

The House Always Wins

While gold has also been a casualty of the hawkish shift, the BoC mentioned how “the increase in housing resales suggested additional momentum in household sector demand.” Similarly, this is not just a Canadian phenomenon.

For example, U.S. building permits and housing starts smashed expectations on Jun. 20. The latter rose by 21.7% month-over-month (MoM) versus an expected decline of 0.8%. As a result, resilient demand and too low long-term interest rates have property developers eager to build.

Please see below:

Likewise, Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), said:

“A bottom is forming for single-family home building as builder sentiment continues to gradually rise from the beginning of the year. The Federal Reserve nearing the end of its tightening cycle is also good news for future market conditions in terms of mortgage rates and the cost of financing for builder and developer loans.”

Yet, while he’s correct on the first point, his second point mirrors the faulty argument that led the silver permabulls astray. If the housing market rebounds, it signals that rates need to rise, which means the Fed is not near the end.

Remember, the housing sector is the most sensitive to interest rate increases. And if North Americans are eager to purchase homes, it means that interest rates are not high enough to dissuade them. It also means that interest rates are not high enough to eradicate inflation.

To that point, while the drop in oil prices on Jun. 22 could help suppress the headline Consumer Price Index (CPI), the core CPI has barely budged. For context, we wrote on Jun. 16:

It stands at 5.33% year-over-year (YoY), and the MoM figure has been 0.30% or higher in each month since October 2021. Furthermore, it’s been 0.38% MoM or higher in each month for the last six months. In contrast, the Fed needs the metric to hit ~0.17% MoM to align with 2% annual inflation. In other words, we’re nowhere near substantial progress.

Supporting the claim, the Cleveland Fed has the core CPI coming in at 0.43% MoM in June, which annualizes to 5.3%. Thus, while stocks ignore at their own peril, inflation anxiety has certainly impacted the PMs.

Overall, our technical and fundamental outlooks continue to unfold as expected. Resistance levels have proved formidable, and the shifting economic landscape has helped boost the performance of our GDXJ ETF short position. And with the junior miners’ index ending the Jun. 22 session down by nearly 20% from its April closing high, we believe a recession-induced U.S. dollar rally will help push the GDXJ ETF to its final bear market low.

Do you think the PMs will enjoy brief countertrend rallies before their downtrends resume?

*********

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.

More from Silver Phoenix 500